Council on Energy, Environment and Water Integrated | International | Independent

Suggested Citation: Bajpai, Aryan, Ishita Gupta, Shreya Wadhawan, Pushp Bajaj, and Vishwas Chitale. 2025. Innovative Financial Instruments for India’s Urban Climate Resilience: Success Stories and Learnings. New Delhi, India: Council on Energy, Environment and Water (CEEW).

Cities across India are at the forefront of climate change, witnessing intensifying extreme weather events, such as floods, cyclones and heatwaves, leading to significant economic and non-economic losses every year. Addressing these escalating risks requires upfront capital investment, something most ULBs struggle to finance through their existing revenue streams. Despite the constitutional mandate under the 74th Amendment to perform the 18 functions for urban planning and development, ULBs remain constrained by low fiscal autonomy, limited technical capacity, inadequate financial records, and restricted access to capital markets. These constraints undermine their ability to effectively plan, implement and sustain adaptation actions to build the resilience of city infrastructure and populations exposed to these climate risks.

Recognising this gap, this study compiles and assesses practical and scalable models that can mobilise adaptation finance for building resilient urban infrastructure in India. Drawing on the examples from India and across the world, it highlights instruments such as green bonds, public–private partnerships (PPPs), blended finance, pooled funds, and insurance-based risk management that can unlock capital towards strengthening urban infrastructure. The study highlights four curated case studies: Vadodara’s certified green municipal bond, Climate Insurance-Linked Resilient Infrastructure Financing (CILRIF), the Climate Smart Health Infrastructure Fund (CSHIF), and the Urban Infrastructure Insurance Facility (UIIF), that provide actionable pathways to enhance financial planning and enabling sustainable, climate-resilient urban development.

Cities across India are at the forefront of climate change, witnessing intensifying extreme weather events, such as floods, cyclones and heatwaves, leading to significant economic and non-economic losses every year. As urban areas in India continue to cater to a growing population, the accelerating impacts of climate change pose monumental challenges for urban development and economic growth. It is critical for urban local bodies (ULBs) to integrate risk-informed adaptive strategies into their short-term and long-term planning to minimise vulnerabilities and enhance urban resilience; to safeguard communities, ecosystems, and critical infrastructure; and to maintain economic stability.

Municipalities in India have a defined set of functions, with a wide scope for enabling climate adaptation. However, there are several limitations that restrict the ability of Indian ULBs to finance and implement climate adaptation measures, such as a lack of fiscal autonomy, discrepancies in managing finance through existing revenue streams, a shortage of technical expertise, limited access to capital markets, stringent regulations posed by the central and state governments to levy taxes, set rates, and access capital markets, and poor management of financial records, especially in municipal councils and nagar panchayats. Most ULBs in India do not have estimates for their financial needs for adaptation, or records of current expenditures that are directed towards activities that provide adaptation-related benefits. Without such estimates, ULBs struggle to accommodate the changing climate and the growing infrastructural and service needs in their respective city development plans.

Finance is a key enabler for ULBs to implement climate adaptation actions within the scope of their mandated functions. In India, ULBs have a longstanding history of devising financial solutions to mobilise resources for infrastructure projects, often leveraging partnerships with the private sector. Traditional instruments such as municipal bonds and pooled financing have evolved significantly, facilitating greater access to capital from capital markets. Innovative financial mechanisms that build upon traditional instruments, such as green municipal bonds and pooled insurance financing, are now being piloted, offering new avenues to strengthen sustainability efforts. However, such instruments remain under-utilised in climate adaptation actions.

Infrastructure-based climate adaptation solutions typically require high upfront costs and have lower returns over longer periods of time, making them difficult to finance through existing revenue streams and with limited government aid. Municipalities’ existing revenue streams and the aid they receive from central and state governments are not enough to implement such solutions. Investments from the private sector are thus necessary to bridge the adaptation finance gap. While some municipal corporations have successfully raised capital in this manner, ULBs continue to face barriers in engaging with the private sector. There is thus an urgent need to identify and adopt innovative financial mechanisms, leveraging public-private partnerships (PPPs), to mobilise resources for climate-resilient infrastructure development.

Based on the challenges faced by Indian ULBs in India and the country’s socio-economic profile, this study compiles and assesses best practices and case studies showcasing innovative and practical financial solutions, which are either currently active or have been implemented in the past by ULBs in India and across the world to finance climate adaptation-related and/or infrastructure-based projects, particularly those related to climate-resilient infrastructure. This study will provide actionable insights and scalable models to enhance financial capacities, leverage diverse funding sources, and promote sustainable urban development across ULBs in India. Our selections along with the category-specific challenges identified in this study will guide state governments, municipal corporations, city managers, urban finance policymakers, and private sector actors in identifying and adopting innovative financial solutions for the implementation of climate adaptation measures.

The study identifies several financial instruments employed worldwide by different stakeholders to implement climate action projects. The financial instruments have been classified into three distinct categories of debt-based instruments, financial risk management instruments, and results-based financing instruments, which have the potential to provide ULBs with a range of options to select from, based on their financial and technical capacity and development priorities. These instruments cater to diverse adaptation projects based on their revenue potential and socio-economic conditions. Furthermore, the study also presents four detailed case studies that showcase practical applications of innovative financial instruments:

These case studies provide real-world examples of unique partnership models that mitigate investment risk and engage private capital to scale finance for climate adaptation measures. Based on the unique requirements of each financial instrument, ULBs will need to address institutional and technical barriers and strengthen their financial and technical capacities by improving creditworthiness, and adopting innovative blended finance models. The government must also support ULBs by facilitating collaborations and providing regulatory support for private-sector engagement.

