Council on Energy, Environment and Water Integrated | International | Independent

Suggested citation: Jain, Abhishek, Gunjan Jhunjhunwala, et al. 2025. Building a Green Economy for Viksit Bharat: New Opportunities for Jobs, Growth and Sustainability in India. New Delhi: Council on Energy, Environment and Water.

Authors:

Report Leads

Abhishek Jain and Gunjan Jhunjhunwala

Core Team

Wase Khalid, Aaditya Malhotra, and Urwa Tul Wusqa

Research Team

Nicole Almeida, Aryan Bajpai, Spandan Biswas, Astha Chandra, Kartikey Chaturvedi, Parineet Kaur Chowdhury, Pallavi Das, Saiba Gupta, Nikhitha Jagadeesh, Aishwarya Jain, Rishabh Jain, Ayush Kumar Jha, Aishwarya Joshi, Viraj Joshi, Apoorve Khandelwal, Krishna Khanna, Clark Kovacs, Karan Kothadiya, Srishti Mishra, Shruti Nambiar, Ribhav Pal, Kavya S, Narendran S, Radhika Sangal, Riddhim Sehgal, Soham Shah, Aanya Singh, Aarushi Singhal, Aditya Swarankar, Banashree Thapa, Akanksha Tyagi, Swathi Vurrakula, Shreya Wadhawan, and Dana Zain

India’s aspiration to become developed and resilient by 2047 will require a growth model that is both environmentally sustainable and economically expansive. This report demonstrates that a green economy can be a critical engine of that transformation. CEEW’s analysis identifies 36 emerging green value chains across energy transition (ET), circular economy (CE), and bioeconomy and nature-based solutions (BE & NbS). Together, these sectors could shape a new economic frontier for India—one that reimagines how the country produces energy, uses materials, manages waste, and leverages natural resources. Such a low-carbon growth pathway aligns with our development priorities and reinforces our pledge to reach net zero by 2070. This study quantifies the economic potential of these value chains, highlights the barriers limiting their scale-up, and outlines the policy and ecosystem actions needed to mainstream green growth.

Our research suggests that by 2047, a green economy can unlock a market value of USD 1.1 trillion (INR 97.7 lakh crore), employ 48 million people, and attract USD 4.1 trillion (INR 360 lakh crore) worth of investments. By shifting to cleaner energy systems, scaling circular production models, and unlocking value from bio-based and nature-positive industries, India can create new markets, unlock substantial investment opportunities and build sustainable jobs across both rural and urban regions.

The study recommends a focused set of measures to strengthen India’s green economy ecosystem—improving economic viability, securing raw materials, accelerating innovation, upgrading skills, better women employment and women-led entrepreneurial growth and enhancing standardisation and quality control. These can be achieved through a coordinated whole-of-nation, whole-of-government, and whole-of-economy approach, illustrated in the study.

With its Viksit Bharat vision for 2047, India is looking to leverage multiple sunrise sectors, from semiconductors to AI data centres to pharmaceuticals to fintech. Investing in a green economy is an equally important opportunity to remain ahead of the curve in a geoeconomically disruptive global order.

Our research suggests that, a green economy can unlock

A green economy for India cuts across many sectors—from manufacturing and deploying renewable energy to electric vehicles; from circularity of plastics and construction debris to making sustainable aviation fuel from spent cooking oil; from sustainable tourism to new-age biofibres and biopolymers from crop residues—the possibilities are immense. Together, the green economic sectors can also abate ~2.3 billion metric tonnes of carbon emissions, which is ~77.6 per cent of India’s total carbon emissions of 2024 (~2.96 billion metric tonnes).

As India grows, that growth can be future-proof and green. For example, packaging, tourism, transport, semiconductors, and construction are all fast-growing sectors in India. These sectors could be future-proofed with greener solutions like bio-based packaging, eco and agri tourism, zero-emission vehicles, e-waste recycling, and sustainable construction materials.

