Council on Energy, Environment and Water Integrated | International | Independent

Suggested citation: Gupta, Saiba, Ayushi Kashyap, Clark Kovacs, Kartikey Chaturvedi, and Nitin Bassi. 2025. Financing Treated Used Water Reuse in India. New Delhi: Council on Energy, Environment and Water.

The growing impacts of climate change are increasing global freshwater scarcity, with cities in the Global South particularly vulnerable to mounting pressure on water resources. Transitioning from a linear to a circular water management approach, where treated used water (TUW) is viewed as a resource, is crucial for enhancing urban water resilience. This report, developed through in-depth analysis and consultation with multi-sectoral stakeholders, estimates the vast economic potential of the circular used water economy in India and provides stakeholder-specific recommendations for implementing sustainable financing mechanisms that move beyond traditional public financial streams to unlock India’s reuse potential and bolster governance frameworks in Indian cities.

India’s used water sector presents an economic opportunity of USD 26–35 billion, encompassing both market potential and investment opportunities by 2047.

The roadmap for mainstreaming circularity in used water management focuses on governance and financing for circular economy solutions. Key aspects of the roadmap include:

Climate change is significantly altering the Earth’s hydrological cycle, intensifying events like floods and droughts worldwide, and increasing their frequency. Freshwater resources are steadily declining globally, with about 2.4 billion people living in water-stressed countries (UN-Water 2023). Cities are particularly vulnerable due to their dense population, putting increased pressure on existing freshwater resources. This complexity calls for adaptation efforts such as improving water use efficiency, and exploring unconventional sources of water like treated used water (TUW). The shift from a linear to a circular model views used water as a resource that can reduce freshwater dependence and improve the water environment, rather than a source of pollution (Tortajada et al. 2025; Gupta et al. 2024). Yet, only 58 per cent of domestic used water is safely treated globally due to inadequate collection and treatment infrastructure, and its high capital and operating costs (WHO and UNICEF 2021). The inability to scale up treatment capacity and meet prescribed effluent water quality standards further lowers the potential for reuse.

Thus, it is crucial to scale up investments in reuse to unlock the economic opportunities within the circular economy of used water. This report discusses various sustainable financing tools, such as scaling up private sector investment, water reuse certificates, municipal bonds, and pricing mechanisms. It provides recommendations for their effective implementation in India, using learnings from successful Indian and global examples. Such efforts can ensure the long-term financial viability of used water treatment and reuse projects.

Beyond the immediate need to meet the rising water demand, mainstreaming the circular economy in urban used water management presents a significant economic opportunity in India:

Unlocking this economic potential requires scaling up investments in reuse, and moving beyond traditional public finance models. We analysed various sustainable financing tools, and are providing stakeholder-specific recommendations for their effective implementation in India (Table ES1). These are based on lessons from successful Indian and global cases, as well as consultations with key stakeholders, including central government agencies, technology solution providers, urban local bodies (ULBs), and industry experts.

Table ES1. From issuing water reuse certificates to unlocking upfront capital—financing models to boost treated used water reuse

| Financing model | Stakeholder-wise recommendations |

|---|---|

|

Cap-and-trade mechanism Water reuse certificates (WRCs): Market-based mechanism that defines reuse targets for bulk water users - those exceeding their targets earn WRCs that can be traded on an open market with those who haven’t met their obligations |

State agencies: (such as state water resource regulatory authorities): Develop a clear regulatory framework that defines roles, responsibilities, and standards to implement the trading schemeULBs: Actively enforce the regulatory framework, and develop city-level TUW reuse plans to identify bulk water users and establish sector-specific reuse targets |

|

Performance-linked financing disbursements |

Central government: Explicitly include TUW reuse in model concession agreements with the private entity |

|

Hybrid annuity model: Public-private partnership model that incentivises private investment in sewage treatment – private entity builds and operates a treatment plant for 15 years, with the central government making performance-based payments, contingent on quality |

Central government and state water utilities: Shift focus to developing, or upgrading to, tertiary treatment capacity, particularly in areas with significant reuse potential for industrial and commercial purposesULBs: Strengthen institutional capacity, including the ability to develop high-quality detailed project reports (DPRs), and integrate TUW reuse/resale as a revenue-generating avenue within the DPRs |

|

Unlocking upfront capital Municipal bonds: Debt instrument issued by urban local body (ULB) to raise upfront capital for infrastructure projects, with repayment linked to future revenue streams |

ULBs: Undertake financial and institutional reforms to meet capital market standards, including strengthening financial discipline for infrastructure development and adhering to disclosure norms, to instil investor confidence for bond issuance |

|

Participation of private end users End-user investment model: Direct investment by end users or ultimate consumers, typically industrial or utility-scale users, to finance and operate used-water treatment and reuse infrastructure |

ULBs/state governments: Enter into long-term, performance-based water purchase agreements with the private end user that guarantee revenue certainty and enable shared riskULBs/state governments: Integrate incentives for end-user participation in city masterplans/TUW reuse plans and state reuse policies |

|

Enabling cost recovery TUW reuse tariffs: Pricing mechanism for TUW to ensure cost recovery for implementing authorities |

ULBs: Implement TUW tariffs that are lower than freshwater rates for equivalent uses, based on treatment levels and users’ paying capacity (e.g., higher tariffs for bulk private users such as industries), ensuring strict adherence to user-specific TUW quality standards |

|

Leveraging technological innovation Appropriate treatment technologies: that enable resource recovery, operational efficiency, and financial viability |

with support of central government and collaboration with technology providers: Promote the adoption of localised, site-specific decentralised used-water treatment systems (to complement centralised treatment) and multifunctional technologies for resource recovery (e.g., bioenergy, nutrient accumulation), and support IoT-based sensing and AI start-ups for improved operations |

Source: Authors’ analysis

We make the following recommendations to accelerate the integration of a circular approach to used water management in water resources planning in India:

Climate change is compounding the disruptions in traditional water availability patterns through increased intensity, duration, and frequency of hydrological extremes (GCEW 2023). Freshwater resources are steadily declining globally, with about 2.4 billion people living in waterstressed countries (UN-Water 2023). The Global South is particularly impacted, with India being exceptionally vulnerable to climate extremes. An analysis of climatic disasters in India between 1971 and 2020 reveals that roughly 75 per cent of its districts are prone to severe hydrometeorological hazards. Nearly 40 per cent of these districts exhibit a ‘swapping pattern’, alternating between drought and floods (Prabhu and Chitale 2024). Further, India is also projected to have the world’s largest urban population facing water scarcity by 2050 (He et al. 2021; Eckstein et al. 2018).