An analysis of the financial solutions collected for the study highlights that most financial instruments used for adaptation finance are debt-based or financial risk management instruments such as bonds, pooled investment funds, etc. Concessional debt, such as blended capital loans and pooled investment funds, alongside insurance mechanisms, is commonly used to mitigate financial risks and build investor confidence. However, there is a global shift from debt-based mechanisms towards financial risk management instruments, as the former can increase financial burdens, particularly for resource-constrained municipalities. In India, given the limited financial capacity of municipalities, risk-sharing mechanisms are more sustainable for adaptation financing. Results-based financial instruments such as green and biodiversity credits offer transparency and accountability, but face challenges such as those related to measuring adaptation benefits, distinguishing adaptation from development activities and limited project pipelines.

In conclusion, Indian ULBs must focus on two priority areas to access private capital effectively:

Additionally, ULBs must be granted greater financial autonomy under the new Indian GST regime to improve their own-source revenue (OSR). At the same time, easing the stringency of procedural and reporting burdens is essential to facilitate ULBs’ access to financial instruments such as municipal bonds and foreign capital markets. Together, these steps will enable ULBs to access the much-needed finance to implement climate adaptation measures, so as to enhance the resilience of urban infrastructure.

The accelerating impacts of climate change continue to pose significant threats to India’s population, critical infrastructure, and economy. A recent analysis by the Council on Energy, Environment and Water (CEEW) found that more than 75 per cent of districts in India, which comprise over 80 per cent of the population, are highly vulnerable to floods, cyclones, and droughts that are being exacerbated by climate change (Mohanty and Wadhawan 2021). Urban areas, in particular, face unique challenges given their high population density, ageing infrastructure, high water and energy demands, and lack of sufficient green spaces (Dookie and Gannon 2022). Additionally, urban areas also contribute 70 per cent of India’s GDP and are projected to attract substantial investments, averaging USD 55 billion annually or 1.2 per cent of the GDP1 (Kouame 2024). To bridge the dual reality of urban areas as both economic powerhouses and climate risk hotspots, ULBs, which are at the forefront of these impacts of climate change, need to develop their technical and fiscal capacity to finance and implement adaptation actions that build the resilience of local communities and infrastructure.

Indian cities are expected to cater to an estimated 630 million people—more than 40 per cent of the total population—by 2030 (Government of India: High-Level Committee on Urban Planning 2023). Accommodating this urban population comes with significant financial demands. The World Bank projects that Indian cities will require USD 840 billion in urban infrastructure investments by 2036 (Athar, White, and Goyal 2021). However, this estimate focuses largely on providing civic services to these cities, and do not account for their need to build resilience against the growing impacts of climate change, which would require significant additional investments.

In recent years, floods have severely impacted Indian cities, particularly coastal cities such as Mumbai and Chennai (Hagare 2024), while inland cities such as New Delhi have witnessed an increase in the frequency and intensity of extreme heat events (Kaul and Lakhera 2024). Such events lead to severe short-term and long-term economic and noneconomic losses as they disrupt livelihoods, damage infrastructure, and can even lead to loss of lives (UNFCCC 2020). For instance, the supercyclone Amphan, which made landfall in West Bengal in 2020, caused damages estimated at USD 14 billion and killed more than a hundred people (WMO 2021). The economic losses were primarily the damage to urban infrastructure and essential services, which highlights the need to build resilience to mitigate future losses.

According to the 2024 State of Cities Climate Finance report, cities in emerging markets and developing economies across the globe will require USD 147 billion annually until 2030 and USD 165 billion annually until 2050 for adaptation (Press-Williams et al. 2024). The Government of India has also recognised the growing need for climate adaptation and estimated that an additional investment of approximately INR 56.68 trillion (USD 700 billion) would be required by 2030 to build the resilience of communities, ecosystems, economy, and infrastructure (MoEFCC 2023a). Even though most of the adaptation-related spending is currently done through public expenditure by the central and state governments, urban local bodies (ULBs) in India—with the exception of a few cities such as Mumbai and Ahmedabad— lack both information on the requirements of adaptation finance as well as any current expenditures directed towards adaptation-related initiatives.

The 74th Amendment Act of 1992 introduced the 12th Schedule under Article 243W of the Constitution and provided a list of 18 functions to be executed by ULBs. However, expenditure by ULBs on these mandated functions has been significantly low. Municipal expenditures in India have stagnated at around 1 per cent of the Gross Domestic Product (GDP) since the late 2000s (Chakravarty and Priya 2025; RBI 2022). This is significantly lower than other Global South countries, such as Brazil (7.5 per cent of GDP) and South Africa (6 per cent of GDP) (IMF 2016; RBI 2022). With adaptation funding remaining insufficient, ULBs face challenges, lacking the financial resources and institutional capacity to scale up climate adaptation measures effectively.