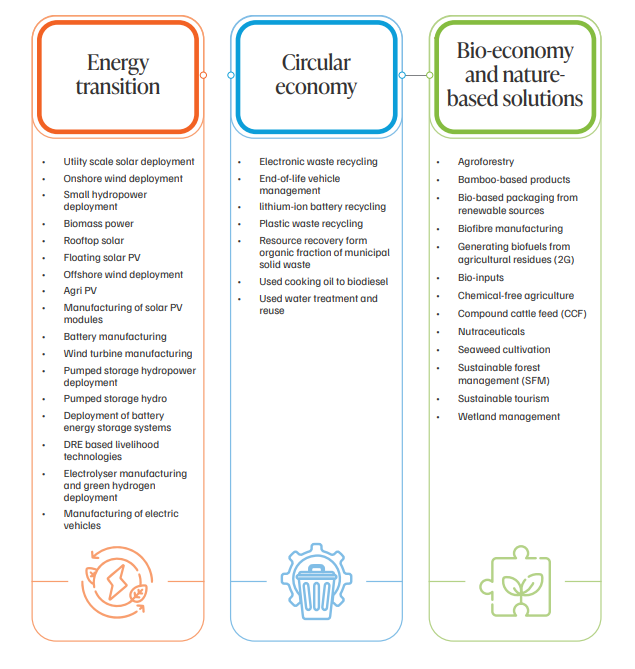

A green economy enables a fundamental rethink of not just the energy we consume, but also the materials we use and the designs we employ in every activity. Across economic sectors, there are opportunities to go green. This report identifies 36 such green opportunities or value chains (refer to Figure ES 1) across three thematic areas: (i) energy transition, (ii) circular economy, and (iii) bio-economy and nature-based solutions. These areas were identified for three main reasons:

Within these three areas, we shortlisted value chains considering:

Figure ES1. Green value chains shortlisted for this report

Source: Authors’ analysis

By no means are these 36 value chains an exhaustive list. More opportunities are available in the green economy, and many more are likely to emerge in the near future. These areas and value chains were chosen to expand our collective imagination of the green economy and its potential in India. At present, many of these emerging opportunities remain overlooked by policymakers, economists, industry leaders, investors, and civil society. This first-of-its-kind report aims to expand our perspectives and deepen our understanding of the wide-ranging possibilities offered by the green economy.

To estimate how each of the green value chains could contribute to India’s Viksit Bharat ambition by 2047 and build evidence on the scale of these opportunities, we measured the jobs, market, and investment (JMI) opportunity. We also identified what’s holding these respective value chains back today, and what actionable next steps could overcome challenges in scaling them up. Table ES1 summarises the JMI for each of the three thematic areas.

Table ES1. Cumulative jobs, market and investment potential of green sectors by 2047

| Green sector | Value chains considered | Jobs (FTE) by 2047 | Market opportunity (in 2047) | Investment opportunity (cumulative by 2047) |

|---|---|---|---|---|

| Energy transition | 16 | 16.6 million | USD 581.5 billion (INR 50.1 lakh crore) |

USD 3.79 trillion (INR 329.2 lakh crore) |

| Circular economy | 7 | 8.4 million | USD 132.2 billion (INR 11.5 lakh crore) |

USD 124.8 billion (INR 10.8 lakh crore) |

| Bioeconomy & nature-based solutions | 13 | 23 million | USD 415.2 billion (INR 36.1 lakh crore) |