This complexity calls for adaptation efforts such as improving water use efficiency and exploring unconventional sources of water, to enhance urban water resilience. Reusing treated used water (TUW) offers one such globally recognised solution to mitigate water stress (UNEP 2023). This shift from a linear to a circular model views used water as a resource that can reduce freshwater demand for non-potable purposes and improve the water environment, rather than a pollution source (Tortajada et al. 2025; Gupta et al. 2024). Even so, only 58 per cent of domestic used water is safely treated globally, with large variations reported across regions (WHO and UNICEF 2023). For instance, 86 per cent of domestic used water is safely treated in Europe and North America, as opposed to 24 per cent in central and southern Asia (WHO and UNICEF 2023). Amongst South Asian countries, India generates the most used water, with its urban areas alone producing 72.4 billion litres of used water (urban domestic sewage) daily. India has the installed capacity (as of 2021) to treat 44 per cent of this sewage, but only 28 per cent is actually treated. Many sewage treatment plants (STPs) do not function at maximum capacity or do not meet the prescribed effluent water quality standards (CPCB 2021), further lowering the reuse potential in Indian cities. A significant reason for underutilisation is the incomplete sewerage network, which often doesn’t cover unauthorised colonies and suburban areas. Furthermore, urban utilities are unable to expand treatment capacity due to the high capital and operating costs associated with used water infrastructure. According to the CEEW’s Municipal Used Water Management Index, over 80 per cent of the 503 Indian ULBs in states with a reuse policy fail to reuse their TUW or lack any functional treatment infrastructure (Gupta et al. 2024).

Scaling up investment in used water treatment and its subsequent reuse presents an economically viable approach, as the long-term benefits of mitigating economic losses due to increasing water scarcity and declining water quality far outweigh the cost of treatment (Khemka & Eberhard 2025). In addition to water reuse, resource recovery, such as fertilisers, bio solids, and energy, can create new value chains and economic opportunity across various sectors. Urban centres, characterised by concentrated populations, high rates of water consumption, substantial used water generation, and intensive economic activity, represent optimal environments for integrating circular water management in water resources planning, which can unlock significant economic opportunity.

The urban domestic used water value chain begins with the generation of domestic effluent (from toilets, kitchens, bathing and washing), which is collected and transported through a piped sewerage network to sewage treatment plants (STPs). Used water treatment involves one or more processes of primary, secondary, tertiary, and advanced levels of treatment. The Government of India’s National Framework on Safe Reuse of Treated Water (SRTW) aims to achieve 100 per cent sewage treatment and based on the level of treatment, the framework promotes reuse for non-potable applications such as landscaping, industrial uses, road cleaning, construction, and agriculture. Further, 12 Indian states have developed a dedicated policy on the safe reuse of TUW (NMCG 2022). It is important to note that while state policies play a facilitating role, the impetus for implementing used water treatment and reuse lies in the action plans, guidelines, and projects realised at the ULB level (Gupta et al. 2024). This report estimates the economic opportunity in reusing TUW (domestic sewage) in urban India, and presents suggestions on sustainable financing tools that can be adopted by ULBs to ensure the long-term financial viability of used water treatment and reuse projects. It then provides recommendations for strengthening governance, and fostering a market for reused water in Indian cities, thereby enabling a circular economy in used water management.

First, we estimated the installed domestic used water treatment capacity in India for 2025 using the compound annual growth rate (CAGR) in installed treatment capacity from 2021 to the national target of 100 per cent treatment of generated used water in 2045 (CAGR of 3.5 per cent per annum). We accessed the latest data on state-wise installed sewage treatment capacity from the Central Pollution Control Board, Government of India (CPCB 2021). The installed treatment capacity for 2047 was estimated using the national target of 100 per cent used water treatment by 2045 (NMCG 2022).

Estimates for used water generation are based on urban population projections, using data from the Ministry of Housing and Urban Affairs (2019). It was considered that 80 per cent of water supplied to domestic users in urban areas returns as used water (CPCB 2021). Next, we estimated the amount of TUW that will be available for reuse in the industrial and irrigation sectors. This was done by apportioning the installed treatment capacity based on the ratio of current and projected water demand for the irrigation and industrial sectors. For the projections we used the water demand growth estimates of the Ministry of Water Resources (MoWR 1999), Government of India.

The market value of TUW refers to the revenue that can be generated from the sale of TUW to different sectors. For the industrial sector, we used an average of existing industrial TUW tariffs in Indian cities (Ahmedabad, Bengaluru, Chennai, Ghaziabad, Surat, and Visakhapatnam), which is INR 51.37 per kilolitre. To estimate potential revenue in the irrigation sector, we used the TUW reuse tariff of INR 20 per kilolitre as per the National Mission for Clean Ganga, Government of India (NMCG 2022). For each sector, we then multiplied the relevant tariff rate by the estimated volume of TUW that can be reused by each sector in 2047.

To compute the number of full-time equivalent (FTE) jobs required for the maintenance of used water treatment plants, we estimated India’s average treatment plant capacity (22 million litre per day (MLD) as of 2021) and computed the required FTEs for a treatment plant of this capacity using the norm of the Ministry of Housing and Urban Affairs estimates. As per this, a 20 MLD plant requires 18 FTE employees (job coefficient of 0.9) (Tare et al. 2010). The number of jobs likely to be created by 2047 were derived by multiplying the job coefficient with the projected installed treatment capacity. However, with technological advancements and the increasing adoption of process automation, the FTE requirements may fluctuate in the coming years. This shift will likely necessitate new types of training and skill sets for treatment plant maintenance.

Further, we estimated national scope 2 greenhouse gas (GHG) emissions for the top five most commonly used water treatment technologies in India by multiplying the installed treatment capacity of each technology, as per the Central Pollution Control Board, with the electricity emission factor, provided by the Union Ministry of Power, and the average electricity requirement per day (CPCB 2021; Ministry of Power 2023; Bassi et al. 2022).