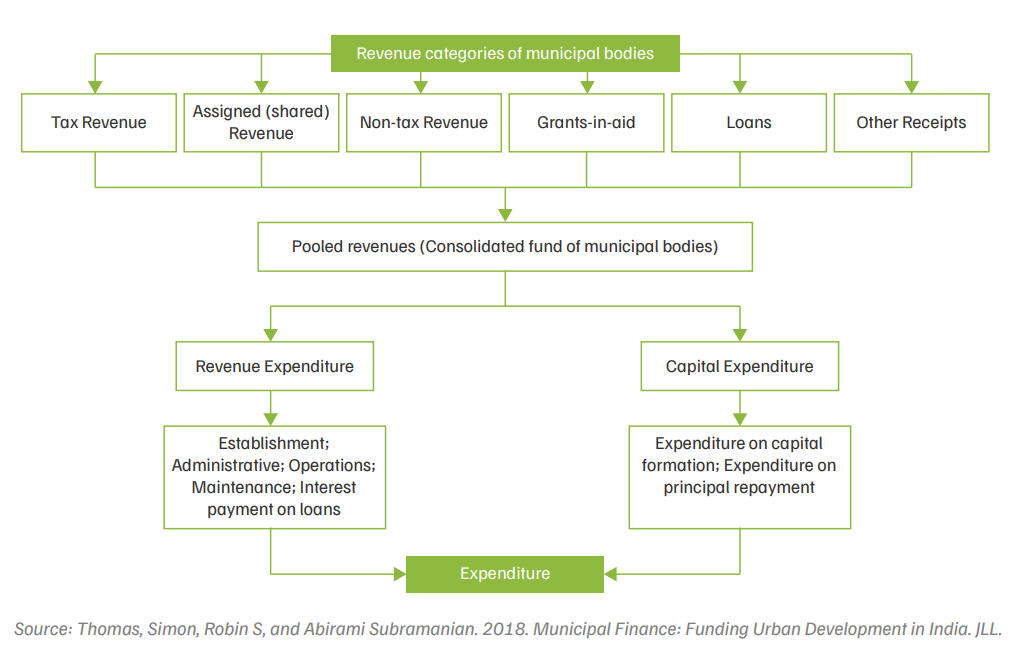

As highlighted in Figure 1, ULBs earn revenue through several different sources. Article 243X of the Constitution empowers state governments to impose taxes, duties, tolls, and fees, and to assign revenues from specific sources to ULBs. However, ULBs have seen a decline in their capacity to generate their own revenue in recent years. This is largely due to over-reliance on property tax, challenges faced due to GST implementation, under-utilisation of land-based financing, and limited non-tax revenue-based sources. Moreover, property tax, intended to be a major source of municipal revenue, faces several challenges, including property undervaluation and incomplete property registers, policy inadequacy and ineffective administration, and pending litigations and staffing shortages within ULBs (RBI 2022).

Figure 1. Revenue and expenditure streams of municipal finance in India

Article 243Y of the Constitution assigns State Finance Commissions (SFCs) the responsibility of reviewing and recommending the devolution of tax revenues and grants-in-aid to ULBs. However, effective devolution and transfer of these revenue sources have been limited (RBI 2022). State governments often do not set up SFCs at the mandated five-year intervals. Even when constituted, SFCs take an average of 32 months to submit their reports, leading to delays in fund allocation. Once the reports are submitted, state governments take a significant amount of time (around 11 months on average) to table the Action Taken Report (ATR) in state legislatures, causing additional implementation delays. Due to these delays, the transfer of funds to local governments remains inconsistent and unpredictable, making financial planning difficult for ULBs.

Current municipal revenue streams face significant challenges, including discrepancies in the collection of taxes, limited access to capital markets and the inability to levy taxes and set rates. These issues make it difficult for ULBs to deliver even basic services under their 18 mandated functions, let alone address the growing need for climate adaptation (GIZ & ICLEI 2025). With most revenues consumed by operational expenses, only limited funds remain for infrastructure development or climate action (Thomas and Subramanian 2018). The Reserve Bank of India highlights that ULBs’ operational and maintenance expenses have increased from 8.8 per cent of the total expenditure in 2019 to 10 per cent in 2023, now constituting the second highest form of expense after salaries and wages (RBI 2024).

Thus, innovative financial solutions are critical to bridge this gap. Mechanisms such as municipal green bonds, pooled investment funds, and public-private partnerships (PPPs) offer promising avenues to mobilise additional resources. However, scaling such solutions requires systemic changes that improve the creditworthiness of ULBs, build their technical and fiscal capacities, and ensure collaboration between public and private entities to mitigate investment risks and accelerate climate adaptation efforts in India.

Recognising the challenges described above, this study aims to compile and assess best practices and case studies that showcase innovative and practical financial solutions. These solutions—either currently active or previously implemented by ULBs in India and globally— focus on financing climate adaptation and/or infrastructure projects, particularly those related to building climate-resilient infrastructure. This study seeks to provide actionable insights and scalable models to enhance financial planning, diversify funding sources, and promote sustainable urban development across ULBs in India.

The study aligns with the broader objectives of The Council’s ongoing initiative, supported by the Foreign, Commonwealth and Development Office (FCDO), British High Commission. The larger project aims to generate end-to-end solutions for Indian cities to enhance their infrastructural resilience against climate change. This includes conducting comprehensive data-driven and scalable climate risk assessments, identifying and prioritising targeted local-level adaptation measures, and developing financing models to enable access to public and private sector funding for climate adaptation.

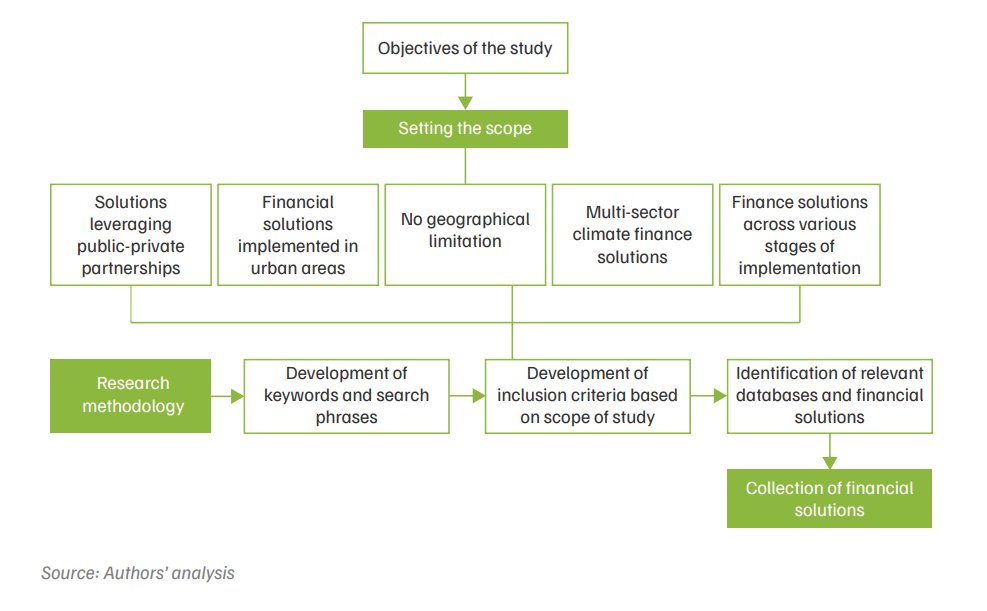

We identified appropriate financial solutions for this study through a structured process, as highlighted in Figure 2. This approach aimed to prioritise solutions that have the highest potential for replication in Indian cities or those that could be accessed by improving the financial and institutional capacities of ULBs, with support from central or state governments.