USD 229.6 billion (INR 20 lakh crore) |

| Total | 36 | 48 million | USD 1.1 trillion (INR 97.7 lakh crore) |

USD 4.1 trillion (INR 360 lakh crore) |

Source: Authors’ analysis

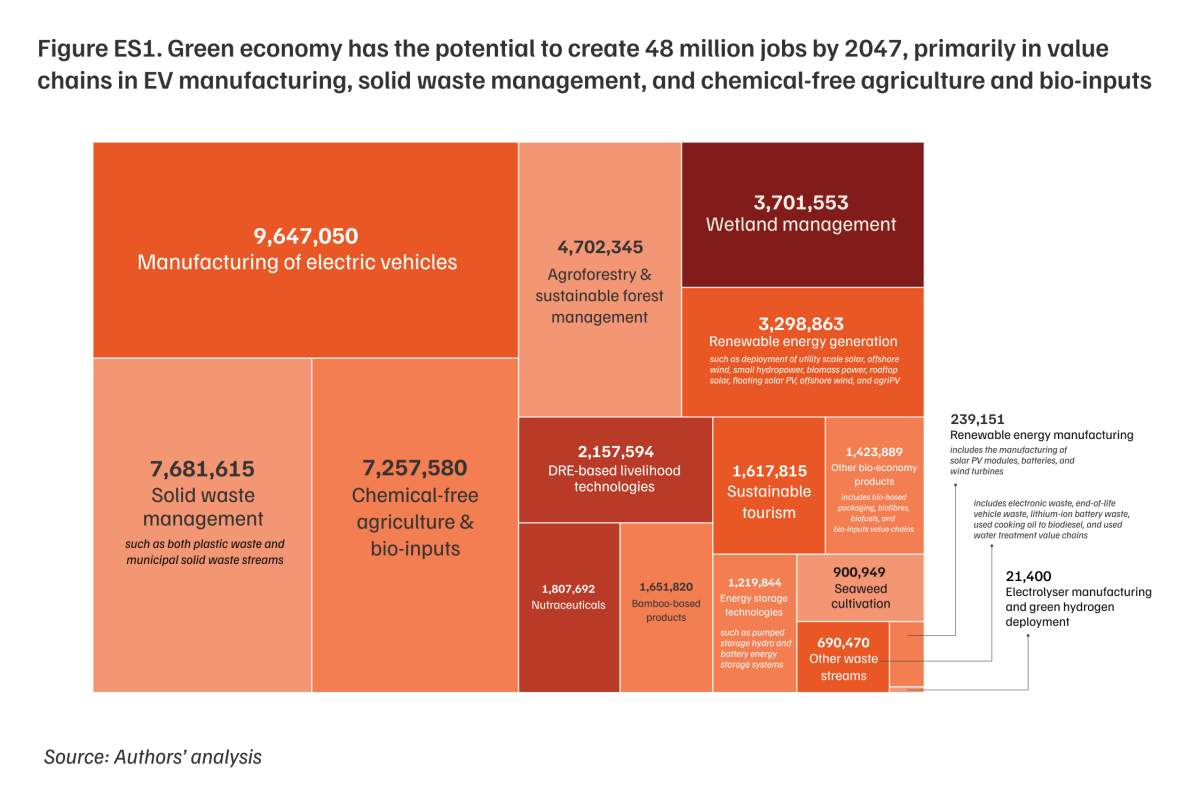

The green economy could create diverse and distributed employment opportunities across urban, peri-urban, and rural areas, and across skill levels. Almost half of the ~48 million green jobs1 (FTE) would be contributed by bio-economy and nature-based solutions, enabling the much-needed economic and livelihood diversification in India’s agriculture-dominated rural economy. Within this sector, bio-inputs for agriculture, agroforestry, and wetland management would be the large job-drivers, followed by nutraceuticals, engineered bamboo products, and sustainable tourism. Figure ES2 illustrates the jobs driven by a green economy.

Value chains in energy transition would be the second-largest set of green employers, creating 16.7 million jobs by 2047. Almost 57 per cent of these jobs would be in electric vehicle manufacturing (largest driver of jobs in a green economy), followed by renewable energy generation (both solar and wind), distributed renewables (2.1 million jobs), and energy storage (1.2 million jobs).

The circular economy would employ another 8.4 million people by 2047. Most of these jobs (7.7 million) are driven by solid waste management—given the large volume and associated large human resource requirements across waste collection, sorting, and aggregation.