Finally, we estimated the capital expenditure and annual operations and maintenance (O&M) costs for the infrastructure that needs to be developed to meet national used water treatment targets. Capital costs for constructing secondary- and tertiary-level treatment plants across commonly used technologies were calculated through a 30- year life-cycle cost assessment (including the cost of land) using the net present value approach. This was based on estimates from the Central Public Health and Environmental Engineering Organisation (CPHEEO), Government of India (Tare et al. 2010). Similarly, annual O&M costs were estimated by averaging secondary and tertiary treatment O&M costs per MLD using estimates from the CPHEEO, which were adjusted for inflation, and multiplying them by the estimated national treatment capacity for 2047 (Tare et al. 2010). This is inclusive of the cost of electricity, input requirements, maintenance, and labour wages.

We analysed various sustainable financing tools that can be adopted by Indian ULBs to scale up investments in reuse and move beyond traditional public finance models. We began by assessing their current status and applicability within the Indian context. Based on insights from successful domestic and international case studies, along with extensive consultations with key stakeholders (Figure ES1), including central government agencies, ULBs, technology providers, and experts, we then developed actionable strategies for the effective implementation of these financing mechanisms across India.

Beyond the immediate need to meet the rising water demand, scaling up used water treatment and reuse presents significant economic opportunities. In this section, we estimate the potential market value, job creation, and environmental co-benefits from TUW reuse through 2047. We then estimate the investment required for the sector to realise this economic opportunity.

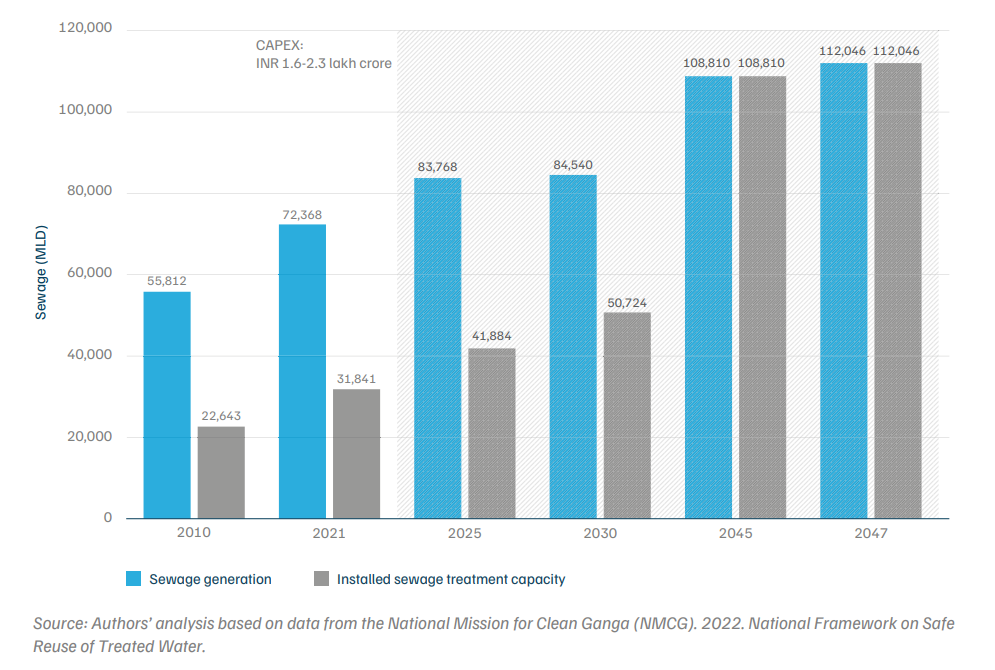

As per our analysis, India has an installed used water treatment capacity of approximately 41,884 MLD as of 2025. This is projected to rise to an estimated 112,046 MLD by 2047 (Figure 1), a three-and-a-half-fold increase over current levels. Boosting used water treatment and promoting its safe reuse offers a significant economic opportunity, if there is a mechanism in place to sell TUW of prescribed quality to different categories of users. We estimate that 31,265 million cubic metres (MCM) (1 MCM = 1000 million litre) of TUW will be available for reuse in the industrial and irrigation sectors by 2047. Across these two sectors alone, the combined average annual revenue through the sale of TUW could reach INR 72,597 crore (USD 8.35 billion) by 2047. However, we suggest that, of the total TUW available for reuse, 50 per cent be utilised to meet the demand of the irrigation and industrial sectors, and the remaining used to contribute to environmental flows in non-monsoon months. Not captured by these estimates is the multitude of other revenue-generating reuse avenues available for TUW, including the recovery and sale of biogas, nutrients, and bio solids.

Figure 1. Achieving India’s 100% used water treatment goal necessitates more than 3x the current installed treatment capacity by 2047.

Scaling up the TUW reuse sector will enable the creation of jobs for maintaining used water treatment infrastructure. If national targets for growth in the water treatment sector are met (section 2.1), over 100,000 employees will be required by 2047 for maintaining sewage treatment plants. Additional jobs will be generated to facilitate the construction of sewage treatment plants, pump stations, and conveyance infrastructure.

Enhancing the reuse of used water treatment will also generate various environmental co-benefits, including emission reductions and greater energy efficiency. Used water primarily releases two potent GHGs, methane and nitrous oxide (Shrof et al. 2022). Globally, the discharge of untreated used water has been correlated with higher methane emissions in urban areas. A lack of used water treatment in urban centres worldwide contributed an estimated 5–10 per cent of global methane emissions in 2023 (De Foy et al. 2023).

There are two categories of treatment technologies— aerobic and anaerobic, in which microorganisms break down organic matter either, with and without the presence of oxygen, respectively. Aerobic treatment plants generally require significantly more electricity, and no methane is generated when it is properly managed. In contrast, anaerobic plants often require less energy, and methane is released during treatment (Shrof et al. 2022). The methane released can be recovered through technological interventions, and utilised as a source of energy for the treatment plants. For example, at the As-Samra used water treatment plant in Jordan, methane biogas recovery is the source of approximately 60 per cent of the total energy used during treatment (Samra Water Resources, 2020). However, if methane recovery is not possible, anaerobic treatment plants become GHG emission hubs, which necessitates the implementation of aerobic technology as an alternative.

