Council on Energy, Environment and Water Integrated | International | Independent

Suggested Citation: Khan, Adeel, Srishti Mishra, Rahul Das, and Priyanka Singh. 2026. Organic Waste Circular Economy for Viksit Bharat: Jobs, Investment, and Emissions Pathways to 2047. New Delhi: Council on Energy, Environment and Water.

India aims to become a Viksit Bharat by 2047, with an economy valued at USD 30 trillion. As urbanisation accelerates, Indian cities are expected to generate approximately 435 million tonnes of municipal solid waste (MSW) by 2050. The organic fraction of MSW (OFMSW), which includes kitchen waste, market waste, and horticulture waste, accounts for about half of all MSW generated in India. Mismanaged organic waste contributes to methane emissions, air pollution, and biodiversity loss. When managed properly, this waste stream has the potential to unlock a wealth of resources, including clean energy (biogas and biomethane) and nutrient-rich compost, creating green jobs and driving economic growth.

This report provides a strategic roadmap for India to achieve circularity in organic waste management in support of the Viksit Bharat vision. It assesses three scenarios – the business-as-usual (BAU) scenario, the accelerated policy scenario (APS), and the ambitious green transition scenario (AGTS) – to quantify investment needs, market opportunities, employment potential, and emissions reductions by 2047.

The study draws insights from multiple expert interviews and stakeholder consultations across policymakers, private sector actors, academic institutions, financial institutions, and civil society. The study maps systemic barriers and enablers across six themes: policy and governance, infrastructure and technology, financial viability and business models, human resources and capacity building, data and information, and awareness and behaviour change.

India aims to become a Viksit Bharat by 2047, with an economy valued at USD 30 trillion (Ministry of External Affairs 2024). Cities in India are currently the engines of this growth, contributing about 60 per cent of the country’s gross domestic product (GDP) (NITI Aayog and Asian Development Bank 2022). India is also expected to undergo one of the largest urbanisations globally, with more than 416 million people projected to move to cities by 2050 (García 2023). As urbanisation accelerates and lifestyles change, Indian cities are expected to generate approximately 435 million tonnes of municipal solid waste (MSW) by 2050 (Khan et al. 2025). In the absence of effective waste management systems, and under the prevailing ‘take– make–waste’ model, this growth in waste generation can exacerbate several local and global challenges, including pollution, urban flooding, biodiversity loss, and climate change.

A transition to a circular economy is therefore both urgent and imperative, and it provides a pathway to effectively utilise resources, reduce pollution, and create green jobs for the future. Given their extensive resource use and concentrated populations, cities play a crucial role in embedding and scaling circular economy principles. Advancing circularity in cities will be pivotal to India’s growth trajectory and to building liveable, clean, and resilient urban centres.

The organic fraction of municipal solid waste (OFMSW), which includes kitchen waste, market waste (vegetables, meat, fruits, and flowers), and horticulture waste, accounts for about half of the total MSW generation in India (MoHUA 2022). Embedded within OFMSW are valuable resources, such as water, nutrients, and clean energy, which can be recovered through processes such as composting and biomethanation (Ddiba et al. 2022). When harnessed effectively, these processes generate nutrient-rich compost that can substitute for chemical fertilisers, while biogas or biomethane can contribute to clean energy and reduce energy imports. Further, the valorisation of OFMSW can reduce methane emissions and prevent contamination of recyclable materials, such as paper, cardboard, and plastics.

Our review reveals that approximately 16 ministries and government bodies are involved in promoting and implementing multiple organic waste management initiatives, encompassing 9 programmes, 3 policy guidelines, and 7 schemes. Flagship initiatives, such as Swachh Bharat Mission–Urban (SBM-U), the National Bioenergy Programme, and Galvanising Organic Bio-Agro Resources Dhan (GOBARdhan), among others, have begun shifting the focus from waste disposal towards resource recovery. We also found that there has been a concerted push to create a favourable environment for biomethanation.

This study addresses a key research gap by assessing how different approaches to organic waste management, including shifts in the treatment mix from composting towards biomethanation, can support India’s Viksit Bharat vision, and what ecosystem levers are needed to enable this scale-up. To address this, we developed a strategic roadmap for organic waste circularity and assessed three scenarios using sigmoid curve modelling: the business-as usual (BAU) scenario, the accelerated policy scenario (APS), and the ambitious green transition scenario (AGTS). These scenarios set targets based on the rate of collection and processing of organic waste with varied allocations of treatment capacities for biomethanation and composting by 2047. For each scenario, we quantified the investment required to establish the facilities, the market opportunity for the end products, the job creation potential, and the emissions reduction potential.