To arrive at these solutions, we reviewed a wide range of financial instruments across debt-based financing, financial risk management, and results-based financing categories that are currently in use, or have been applied in urban contexts globally. Each financial instrument was assessed for its relevance, scalability, and adaptability to Indian urban context, ensuring that the proposed solutions are both practical and replicable.

Figure 2: Overview of the methodology followed for the development of the collection of financial solutions

In line with the overarching objectives of the larger project, this study ensures a thorough exploration of financial mechanisms that support urban infrastructure resilience through publicprivate collaboration, focusing on climate adaptation and mitigation in diverse geographies and implementation contexts. The following points outline the scope of research in detail:

To ensure a comprehensive and targeted analysis of financial solutions for this study, we adopted a structured research methodology aligned with the scope of the study. The approach is outlined below:

The study identifies a broad range of financial instruments applied in urban areas across the globe to implement climate action. The findings are divided into three key sections:

Through the literature review, several financial solutions were identified. Most instruments such as loans, bonds, pooled investments, credits, etc. employ similar mechanisms and can be classified into three distinct categories. These categories reflect the scope of adaptation actions and the socio-economic condition of the implementation entities. Selecting the appropriate category helps stakeholders ensure not only the feasibility of implementation but also the long term sustainability and scalability of the adaptation actions. Table 1 highlights the three distinct categories of financial instruments.

Table 1. Categories of financial instruments

| Category | Description | Instruments |

|---|---|---|

| Debt-based instruments | Debt instruments are agreements between a lender and a borrower in which the lender receives fixed payment(s), usually with interest | Green bonds, resilience bonds, sustainability-linked loans |

| Financial risk management instruments | Financial risk management instruments transfer risks from one party to another, such as to an insurer, that can better underwrite or manage the risk | Credit guarantees, pooled investment funds, parametric insurance, debt-for-nature swaps |

| Results-based instruments | Results-based financing is a method of funding through which the lender/ funder provides capital contingent on the achievement of predefined and verifiable results These methods are intended to improve development outcomes and accountability and drive innovation and efficiency |

Green credits, biodiversity credits, payment for ecosystem services |

Source: NAP Global Network. 2024. Inventory of Innovative Financial Instruments for Climate Change Adaptation.

Over the past few years, several innovations have been made worldwide that combine instruments from different categories. Such new models of financial instruments have been categorised as ‘Other’ in Table 2, which provides a list of financial solutions implemented across the globe.

The selection of a financial instrument depends on several factors, including the socio-economic conditions of the implementing (public or private) entity undertaking the adaptation action and the specific characteristics of the climate action (Knight and Negreiros 2022). Certain financial instruments are better suited for specific types of adaptation actions, particularly those that align with the revenue-generating potential or scale of the project. For instance, large-scale adaptation actions with clear revenue streams may attract larger private investments or be supported through public-private partnerships. In contrast, smaller-scale or community-based actions with limited or no revenue potential may require concessional finance, grants, or subsidies (OECD 2023). Similarly, results-based financial instruments are more suitable for actions whose adaptation outcomes can be easily measured and verified.

Table 2 provides a list of financial solutions classified based on the financial instrument category and the adaptation action supported by the financial solution. Furthermore, the table highlights information about the stakeholders who either supported the implementation of the adaptation projects or provided financing for them. The table offers a comprehensive overview of the broader range of adaptation projects, stakeholders, and geographies that are actively engaged in scaling adaptation finance through innovative mechanisms at a global level.

Table 2: Financial solutions and instruments identified as part of the study

Table 2a. Debt-based instruments

| Instrument | Solution | Primary stakeholder | Adaptation solution(s) | Geography |

|---|---|---|---|---|

| Bonds | Eko Atlantic City Green Bond | Access Bank (Bond Issuer) | Building a seawall; installation of water infrastructure, such as surge barriers, pumping stations, levees, and gates. | Eko Atlantic City, Nigeria |

| Green bond for infrastructure financing in Cape Town | City of Cape Town, South Africa | Investments in water and sanitation projects, such as the upgradation of reservoirs and infrastructure | Cape Town, South Africa | |

| The Netherlands’ green bonds and blue projects | State of Netherlands | Reinforcing flood defence infrastructure, monitoring and management of water levels | Netherlands | |

| Indonesia’s Green Bond/Green Sukuk | Government of Indonesia | Habitat and biodiversity conservation; disaster risk reduction research leading to technology innovation | Indonesia | |

| Miami Forever Bond (climate resilience bond) | Government of Miami | Infrastructure investments such as flood mitigation pump stations, installation of backflow valves, drainage improvement, etc. | Miami, United States of America (USA) | |

| Ghaziabad Green Municipal Bond | Ghaziabad Municipal Corporation | Water reuse and tertiary sewage treatment plant | India | |

| Climate Resilience Bond | European Bank for Reconstruction and Development | Investment in climate-resilient infrastructure, such as wastewater treatment, water conveyance, irrigation, sustainable cooling infrastructure, climate-resilient agriculture, etc | Central Asia, Mediterranean, Central and Eastern Europe | |

| Sustainability Bond | Grameen Foundation | Resilience bond issued to build climate resilience of women in agrifood systems by enhancing their capacities and financing women-led agri-SMEs. | Uganda | |

| Climate Adaptation Bond | Asian Infrastructure Investment Bank | Investment in assets or activities enabling adaptation, such as urban flood-warning systems, or the installation of indoor cooling systems, upgrading urban drainage systems, undergrounding electricity transmission, etc. | Asia |