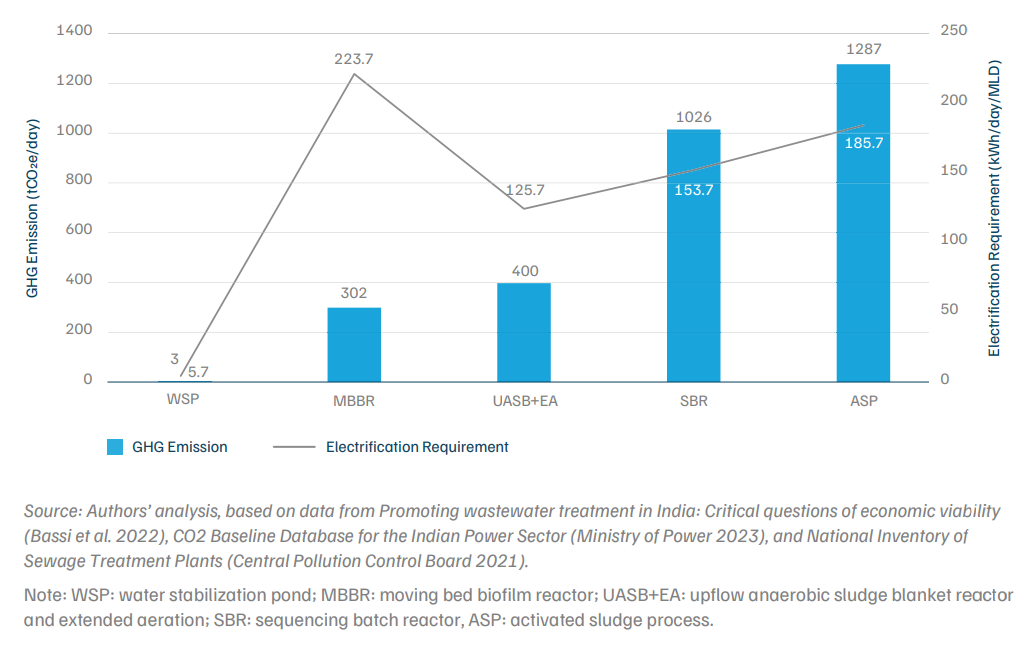

Our analysis indicates that activated sludge process (ASP) and sequencing batch reactor (SBR) technologies, are the two largest aggregate sources of scope 2 emissions in India by way of their energy consumption (as of 2021) (Figure 2), mainly due to their larger penetration in comparison to other electro-mechanical used water treatment technologies. Though the moving bed biofilm reactor (MBBR) has the highest energy footprint among all the technologies assessed, as it represents a small portion of the overall scope 2 emissions due to its low penetration in India. Of the most common treatment technologies, water stabilisation pond (WSP) and upflow anaerobic sludge blanket reactor and extended aeration (UASB+EA) technologies, have the lowest energy requirements (Figure 2). Therefore, prioritising the implementation of less energy-demanding technologies such as WSP and UASB+EA, along with the deployment of methane recovery technologies, will significantly reduce scope 2 GHG emissions and transform treatment plants into a source of energy. However, technologies such as WSP have a high land footprint, and will be more feasible in cities where land is not a constraint as yet.

Figure 2. Sequencing Batch Reactor (SBR) and Activated Sludge Process (ASP) are the used water treatment technologies with the highest Scope 2 emissions in 2021

There is a need to scale up investment in India’s used water treatment infrastructure to unlock the economic opportunity offered by TUW reuse. To meet the national used water treatment targets (section 2.1), treatment capacity needs to be enhanced by over 70,000 MLD by 2047 (NMCG 2022). The cost of constructing this capacity will depend on the type of technology and the level of treatment (secondary or tertiary), required in each local context. We estimate the total investment needed between 2025 and 2047, at current market value, to range from INR 1,56,494 crore–2,31,050 crores (USD 18–27 billion). The average annual O&M costs for treatment plants at the national level are estimated at INR 15,406 crore (USD 1.8 billion) by 2047.

India’s used water circular economy presents an over 26-35 billion-dollar opportunity over the next two decades (section 3). Unlocking this potential requires scaling up investments in reuse, and moving beyond traditional public finance models. In this section, we discuss various sustainable financing tools and outline strategies for their effective implementation in India. Such efforts can foster a market for reuse and support cost recovery for implementing authorities.

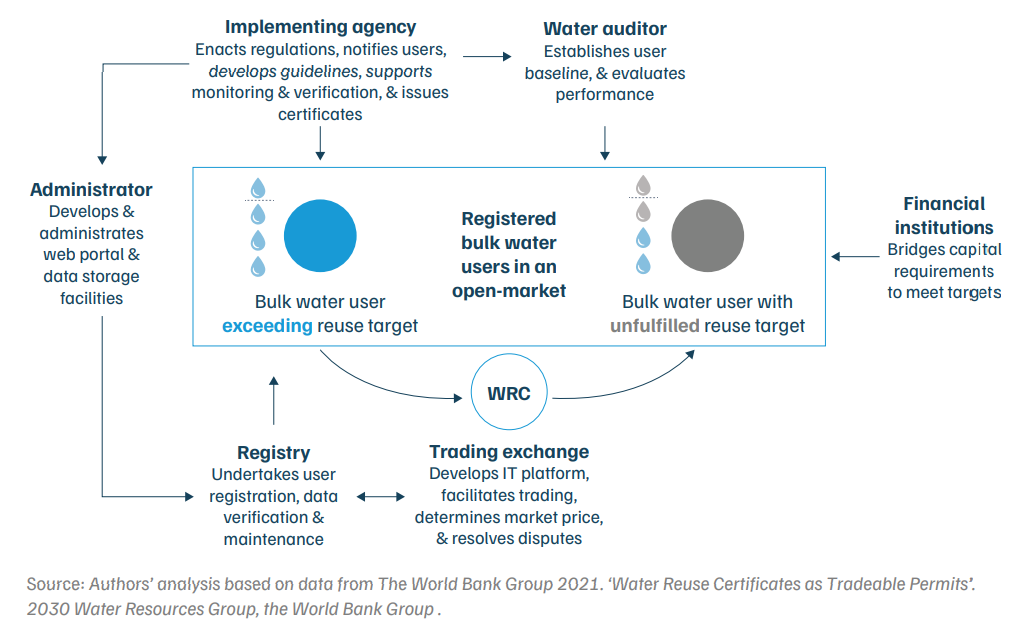

Water reuse certificates (WRCs), a model developed by the 2030 Water Resources Group, operate as a cap-andtrade policy instrument. This market-based mechanism aims to drive target-based TUW reuse among bulk water users. Under a regulated approach, an implementing agency identifies and sets individual reuse targets for bulk water users across municipal, industrial, and agricultural sectors. Users who exceed their stipulated targets earn WRCs, which can then be traded in an open market to those failing to meet their obligations. This dynamic not only optimises financial resource allocation, but the positive reinforcement through target achievement also stimulates technological innovation and process improvements in used water treatment, attracting vital additional finance. The institutional mechanisms may vary depending on the geographical context, but, largely, the actors showcased in Figure 3 should be involved in setting up the WRC system.