We conducted expert interviews and stakeholder consultations with diverse stakeholders, including policymakers, private-sector actors, academia, financial institutions, and domain experts, to identify current gaps in the ecosystem that must be addressed to unlock this potential. Insights from these consultations can provide strategic foresight to policymakers across ministries, such as the MoHUA, the Ministry of New and Renewable Energy (MNRE), and the Ministry of Petroleum and Natural Gas (MoPNG), as well as for business and city leaders seeking to harness organic waste as a driver of India’s circular economy transition.

Currently, biomethanation and composting are the two most widely adopted organic waste processing techniques in India, accounting for approximately 4 per cent and 96 per cent of treatment capacity, respectively (MoHUA n.d.). Beyond these two dominant techniques, other waste processing options, such as black soldier fly and briquetting, are available, but their uptake remains limited. Figure ES1 presents the economic and environmental potential of integrating circularity into OFMSW management across three scenarios.

Investment potential: Under a BAU scenario, current investments in waste processing are projected to increase to USD 4.5 billion by 2047, up from the current baseline of USD 0.9, with around half of the waste remaining untreated. In contrast, under the APS and AGTS, investment opportunities would increase significantly, reaching USD 24.3 billion and USD 30.2 billion, respectively, by 2047.

Market potential: The market size for end products reflects this shift. From USD 10.0 billion under the BAU scenario, the market could expand fivefold to USD 50.6 billion under APS and further to USD 61.5 billion under AGTS by 2047.

Job growth: India’s strides in organic waste management are expected to shape job creation over the coming decades. Under APS, the sector could potentially create 2.6 million jobs by 2047. Under AGTS, direct job creation is estimated at 1.9 million, slightly lower due to the greater contribution of biomethanation, which is characterised by higher levels of mechanisation than composting.

Emissions reduction: Waste has been one of the fastest-growing contributors to India’s emissions, increasing by 226 per cent between 1994 and 2020 (MoEFCC 2024). Under the BAU scenario, emissions from the sector could reach 119.5 MtCO₂e by 2047. Under the APS and AGTS, emissions from the waste sector are reduced, while the use of end products in sectors such as agriculture, transport, and industry enables additional emissions offsets of 67.5 MtCO₂e and 100.5 MtCO₂e, respectively. Together, these outcomes position OFMSW management as a key lever for driving low-carbon growth and supporting India’s net-zero ambitions.

Figure ES1. USD 60 billion+ market opportunity can be unlocked by scaling organic waste treatment in India by 2047

Note: Under AGTS the number of jobs reduce due to a shift towards biomethanation, which is more automated and capital-intensive than composting. Negative emissions in the APS and AGTS scenarios arise from diverting waste from dumpsites and using end products across agriculture, transport, and industry to displace fossil fuels and chemical fertilisers.

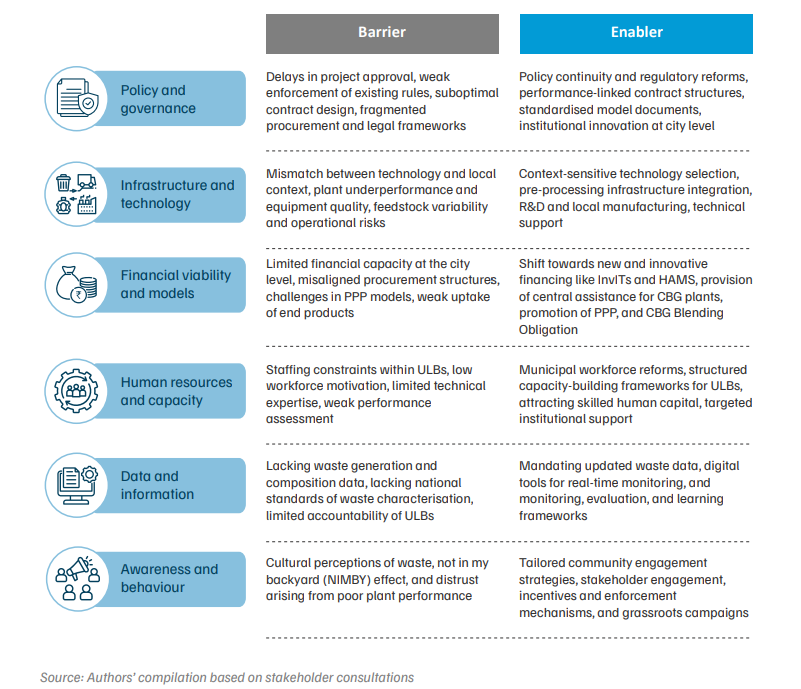

There is significant potential for a circular economy in OFMSW to drive economic growth, create millions of green jobs, provide a low-carbon pathway, and support cleaner cities. However, unlocking these opportunities requires a holistic, multi-stakeholder approach that accounts for the range of challenges and levers. Drawing on our analysis and insights from stakeholder consultations, we identified certain barriers, including delays in project approvals, weak enforcement of waste management rules, variability in feedstock quality and quantity, competition for end products, limited local capacity, lack of data on generation and composition, and low levels of awareness. At the same time, we identified certain enablers, including policy continuity, research promotion, local manufacturing, innovative financing mechanisms, digital public infrastructure, and targeted capacity building and training initiatives. We have mapped these barriers and enablers across six different themes and provided a summary in Figure ES2.