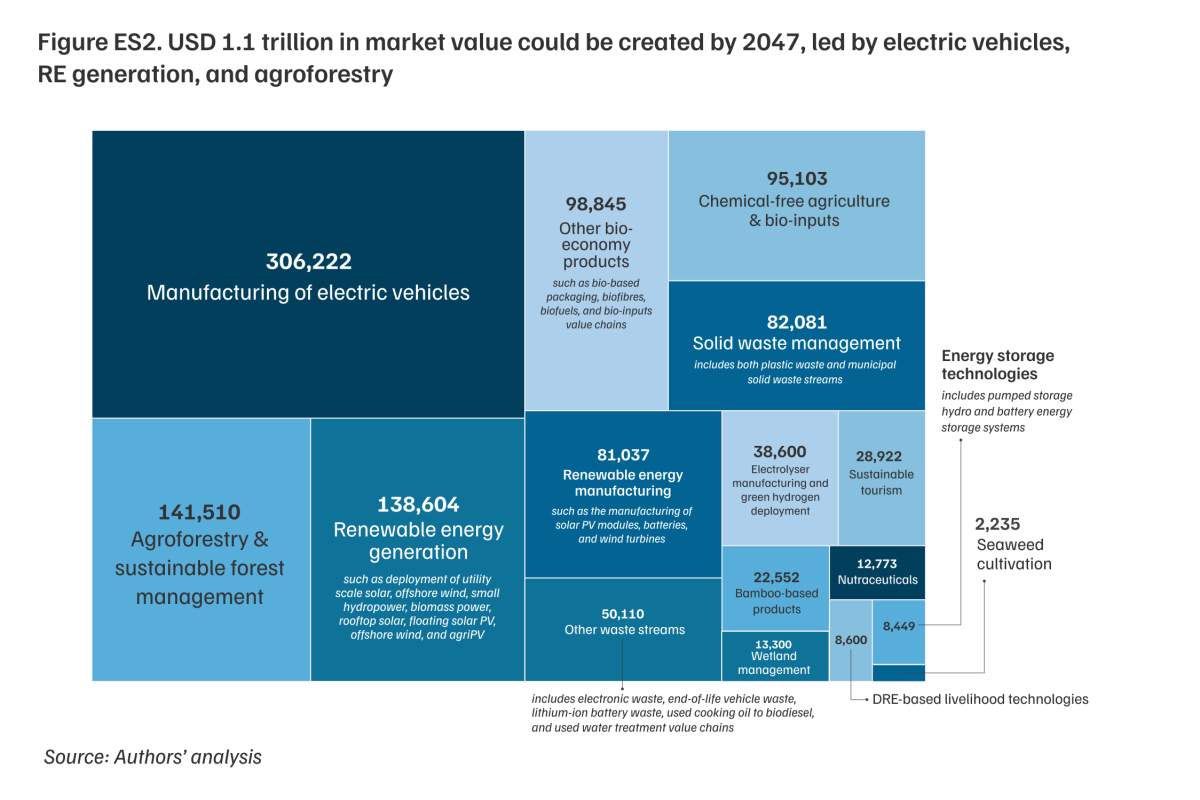

Much like the jobs, the USD 1.1 trillion (INR 97.7 lakh crore) market opportunity of a green economy is also fairly diverse. Both energy transition and bio-economy contribute significantly to the market opportunity, with circular economy contributing about 10 per cent of the market opportunity.