Figure 3. How water reuse certificates (WRCs) work.

Enablers for the successful implementation of water reuse certificates (WRCs) in India

The WRC model is typically structured in three-year phases involving baseline establishment (assessing water consumption and reuse patterns of identified users), reuse target implementation (where the users undertake measures to achieve the reuse targets), and assessment for issuance and trading (where user performance is independently assessed for issuance and trading of WRCs). For India, critical prerequisites for its successful implementation include:

Strategy for effective WRC implementation in India

The adoption of WRCs in India can draw valuable lessons from similar cap-and-trade models implemented globally and domestically.

The Implementation of the WRC scheme in India may face the following challenges:

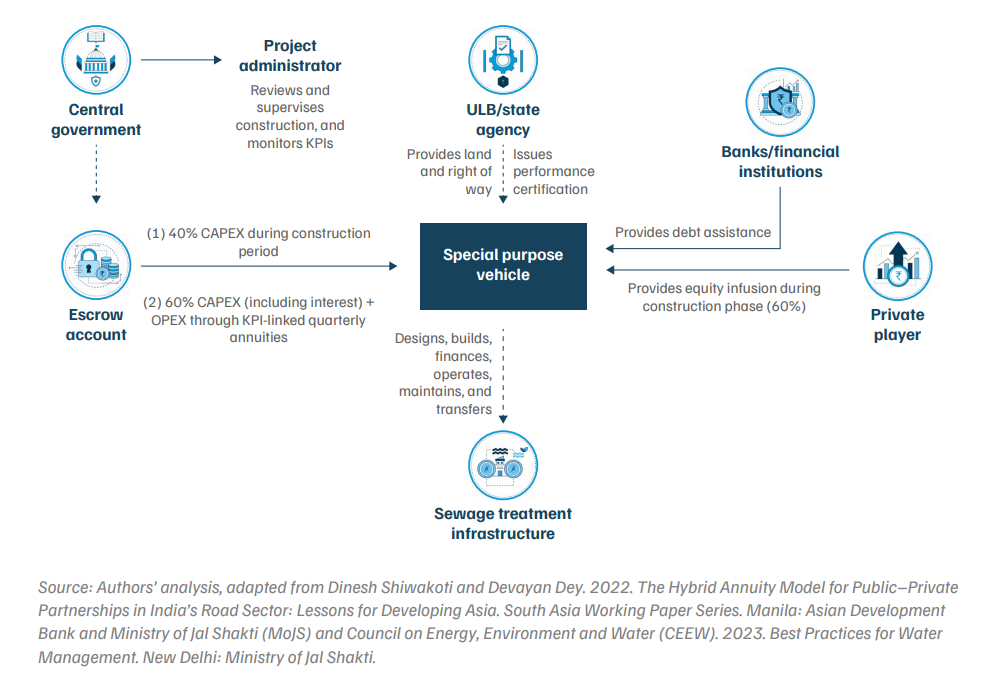

The Government of India’s Hybrid Annuity Model (HAM) is a PPP initiative that offers assured government funding for the development of used water infrastructure, and its operation and maintenance for a specific period. It ensures sustained infrastructure performance through shared risks and clear accountability for the private entity. The central government provides 100 per cent funding, infusing 40 per cent of the project capital cost during the construction period, and disbursing the remaining 60 per cent along with O&M expenses over 15 years as quarterly performancelinked annuities (MoJS and CEEW 2023). The private entity is responsible for the asset’s construction and O&M. In combining the central government’s financial support with the technical competence of a private player, HAM delivers a more balanced solution to used water infrastructure development. It is implemented through a tripartite agreement between the central agency (National Mission for Clean Ganga), the state government or ULB, and the private player or concessionaire (Figure 4):

Figure 4. The Hybrid Annuity Model (HAM) Public-Private Partnership (PPP) balances the financial risk between public and private players

Leveraging The Hybrid Annuity Model (HAM) Public-Private Partnership (PPP) for a circular used water economy

As of date, 32 STPs have been developed in India with a total investment of over INR 110 billion. The plants are in the five states on the main stem of river Ganga: Uttarakhand, Uttar Pradesh, Bihar, Jharkhand, and West Bengal (MoJS and CEEW 2023). However, TUW reuse is yet to see widespread integration into HAM–PPP projects. Here are recommendations for leveraging HAM–PPP to maximise TUW reuse:

The implementation of the HAM-PPP model to increase the reuse of TUW may be limited by:

In India, financing of ULBs is structured around a mix of ownsource, grants transfer, and borrowings. Between financial year (FY) 12 and FY18, on average, ULBs generated around 50 per cent of their total revenues independently, while grants transfer accounted for 40 per cent of total revenue, and borrowings were limited to ~10 per cent. Proceeds from bonds accounted for only ~5 per cent of the borrowings (Bibhudatta and Rathee 2025).