Figure ES2. Barriers and enablers associated with organic waste management across different themes

Note: R&D – Research and Development; CBG – Compressed Biogas; PPP – Public–Private Partnership;

ULB – Urban Local Body; InvITs – Infrastructure Investment Trusts, and HAMs – Hybrid Annuity Models

Translating this potential into reality will require coordinated action from stakeholders across governments, private enterprises, academic institutions, multilateral banks, and civil society to address systemic barriers and translate enabling levers into policies, infrastructure, markets, and mindsets. As India prepares to host the World Economy Forum in 2026, it has a unique opportunity to showcase progress in the sector and strengthen international collaboration to advance the circular economy agenda as a pathway for climate action. To support this transition, we propose the following seven action points:

The organic fraction of municipal solid waste (OFMSW) includes kitchen waste, market waste (vegetables, fruits, meat, and flowers), and horticulture waste. It constitutes roughly 50 per cent of all MSW generated in Indian cities. Effective management of OFMSW can halve the overall waste burden, recover valuable resources such as biogas and compost, reduce methane emissions, and improve the quality of other recyclable materials like paper and plastic.

The two primary methods are composting and biomethanation. Composting converts organic waste into nutrient-rich compost that can substitute chemical fertilisers. Biomethanation is an anaerobic process that produces biogas (and, when purified further, compressed biogas or CBG), which can be used for cooking, electricity generation, or as a transport fuel.

The report models three scenarios for India by 2047. The Business-as-Usual (BAU) scenario assumes the current situation, with 90 per cent waste collection and only half the waste processed. The Accelerated Policy Scenario (APS) targets full collection and 95 per cent processing, with an equal split between composting and biomethanation. The Ambitious Green Transition Scenario (AGTS) assumes 100 per cent collection and processing, with a greater emphasis on biomethanation (66 per cent) over composting (34 per cent).

The report identifies six key challenge areas: weak enforcement of waste management rules and delays in project approvals; technology mismatches and feedstock quality issues due to poor source segregation; limited financial capacity of urban local bodies and challenges in attracting private investment; staff shortages and low technical capacity within municipalities; lack of up-to-date waste data, i.e., waste characterisation; and low public awareness and the "not in my backyard" (NIMBY) effect when setting up treatment plants.

Source segregation, which means separating the wet (organic) waste from the dry waste at the household level, forms the foundation of the entire system of organic waste management. Without clean, segregated feedstock, both composting and biomethanation plants underperform or fail in the long run. Cities like Indore have demonstrated that nearly 100 per cent source segregation is achievable and directly enables high-quality end products and financially viable plants. Poor segregation is cited as one of the most common reasons plants become defunct.

The economic potential varies significantly depending on policy ambition. The accelerated policy scenario could unlock a USD 50.6 billion market and mobilise USD 24.3 billion in investment by 2047, while creating the highest number of direct jobs at 2.6 million. The ambitious green transition scenario unlocks an even larger market of USD 61.5 billion and USD 30.2 billion in investment, but generates fewer direct jobs at 1.9 million, as biomethanation is more automated and capital-intensive than composting.

The waste sector overall is currently one of the fastest-growing contributors to India's greenhouse gas emissions, having grown by 226 per cent between 1994 and 2020. Under a business-as-usual approach, emissions from the organic waste could reach nearly 120 MtCO2e by 2047. Under the accelerated policy scenario and the ambitious green transition scenario, the sector could achieve net-negative emissions of 67.5 MtCO2e and 100.5 MtCO2e, respectively. This is achieved by diverting waste away from dumpsites and using end-products such as biogas and compost to displace fossil fuels in sectors like transport and industry, and reduce dependence on chemical fertilisers in agriculture.

Roadmap of the methodology to assess the climate co-benefits of the SUP ban in Maharashtra

Building a Green Economy for Viksit Bharat

Financing for Treated Used Water Reuse in India

How Much Does It Cost to Recycle a Solar Module in India?

How Big is the Solar Module Recycling Industry in India?