Table 2(b) Financial risk management instruments

| Instrument | Solution | Primary stakeholder | Adaptation solution(s) | Geography |

|---|---|---|---|---|

| Bonds | Eko Atlantic City Green Bond | Access Bank (Bond Issuer) | Building a seawall; installation of water infrastructure, such as surge barriers, pumping stations, levees, and gates. | Eko Atlantic City, Nigeria |

| Green bond for infrastructure financing in Cape Town | City of Cape Town, South Africa | Investments in water and sanitation projects, such as the upgradation of reservoirs and infrastructure | Cape Town, South Africa | |

| The Netherlands’ green bonds and blue projects | State of Netherlands | Reinforcing flood defence infrastructure, monitoring and management of water levels | Netherlands | |

| Indonesia’s Green Bond/Green Sukuk | Government of Indonesia | Habitat and biodiversity conservation; disaster risk reduction research leading to technology innovation | Indonesia | |

| Miami Forever Bond (climate resilience bond) | Government of Miami | Infrastructure investments such as flood mitigation pump stations, installation of backflow valves, drainage improvement, etc. | Miami, United States of America (USA) | |

| Ghaziabad Green Municipal Bond | Ghaziabad Municipal Corporation | Water reuse and tertiary sewage treatment plant | India | |

| Climate Resilience Bond | European Bank for Reconstruction and Development | Investment in climate-resilient infrastructure, such as wastewater treatment, water conveyance, irrigation, sustainable cooling infrastructure, climate-resilient agriculture, etc | Central Asia, Mediterranean, Central and Eastern Europe | |

| Sustainability Bond | Grameen Foundation | Resilience bond issued to build climate resilience of women in agrifood systems by enhancing their capacities and financing women-led agri-SMEs. | Uganda | |

| Climate Adaptation Bond | Asian Infrastructure Investment Bank | Investment in assets or activities enabling adaptation, such as urban flood-warning systems, or the installation of indoor cooling systems, upgrading urban drainage systems, undergrounding electricity transmission, etc. | Asia | |

| Pooled investment | Sustana Cooling India Fund | Climate, Sustana Impact Advisors | Space cooling-residential (including passive cooling materials); cooling devices - fans and air coolers | India |

| Sub-National Climate Finance Initiative (SCF) | IUCN, Pegasus Capital Advisors (Pegasus), BNP Paribas, Gold Standard, and R20 – Regions of Climate Action | Agri-food/bioenergy-related business projects with a nature impact lens | Asia and Pacific, Latin America and The Caribbean, Mediterranean, Sub-Saharan Africa | |

| Subnational Blended Finance Facility | Goa Government, SIDBI, NABARD, World Bank, PFC | Investment in projects with a focus on nature-based solutions | India | |

| Pooled investment funds, Credit guarantees | Climate Smart Health Infrastructure Fund | Samridh Blended Finance Facility, IPE Global | Investment to scale climate solutions like sustainable cooling infrastructure | India |

| Insurance | Philippine City Disaster Insurance Pool | Asian Development Bank | Improving the financial preparedness of the governments at the time of climate-induced disasters, focusing on rapid post-disaster financing. | Philippines |

| CILRIF (Climate Insurance Linked Resilient Infrastructure Financing) | United Nations Capital Development Fund | Adaptation measures that address heat and flood-related risk while building the resilience of infrastructure owned by municipal governments | Piloted in Durban (South Africa) and Makati (the Philippines) | |

| Municipal Pooled Insurance | Urban Infrastructure Insurance Facility | Latin American and Caribbean governments | Risk assessment of critical assets in urban areas to inform insurance coverage products against the impact of extreme weather events | Curitiba, Porto Alegre and Recife in Brazil; Reynosa and Mérida in Mexico; Tegucigalpa, Honduras, and Kingston, Jamaica |

| Guarantees | Green Guarantee Company (GGC) | Development Guarantee Group | Undertaking nature-based solutions projects | South Africa |

Table 2(c) Results based financing instruments

| Instrument | Solution | Primary stakeholder | Adaptation solution(s) | Geography |

|---|---|---|---|---|

| Insurance and Blue/ Green Credits | Restoration insurance service company | Conservation International | Investments in mangrove conservation and restoration in areas with high-value assets | Philippines |

Table 2(d) Debt and equity-based financial instruments

| Instrument | Solution | Primary stakeholder | Adaptation solution(s) | Geography |

|---|---|---|---|---|

| Private equity fund | Catalyst Climate Resilience Fund | Catalyst Impact Partners, BFA Global Group | Investment in technology solutions to manage risks, adapt livelihoods and build long-term resilience to climate change | Africa |

| ACT Fund | ARM-Harith Infrastructure Investments Limited | Investment in water infrastructure projects | West Africa |

Table 2(e) Other - Miscellaneous category*

| Instrument | Solution | Primary stakeholder | Adaptation solution(s) | Geography |

|---|---|---|---|---|

| Levy/Tax | Infrastructure levy for urban renewal measures in Germany | Local governments | Examples where a landowner pays a levy include: green and open spaces for climate protection and adaptation, construction or expansion of renewable energy systems | Germany |

| Platform | Matchmaker service | Carbon Disclosure Project | Investment in initiatives like stormwater management, urban tree canopy | India |

Source: Authors’ compilation based on literature review

*Note: Financial instruments falling in ‘Other – Miscellaneous’ category refer to those that do not fall in the traditional categories of financial instruments, as highlighted in Table 1. These instruments either do not generate finance (from the private sector) or have not yet been ideated for the purpose of implementation.

While each identified financial instrument and solution caters to a specific adaptation measure or the socio-economic profile of the user, a few are particularly important to understand, since they have the potential to be replicated and utilised to build the resilience of urban infrastructure in India. The following solutions are explained in detail, including not only the working model of the solution but also the challenges faced by the instruments, which will need to be addressed before replicating them in the context of any city in India.