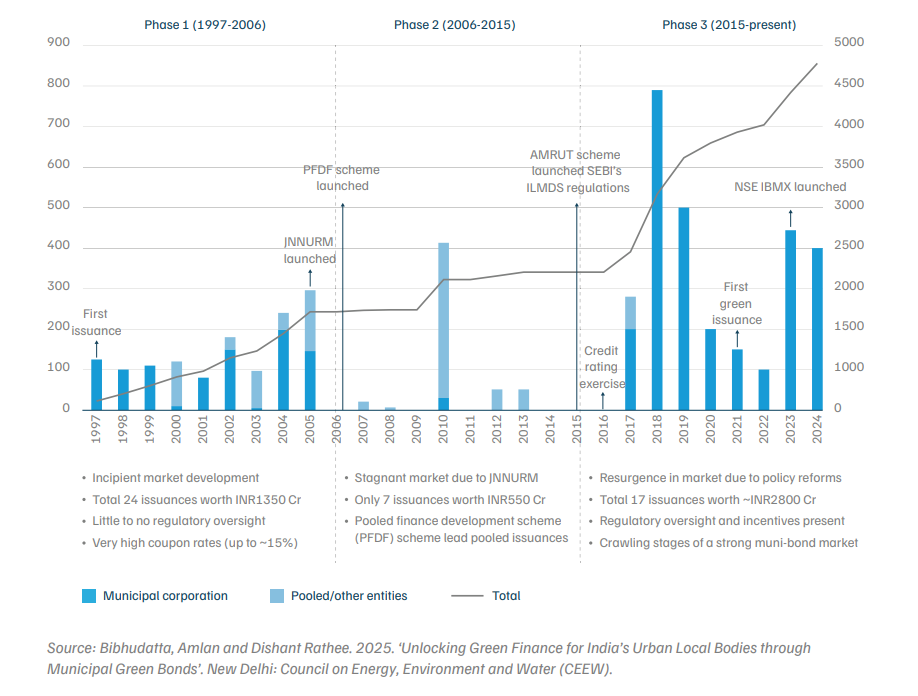

Nevertheless, despite having diverse funding sources, municipal expenditures by Indian ULBs contribute only around 1 per cent of India’s GDP, which is significantly lower compared to some BRICS nations such as Brazil (7.4 per cent) or South Africa (6 per cent) (RBI 2022). This is primarily attributed to poor financial management, overdependence on central and state grants transfers, and weak financial autonomy. These challenges spurred the exploration of alternative methods to fund urban infrastructure in the early 1990s. In this context, municipal bonds have emerged as a promising debt-financing tool. Bengaluru became the first municipal corporation to issue municipal bonds in 1997. In 2025, the Pimpri-Chinchwad municipal corporation issued a first-of-its-kind green municipal bond that aimed to raise INR 200 crore to support Harit Setu, a sustainable transportation initiative.

Municipal bond market in India

A municipal bond is a debt instrument issued by a ULB to raise upfront capital for infrastructure projects, with repayment linked to future revenue streams. Under this model, ULBs access capital markets by pledging predictable cash flows such as user charges, property tax collections, or water tariffs to service the debt over time (GoI 2017). This enables cities to finance and implement large-scale service delivery projects without solely relying on the grants of the central and state governments.

India’s municipal bond market has evolved through three key phases (Figure 5). The early development phase saw 17 ULBs raise INR 1,350 crore through the issuance of 24 bonds, though at high coupon rates (up to 15 per cent) due to the ULBs’ weak financial systems and a lack of standardised regulation. The limited activity phase during the implementation of the central government’s erstwhile Jawaharlal Nehru National Urban Renewal Mission (JNNURM) from 2005 onwards saw a decline in bond issuances as the scheme envisaged total investment of about INR 1 lakh crore (CCIL 2024) available to ULBs in the form of grants from the Centre. The incentive-driven phase post2015 witnessed renewed surge in the bond market. This was driven by proactive policies anchored by the central government such as the Atal Mission for Rejuvenation and Urban Transformation (AMRUT) scheme, launched in 2015, that introduced financial incentives in the form of a lumpsum grant-in-aid for municipal bond issuances at a rate of INR 13INR 13 crore per INR 100 crore) of bonds (MoHUA 2025). The Smart Cities Mission, also launched in 2015, pushed for private financing, and led to the issuance of bonds worth INR 2,800 crore issued at average coupon rates of 8.5 per cent (Bibhudatta and Rathee 2025). Moreover, the Securities and Exchange Board of India’s (SEBI’s) Issue and Listing of Municipal Debt Securities (ILMDS) regulation in 2015 (SEBI 2015) compelled ULBs to maintain high standards of transparency, creditworthiness, and fiscal discipline, which instilled confidence in investors.

Figure 5. The municipal bond market in India has evolved in a non-linear fashion over the years

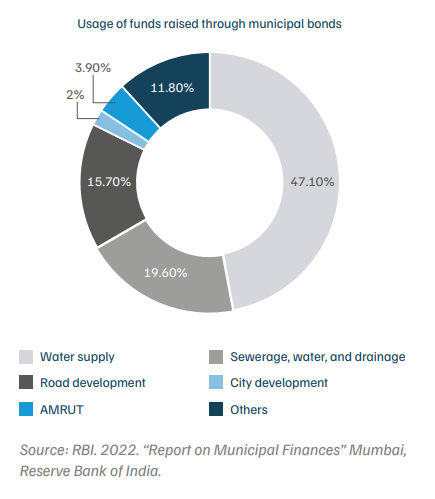

Proceeds from municipal bonds in India have almost exclusively been used for capital expenditures and/or expansion of essential municipal services. Most issues have been used to finance water supply, sewerage, and road construction works (Figure 6).

Figure 6. Over 50% of municipal bond proceeds have financed water supply and sewerage projects

Leveraging municipal bonds to finance TUW reuse projects

Municipal bonds offer ULBs a reliable alternative to public finance, helping them bridge funding gaps and independently finance capital-intensive projects in the following ways:

Challenges of using municipal bonds for TUW reuse

While municipal bonds have emerged as a promising tool for financing urban infrastructure, their applicability for TUW reuse projects remains limited due to the following reasons:

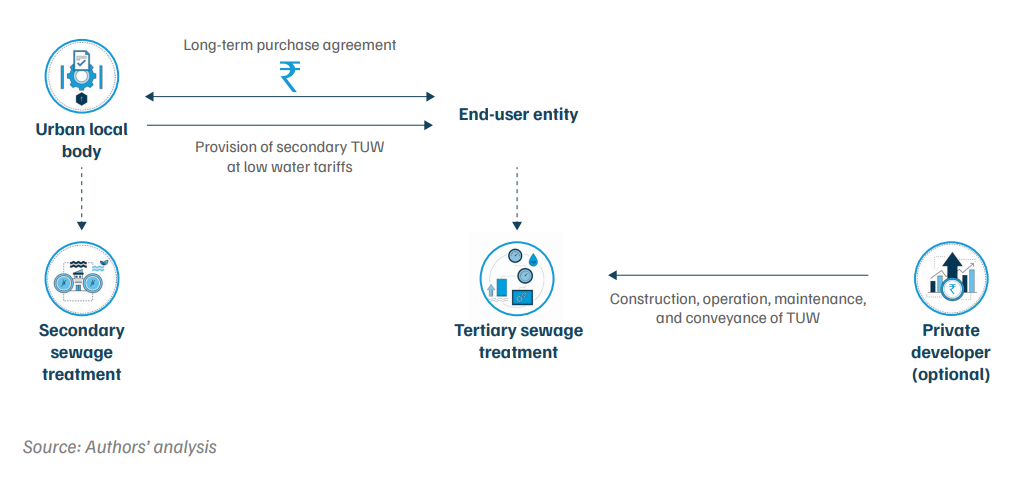

The end-user investment model enables direct investment by the end users or ultimate consumers, typically industrial or utility-scale users, to finance and operate used water treatment and reuse infrastructure (Fouad et al. 2021, FICCI and 2030 WRG 2016). The model ensures revenue certainty and project ownership through long-term offtake arrangements. For instance, the Maharashtra State Power Generation Co. Ltd. (MAHAGENCO), a large power generation company, partnered with the Nagpur Municipal Corporation (NMC) under a 30-year build-operate-transfer (BOT) end-user contract where the latter agreed to provide the raw used water, and MAHAGENCO agreed to be in charge of transportation and treatment. The contract involved investment of INR 195 crore in a 130 MLD STP to supply TUW for power generation, saving costs and securing water supply (MAHAGENCO 2020). Similarly, the Chennai Petroleum Corporation Ltd. (CPCL) financed its tertiary treatment facility to process 24 MLD of secondaryTUW from the Chennai Metropolitan Water Supply and Sewerage Board (CMWSSB) (World Bank 2020), saving costs of industrial freshwater tariffs in the long term for CPCL.

This model is implemented through an arrangement between the ULB, the end user, and the private developer or operator (optional) (Figure 7). Their roles are as follows:

Figure 7. The end-user investment model allows direct investment from final consumers and provides revenue certainty through long-term offtake agreements

Leveraging the end-user investment model for a circular used water economy

The end-user investment model offers a unique opportunity to drive circularity by shifting the capital burden of infrastructure from public agencies to bulk water users. It can unlock a sustained reuse market across sectors in the following ways:

Limitations of the end-user investment model

The end-user investment model has demonstrated potential in select industrial contexts by leveraging private capital for TUW reuse. However, its scalability remains a major challenge.

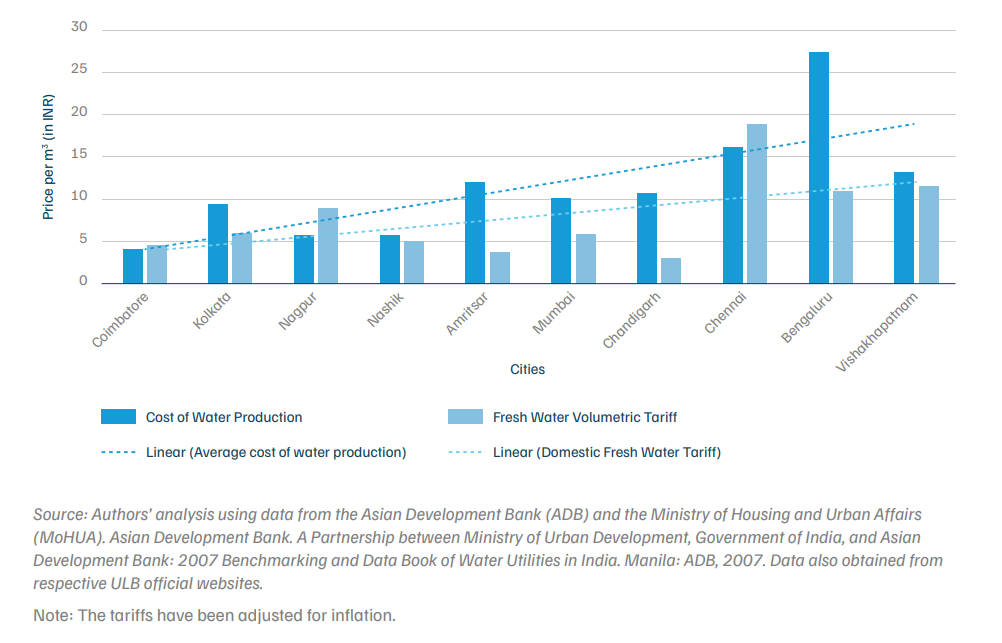

Our analysis indicates that the average annual O&M costs for commonly deployed treatment technologies in India (including energy, inputs, and salaries) ranges INR 10–18 lakh per MLD, with advanced technologies leading to higher costs for maintaining functions and effluent quality. Low cost recovery by water utilities puts the operational efficiency and economic viability of these infrastructure projects at risk. Beyond physical and institutional bottlenecks, a more fundamental problem persists: a widespread failure to recognise water’s full value in policy, pricing, and investment decisions. Water is largely treated as a free or low-cost input, rather than a scarce, vital resource. This undervaluation leads to overuse, inefficiency, and underinvestment.

We compared the cost of production (per cubic metre) with the domestic fresh water tariff (per cubic metre) levied across 10 metropolitan Indian cities (Figure 8). The general trend indicates that, in most cities, the cost of water production exceeds the water tariff charged to consumers, highlighting a financial imbalance in water supply operations. In order to sustain a demand for TUW, freshwater prices need to reflect its true value, with alternative supplies priced competitively.

Figure 8. The cost of water production exceeds domestic water tariffs in 7 of 10 Indian cities

For instance, in Bengaluru, industrial consumers receive secondary TUW at INR 25/KL, significantly lower than the freshwater rate of INR 90/KL. Surat currently supplies tertiary-TUW to industries at a competitive price of INR 36/KL compared to the freshwater price of INR 39/KL. In adopting a revenue-driven approach to the sale of TUW, one of its STPs was able to generate INR 233 crore between November 2014 and July 2021 (CPHEEO 2021).

Recommendations for an effective tariff structure for TUW

The landscape of used water pricing policy in India is relatively new, evolving through gradual developments across different levels of governance. A national-level framework on the safe reuse of treated water provides guiding principles, while state-level reuse policies, introduced in 12 out of 28 states, establish region-specific pricing structures. Implementing authorities, which may be the ULBs, state agencies, or SPVs, should design TUW tariffs keeping in mind the following objectives:

The technology selection and deployment for used water treatment often lack feasibility assessment and operational efficiency, respectively. In the absence of financial and technical capabilities, ULBs are often compelled to choose inefficient, often the least costly, technologies over the most efficient, compromising environmental performance (Niti Aayog 2022).