At the value chain level, green mobility, RE generation, and agroforestry and sustainable forest management collectively contribute about half the market opportunity. Respective value chain contributions are detailed in Figure ES3

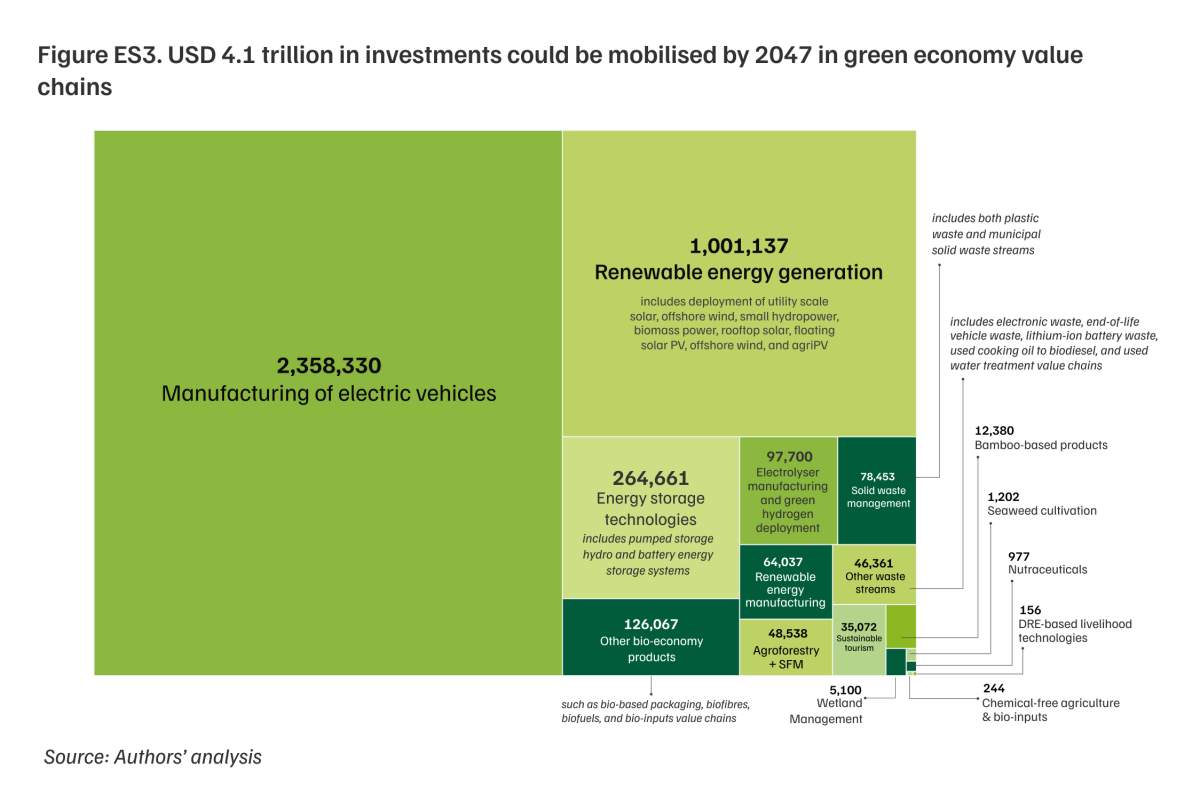

Given its capex-heavy nature, the bulk (almost 90 per cent) of the USD 4.1 trillion (INR 360 lakh crore) investments needed in a green economy get concentrated in the energy transition sector, at USD 3.79 trillion (INR 329.2 lakh crore).

Across the green economy value chains, there is a spectrum from capital-intensive to labourintensive opportunities. Renewable energy generation, renewable energy manufacturing, green mobility manufacturing, energy storage, and green hydrogen are capital-intensive. Investment per direct job in these sectors typically exceeds ~USD 215,000 (INR 1.9 crore) per job, with some segments like renewables and EV manufacturing approaching or surpassing ~USD 225,000–340,000 (INR 2–3 crore) per job in the present modelling. However, these value chains would likely create a greater share of high-value, high-skilled jobs.