Vadodara green municipal bond

The Vadodara Municipal Corporation (VMC) in 2019 initiated the process of issuing municipal bonds to finance its critical water supply and liquid waste treatment projects in the city. The municipal corporation identified the utility of the Sindhrot Water Supply Project in addressing the drinking water needs of the southern zone of the city, which could be further supported by the installation of an auxiliary pumping station at Amit Nagar to avoid untreated sewage water reaching the Vishwamitri River (OECD 2023).

In 2022, VMC issued its first municipal bond on a private placement basis, raising INR 100 crore (USD 12 million). This was used to meet VMC’s 30 per cent contribution mandate for Atal Mission for Rejuvenation and Urban Transformation (AMRUT) projects (Vadodara Municipal Corporation and US Treasury 2022).

In 2024, VMC issued a municipal green bond for a tenure3 of five years at a coupon rate of 7.9 per cent, again raising INR 100 crore (USD 12 million) to fund liquid wastewater management projects. The bond is distinguished as India’s, and Asia’s, first certified green municipal bond for sustainable water infrastructure (Climate Bonds Initiative 2024). The bond proceeds will fund the establishment of two sewage treatment plants in Sherkhi and Undera, along with an auxiliary pumping station. The total project cost, including capital, operations, and management expenditure, is estimated to be INR 360.26 crore (USD 41.55 million) (Vadodara Municipal Corporation 2024). The main aim of implementing these projects is to reduce the surcharge flow and facilitate the usage of treated sewage water by industries, to reduce the stress on freshwater resources (Climate Bonds Initiative 2024).

Instrument mechanics

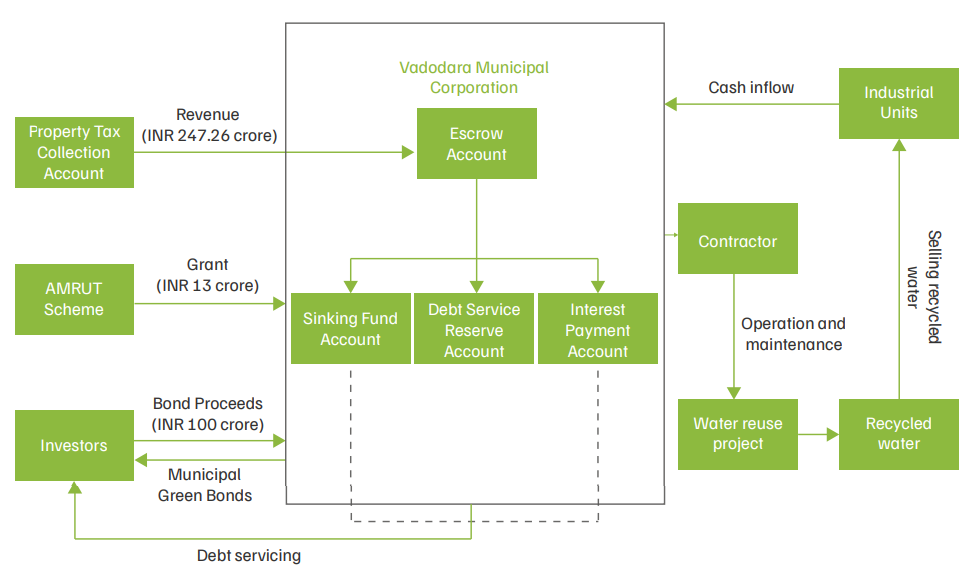

Under the AMRUT 2.0 scheme, ULBs that have previously received financial incentives for issuing municipal bonds become eligible for a second incentive upon issuing municipal green bonds. VMC issued municipal bonds in 2022 to finance two projects under AMRUT, receiving a financial incentive of INR 13 crore (USD 1.5 million) as a grant upon issuing an INR 100 crore (USD 12 million) bond. Subsequently, VMC issued a green bond in 2024, securing an additional grant of INR 13 crore (USD 1.5 million) under the AMRUT scheme (Vadodara Municipal Corporation 2024). The financial support from the central government, along with the INR 100 crore (USD 12 million) raised from issuing the green bond, supplemented by VMC’s existing revenue stream, enabled the city to construct and upgrade liquid wastewater management infrastructure.

VMC has implemented a structured payment mechanism4 by establishing a separate escrow account for the purpose of debt servicing. As per the mechanism, property tax revenue is periodically transferred from the property tax collection account maintained by the municipal corporation to the escrow account. From there, funds are further transferred to an interest payment account from which the interest is paid to the bondholders. A sinking fund account5 and a debt service reserve account (DSRA) are also maintained to ensure timely repayment of the principal amount and provide risk coverage in case of default.

Figure 3: Financing structure of the Vadodara green municipal bond

Source: Authors’ analysis

Gujarat’s 2018 wastewater reuse policy mandates that only treated water may be used by industrial units in the Special Investment Region (SIR), industrial parks, and large industrial units consuming a minimum of one lakh litre of freshwater per day for non-potable purposes and located within a 50 km radius of a sewage treatment plant (STP) (Government of Gujarat 2018). Therefore, in addition to reducing the strain on freshwater resources through wastewater reuse, the STP project offers VMC an economic incentive by selling treated water to industries. The proceeds from the green bond will be channelled through an escrow account to finance capital expenditures incurred during the construction and management of STPs. Once operational, the project is expected to generate cash inflow from the sale of treated and recycled wastewater. Currently, VMC is in the process of identifying an implementing agency to operate and maintain the treated wastewater facility.

The Vadodara Municipal Corporation appointed CRISIL and India Rating & Research Private Limited, both SEBI-registered credit rating agencies, to conduct the credit rating process (Vadodara Municipal Corporation 2024). Based on various fiscal indicators such as revenue income, revenue expenditure, property tax collection, debt repayment trends, and others, and after the review of financial statements, VMC received credit ratings of AA+ from CRISIL and AA from India Rating & Research Private Limited (Vadodara Municipal Corporation 2024). The ratings indicate a high degree of safety and strong creditworthiness in servicing financial obligations. VMC appointed SBICAP Trustee Company Limited as the debenture trustee6 for the bond to oversee compliance with regulatory requirements and to ensure payments to bondholders are made on time (Vadodara Municipal Corporation 2024).