Technology innovation is being driven by the penetration of international market players, as well as by the Indian start-up ecosystem that is targeting small-scale applications to tap into the used water economy. This can be leveraged to improve used water treatment, and increase resource recovery, all while maintaining the financial viability of such projects. Such initiatives in the used water management domain can benefit from the establishment of dedicated platforms supported by the government, attracting a larger base of investors and reaching new geographies. The following are some big-bet technological solutions that can be mainstreamed in India:

Decentralised treatment technologies

Upgrading technology to meet end-use-specific quality requirements in centralised treatment systems often incurs high costs without sufficient revenue streams, increasing the risk of sunken costs and increased operational burdens for the managing entity. In contrast, the site-specific nature of decentralised used water treatment systems enables designs tailored to techno-socio-economic feasibility, considering both the effluent’s characteristics and the intended end use of the TUW (Kumar and Tortajada 2020). As opposed to CAPEX-heavy centralised treatment, decentralised systems offer arenas for phased investments and quicker adoption of technology based on the specific needs of urban areas (Niti Aayog 2022).

Innovative decentralised technological solutions are being localised to solve chronic issues in the sector. For example, Indra Water successfully employs a patented, modular, electrically driven technology using a plug-andplay model within industrial, residential, and commercial settings. Through its smart, optimised, and space-efficient technology, Indra Water has been able to achieve a best-in-class cost per kilolitre and generate revenue by charging a user fee through the sale of TUW. In Tamil Nadu, JSP Enviro employs its modular microbial fuel-cell (MFC) based technology to supplement conventional technologies in targeting heavy metal contamination. Demand for such technologies is notable in industries and regions facing space limitations or freshwater scarcity. This innovation space must be appropriately fostered by well-crafted policy nudges and government support to boost investor confidence and enable wide-scale adoption. Knowledge institutions that serve as pilot incubators can be financially supported to scale up promising technologies and create government buy-in. Established companies with large market shares can collaborate with start-ups to initiate technology pilots and provide market access. By strategically combining the economies of scale offered by centralised infrastructure with the localised advantages of decentralised solutions, cities can effectively minimise the discharge of unsafe sewage while simultaneously maximising economic gains from resource recovery and efficient management.

Multifunctional technologies

The current treatment approach is linear, in that it only views used water as an end-of-pipe pollution source. The treatment process must evolve to extract maximum value from used water, which can not only generate revenue but also save resources. The integration of energy recovery, resource recycling, and clean water production aligns with global trends towards sustainability and resource efficiency (Pott et al. 2017).

The choice of technological solution must therefore be informed by its ability to recover valuable resources. The installation of new STPs must not only meet installed capacity targets, but also be aimed at creating new revenue streams from the sale of TUW and other resources recovered from the process. The adoption of newer multifunctional technologies—i.e., technologies that, apart from used water treatment, aid in saving or extracting valuable products—must be encouraged. Technologies like MFC that produce bioenergy, nutrient-accumulating nature-based treatment, electro-chemical based reactors, energy-saving Ubox, or microbubble technology can be commercialised, along with the more mainstream technologies such as energy-saving UASB + EA or resourceand-time efficient advanced oxidation processes (AOP). The selection of technology must not only be done on the basis of the lowest cost, but be supported by a market analysis of potential by-products and a techno-economic feasibility assessment. In existing secondary STPs, technology upgradation must be prioritised to extract products with a clear market demand and applicability to increase the profitability of water utilities.

Soft technological solutions

Data and information play a crucial role in overcoming operational barriers to maintain the vast and expanding network of sewage infrastructure. Digital public infrastructure must be extended to the used water sector to transform the current fragmented and unreliable data systems into a centralised system that facilitates operational transparency, better quality control, and proactive resource allocation. Leveraging tools such as digital mapping technologies or supervisory control and data acquisition (SCADA) platforms to monitor plant functioning can help increase the reliability of monitoring data and responsiveness against operational failures.

While the use of digital technology in this domain is still nascent in India, there has been some advancement in the creative use of software—even artificial intelligence—to improve operational efficiency and monitoring for better service delivery. Digital Paani, a Gurugram-based startup with pan-India operations, goes beyond conventional SCADA systems to integrate IoT-based sensing technology, aiming for operational efficiency to optimise the overall workflow. Another profitable start-up called TankerWala, based out of Bengaluru, is using a mobile app as a platform to deliver TUW from STPs via tankers for real-estate and infrastructure construction activities (TankerWala 2023). It offers operation-optimisation for independent suppliers, and locality-based pricing for all customers. Many such technology and service-based start-ups are in an incubation phase, and must be supported with the necessary funding to achieve scale and recognition.

Challenges in leveraging technological innovations

While innovative technological solutions are crucial levers to advance a circular economy within the used water sector, they face the following barriers in adoption:

This report provides an actionable framework for deploying various financing tools at the ULB level to ensure the sustainable implementation of used water treatment and reuse projects (Section 4). While cities like Surat, Chennai, Nagpur, Udaipur, and Ahmedabad have demonstrated successful financing models for reuse projects, these initiatives have yet to become mainstream at the national level. To address this, we make the following recommendations to scale up finance in TUW reuse:

Reuse plans should include:

The financial feasibility of reuse projects is crucial for their sustainable implementation.

To achieve this, state governments and ULBs should take the following key actions:

Key actions for ULBs:

This study targets policymakers, urban local bodies, financiers, and water sector stakeholders. It highlights India's growing water scarcity challenge and presents economic, job, and environmental benefits of scaling reuse of treated used water (TUW). It outlines sustainable financing tools and governance recommendations to mainstream circular water management and ensure the long-term viability of TUW reuse projects.

Financing TUW reuse requires diversified funding mechanisms to ensure the long-term sustainability of reuse projects. Innovative models include Water Reuse Certificates, Hybrid Annuity-based Public-Private Partnerships, municipal bonds, and end-user investment, which are important alternatives to public financing that diversify funding streams.

The integration of a circular economy approach begins with long-term, city-level TUW reuse plans that define clear treatment and reuse targets. These plans must identify suitable reuse avenues, specific quality standards, and appropriate conveyance mechanisms.

ULBs are central to implementing reuse plans, developing pricing mechanisms, leveraging commercial and industrial consumption, and coordinating the development of reuse infrastructure and policies at the city level.

Organic Waste Circular Economy for Viksit Bharat

Roadmap of the methodology to assess the climate co-benefits of the SUP ban in Maharashtra

Building a Green Economy for Viksit Bharat

How Much Does It Cost to Recycle a Solar Module in India?

How Big is the Solar Module Recycling Industry in India?