Several bio-economy and nature-based solution (NbS) value chains—notably bioinputs, wetlands restoration, agroforestry, and distributed renewable energy (DRE) for livelihoods—create large numbers of jobs at very low capital per job (fractions of INR 1 crore per job). These activities are typically geographically dispersed, often rural, and require complementary investments in training, aggregation platforms, quality assurance, and market access to raise livelihoods and productivity. Furthermore, they generate employment at scale in rural and peri-urban areas and can absorb lower- and mid-skilled labour. Figure ES4 shows the investment potential of several value chains.

The net employment effect of the green economy is a combination of additional employment (new jobs created) and transition (existing workers moving from carbonintensive activities). Manufacturing and grid-scale energy deployment value chains, such as renewables, storage and EV components, will combine both transition and additionality—some workers and capabilities can be redeployed from incumbent industries, but domesticising component supply chains and building new project pipelines will yield net new employment. By contrast, many bio-economy and nature-based solutions value chains are primarily additional livelihoods that diversify and augment rural incomes rather than directly displace fossil-fuel jobs. The circular economy (solid waste and other waste streams) is already seeing an upswing in jobs, albeit the majority are informal in nature. The jobs presented in our report are in addition to the existing jobs.

India’s development goals need 400 million women in the workforce by 2047. However, considering the current growth rate of women in the labour force, the number is expected to reach only 145 million. In the context of the green economy, we discuss the roles women are currently occupying in each sector and suggest measures to boost their participation.

The key characteristics of women’s employment in green value chains are: (i) women’s participation is more dominant in early stages of value chains, where pay is lower and physical labour is greater; (ii) their participation is inversely affected by the remoteness of the job, especially for renewable energy installations; and (iii) the percentage of women entrepreneurs is far lower, with their overall (green and non-green sectors) participation at a mere 14 per cent (MoSPI 2013). While some challenges, like travelling to remote locations, stem from sociological concerns, certain others, like wages and low entrepreneurship, are structural. Accordingly, Chapter 4 offers actionable recommendations to improve overall women’s participation and employment in a green economy.

While the green economy has a vast potential to contribute to India’s economic development, a set of structural challenges holds back the realisation of this potential. Each value chain has its own set of particular barriers to scale, but across them, a few structural and common ones stand out. Here we discuss the common challenges that hold back several of the green sectors, and how they can be overcome:

Finally, making the green economy people-centric will ensure widespread participation and ownership, empowering over a billion individuals to drive India’s journey toward becoming economically thriving, socially responsible, and environmentally resilient.

A green economy is an economic paradigm that ‘protects the environment and stays within the ecological boundaries of nature while promoting jobs and economic prosperity’ (Jain, Jhunjhunwala et al. 2025). Any economic activity qualifies as “green” if it improves resource efficiency or conservation, or if it reduces greenhouse gas emissions and local pollution compared to conventional practices. India’s green economy paradigm, however, goes beyond this definition. It outlines how the country must strategically reshape its economy to achieve long-term, sustainable prosperity. Specifically, the paradigm emphasises: (i) mainstreaming sectors and value chains in the economy that further jobs and economic growth while regenerating/safeguarding the natural capital; (ii) enhancing economic resilience by investing in sectors that would be relevant and thriving in a low-carbon and climate-changed world; (iii) expanding the ‘greening’ of the economy to include sustainability-oriented sectors, such as bio-economy, and nature-based solutions, the circular economy in addition to the energy transition; (iv) building the capacity and skills of the (future) workforce to actively transform the economy from extractive to a regenerative one.

The three green sectors identified are Green Energy Transition (ET), Circular Economy (CE), and Bioeconomy & Nature-based Solutions (BE and NbS). We looked at sectors in the economy that: (i) would further jobs and economic growth while regenerating/safeguarding the natural capital; (ii) would be relevant and thriving in a low-carbon and climate-changed world; (iii) would enable expanding the ‘greening’ of the economy to include sustainability-oriented sectors in addition to the energy transition. We identified the three aforementioned sectors based on the following parameters: (i) growing private sector interest and investment momentum; (ii) evolving policy support as documented in Ministry announcements and policy documents; (iii) the need to explore green opportunities in addition to the renewable energy transition (widening green opportunities across the economic spectrum, from large industries to microenterprises, and from primary sectors to tertiary ones).