The Gujarat Provincial Municipal Corporation Act of 1949 empowers municipal corporations of the state to raise funds through debt instruments. In addition, legislative provisions encourage cities in the state to seek financing for urban infrastructure from government institutions, such as the Housing and Urban Development Corporation (HUDCO) and National Housing Bank (NHB), among others (Vadodara Municipal Corporation and US Treasury 2022). Together, these measures create an enabling ecosystem for the cities in Gujarat to improve their access to debtbased financing.

Challenges faced by these types of instruments

Although green bonds have a growing potential as an innovative financing mechanism for municipal corporations, their expansion is hindered by several structural and institutional challenges. One major challenge is the lack of in-house capacity and trained professionals to manage the technical and regulatory aspects of green bond issuances (GIZ 2017). This concern is even more acute in the cases of smaller ULBs, which often lack the resources and technical capacities to engage with the complexities of the capital market. As per the eligibility criteria set by SEBI, a positive net worth equivalent to three financial years must be maintained before the issuance year of the bond. This requirement can be particularly challenging for small and medium-sized municipal corporations facing poor budgetary conditions with low revenue-generating capacity (GIZ 2017).

In addition, the participation of municipal corporations in the bond market remains limited due to their lack of financial autonomy, outdated accounting standards, and insufficient transparency in reporting credible financial data (Bibhudatta and Rathee 2025). Investors require reliable and consistent financial data in order to make informed credit and investment decisions (Athar, White, and Goyal 2022). However, many Indian ULBs continue to follow traditional cash-based accounting instead of accrual-based system which fail to accurately reflect the financial health of these urban local bodies (Bibhudatta and Rathee 2025) . This undermines investors’ confidence and further limits access to private finance. Compounding these challenges is the limited fiscal autonomy of ULBs. Most ULBs require approval from state government, before undertaking capital expenditure, restricting their ability to respond to local infrastructure needs in a timely manner (Athar, White, and Goyal 2022). Without an enabling institutional environment that supports decentralised decision-making, it is challenging for ULBs to build their fiduciary capacities and improve their public financial management.

Despite these challenges being widespread, some ULBs have successfully navigated these obstacles. Prior to 1993-94, the Ahmedabad Municipal Corporation (AMC) faced significant fiscal constraints, with no new sources of income and a heavy dependence on government grants. However, beginning in 1994, AMC took a series of measures to strengthen its financial position which included restructuring and strengthening of property tax department, issuing notices and warrants to defaulters, and recruiting professionals to improve its workforce capabilities. These targeted measures progressively improved AMC’s fiscal and technical capacity, enabling the corporation to manage several capital-intensive infrastructure projects over time (Vaidya and Johnson 2001). The effectiveness of these reforms became evident in 2019, when AMC’s municipal bond issuance for the implementation of green projects attracted strong market demand (Verma 2020). The bond received a credit rating of AA+ from both CRISIL and India Ratings, reflecting the ULB’s strengthened financial risk profile and enhanced operating efficiency. The case of AMC highlights that the introduction of local reforms can help ULBs overcome their challenges and improve their access to funds so as to finance their infrastructure needs.

Scope of replication

Vadodara Municipal Corporation has a long history of securing finance for urban infrastructure projects through loans from commercial banks, development institutions, bilateral agencies, etc. Over time, VMC has ensured the timely payment of debt financing, which became one of the key factors in increasing investors’ confidence in the corporation’s institutional capabilities and fiscal strength (Vadodara Municipal Corporation and US Treasury 2022). Thus, ULBs with a proven track record in debt management and repayment, and an enabling ecosystem at the state level that supports debt finance for infrastructure investments, are well positioned to replicate such financial instruments successfully.

Pooled financing emerged as a viable strategy towards improving ULBs’ accessibility to domestic capital markets for the debt financing they need to invest in their urban infrastructure projects, particularly for small and medium-sized ULBs. This approach allows multiple ULBs to collectively access debt financing to fund infrastructure projects, by issuing municipal bonds under a single umbrella. For example, in 2002, the Tamil Nadu state government created the Water and Sanitation Pooled Fund (WSPF) to help small ULBs finance their water and sanitation services by raising domestic capital on a pooled basis (World Bank 2016). Thirteen small and medium ULBs that lacked credit ratings were selected to receive sub-loans from the bond proceeds issued by the WSPF. This initiative enabled these ULBs to meet the funding requirements to finance their infrastructure projects, as they could not issue municipal bonds independently.

The Pooled Finance Development Fund (PFDF) Scheme, initiated by the Government of India, aims to enhance the financial capacity of Indian ULBs — particularly smaller ones — by enabling their access to capital investments for funding infrastructure projects, while reducing their borrowing costs through state level pooled financing facility (Ministry of Urban Development 2008). The existence of WSPF indicates that innovative, blended finance models for urban development are already in place. With support from both public and private stakeholders, similar financial models could be designed to address the urban infrastructure needs of small and medium-sized ULBs, with an emphasis on enhancing their climate resilience.

To address the water crisis in Ghaziabad, which was characterised by both a shortage of potable water and poor water quality, particularly during the summer months, Ghaziabad Nagar Nigam (GNN) issued India’s first green municipal bond (not certified by a third party) in April 2021. This debt instrument, issued by GNN, aimed to address urban infrastructure needs by encouraging investments from the private sector. The bond raised INR 150 crore (USD 17.61 million) through the Bombay Stock Exchange (BSE) to partially finance the development of a tertiary sewage treatment plant, a revenue-generating water reuse project with a net output capacity of 40 million litres per day (Tetra Tech 2024). The bond had a tenure of 10 years, with principal repayments scheduled annually starting four years from the deemed date of allotment.