ET involves adopting essential renewable energy (RE) technologies that enable a shift towards a decarbonised economy. For our assessment, we identified 16 value chains within ET- across deployment, component manufacturing, industrial decarbonisation and decentralised renewables. For deployment, we included RE technologies such as utility-scale solar, on-shore and off-shore wind, biomass, agri PV, as well as storage technology such as pumped storage hydropower and battery energy storage systems (BESS). For component manufacturing, we identified solar modules, wind components, and batteries. Industrial decarbonisation, ranging from GH2 deployment to the production of two-, three-, and four-wheelers, eBuses, and electric medium and heavy-duty commercial vehicles such as trucks (MHDTs), as well as decentralised renewable energy (DRE)-powered livelihood applications fall within the purview of ET. The sector is pivotal to decarbonising the economy while advancing energy access, advancing local enterprise, employment, and overall economic growth. The CE is a system designed to maximise resource efficiency by minimising waste, promoting maintenance, reuse, refurbishment, remanufacturing, recycling, and reducing environmental impacts associated with resource extraction and disposal. We have identified seven value chains within CE: resource recovery from the organic fraction of municipal solid waste, plastic waste recycling, electrical and electronic equipment waste (e-waste) recycling, lithium-ion battery (LIB) waste recycling, end-of-life vehicle (ELV) scrapping, used cooking oil (UCO) recycling, and used water treatment and reuse. BE is described as an efficient method of transforming and utilising biological resources to generate economic goods, thus fostering revenue growth towards realising a sustainable economy. BE encompasses a broad range of value chains, including biofibers, bio-inputs, bio-residue based packaging, second-generation biofuels, nutraceuticals, and compound cattle feed. While the BE focuses on product-based industries, NbS involves actions like protecting, restoring, or sustainably managing natural ecosystems to create income and job opportunities for local communities (Jain, Jhunjhunwala et al. 2025). It encompasses value chains such as wetland management, seaweed cultivation, sustainable forest management, sustainable tourism, and chemical-free agriculture. Within the combined sector, we have identified 13 value chains which could actualise India’s green transition.

We estimate the job, market, and investment (J-M-I) potential for each of the green value chains by 2047. For jobs, only full-time equivalent (FTE) jobs are calculated, Additionally, for each value chain, we identify challenges to implementation and corresponding recommendations, risks associated with scaling, and a story from the ground to inspire action.

We recommend a comprehensive set of measures to operationalise a green economy in India. These include: improving the economic viability of green solutions through public procurement, blending mandates, tax incentives, and viability gap funding; strengthening raw material supply chains by reducing import dependence, formalising the circular economy workforce, and investing in bio-processing technologies; and significantly boosting domestic R&D and innovation through dedicated funds, private-sector incentives, and regulatory sandboxes for climate technologies. We also call for building a future-ready workforce through industry–academia partnerships, expanded green job certifications, and support for local women-led enterprises in nature-based solutions. Finally, we emphasise the need for stronger standardisation and certification frameworks to improve quality, reduce market fragmentation, and build consumer trust—anchored in a coordinated whole-of-nation (one that integrates green value chains into local, district, state, and national economic planning), whole-of-government (one that aligns ministries, schemes, and regulatory frameworks to accelerate adoption and investment), and whole-of-economy (one that empowers MSMEs, cooperatives, startups, and large industry to participate and benefit, while expanding opportunities for women and youth) approach to scale green value chains across India.

Organic Waste Circular Economy for Viksit Bharat

Roadmap of the methodology to assess the climate co-benefits of the SUP ban in Maharashtra

Financing for Treated Used Water Reuse in India

How Much Does It Cost to Recycle a Solar Module in India?

How Big is the Solar Module Recycling Industry in India?