Through bond proceeds and its property tax revenue stream, GNN has provided financial backing for the water reuse project, with a total cost of INR 239.93 crore (USD 28.17 million). Under the Atal Mission for Rejuvenation and Urban Transformation (AMRUT) scheme, a municipal corporation is eligible to receive a financial incentive of INR 13 crore (USD 1.527 million) for every INR 100 crore (USD 11.74 million) of green bonds issued. Therefore, for issuing a green bond of INR 150 crore (USD 17.61 million), GNN secured a financial incentive of INR 19.5 crore (USD 2.29 million) from the central government (Brickworks Ratings 2024).

GNN has established a structured payment mechanism and identified a suitable revenue stream to fund an escrow account, where money will be collected from house, water, and sewer taxes (collectively referred to as property tax). In this mechanism, the Urban Development Department of Uttar Pradesh state government would provide additional liquidity support through its infrastructure development fund to replenish any shortfalls in the DSRA and sinking fund account.

Though this is a revenue-generating project, cash inflows generated from selling recycled water to the nearby industrial units are not earmarked for the servicing of GNN’s financial obligations to bondholders. For the green bond, SBICAP Trustee Company Limited acts as a debenture trustee, ensuring that all accounts align with regulatory requirements and payments are met in a timely manner (Ghaziabad Nagar Nigam 2021).

The preparatory process for issuing this bond took nearly two years, and involved project identification, improvements in GNN’s financial management systems, the development of a structured payment mechanism, credit rating by a recognised agency, and due diligence by an appointed merchant banker. This groundwork improved GNN’s credit rating from ‘A-’ to ‘AA (CE)’ as rated by Brickwork Ratings, a SEBI-registered credit rating agency, indicating that the instrument has a high degree of safety in the timely servicing of financial obligations (Ghaziabad Nagar Nigam 2021).

A bond is a debt-based instrument, commonly used in blended finance, that is issued by governments, public utilities, banks or companies to raise capital for growth and development (Habbel et al. 2021).

Broadly, thematic bonds are classified into two types:

Transition bonds: Transition bonds can either be UoP or sustainability-linked bonds (Jain 2022). They are characterised by proceeds being specifically used to finance the green transition of industries emitting higher levels of greenhouse gases (GHGs).

By understanding the differences among these thematic bonds and their categories, stakeholders — particularly investors — can make informed choices based on which debt instruments align with their impact objectives, financial goals, and risk tolerance. For the purpose of this study, we have focused on four specific types: green bonds, climate resilience bonds, blue bonds, and municipal green bonds.

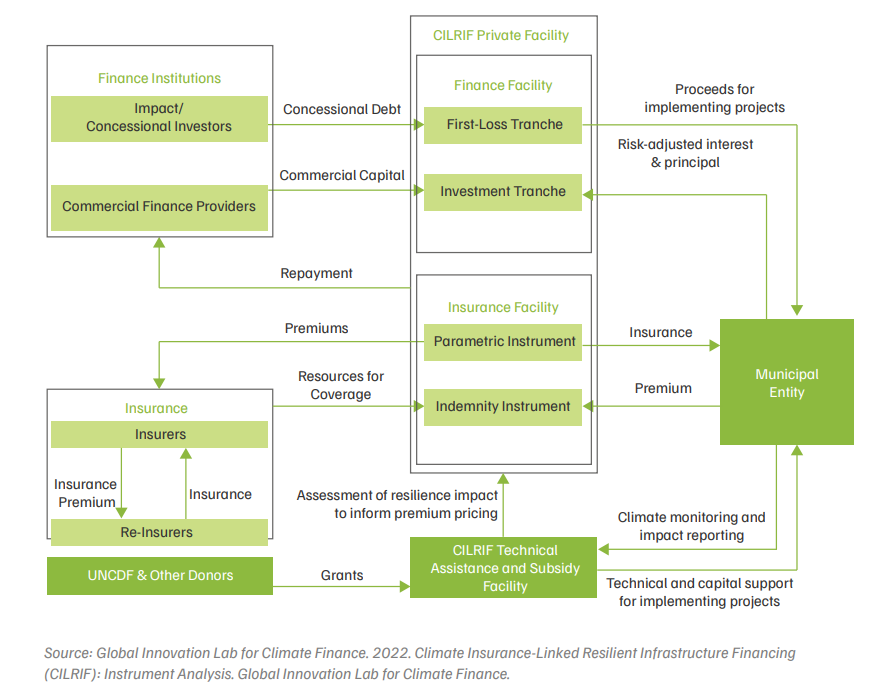

Climate insurance-linked resilient infrastructure financing (CILRIF)

Instrument mechanics

CILRIF is divided into two structures. The primary structure, called the CILRIF Private Facility, consists of the insurance and financial facilities and is responsible for pricing both sides of the transaction: buying and selling climate risk. This primary structure is supplemented by the CILRIF Technical Assistance and Subsidy Facility, which provides technical support to cities through grants.

The insurance facility provides municipal governments with long-term climate insurance products for 10 years and longer, at fixed premiums and coverage terms. This insurance covers municipally owned assets exposed to climate risks like heat or flood, and requires cities to invest in climate adaptation projects. Successful completion of these projects leads to reduced premiums, reflecting the lowered risk. The insurance facility combines parametric and indemnity structures, wherein the former ensures immediate pay-outs based on predefined climate thresholds (for instance, temperature or flood levels identified through climate risk assessment), while indemnity coverage adjusts premiums based on the demonstrated impact of resilience measures.

Figure 4: CILRIF instrument mechanics

The financing facility will develop a global fund to finance projects that focus on resilient municipal infrastructure directly. This will be done as part of the insurance contract, or as a municipal bond purchase. The global fund, with a target of USD 1 billion — USD 800 million as commercial investment and USD 200 million as concessional investment — will act as a pooled investment that will generate investor confidence and provide municipalities with finance that would not have been accessible otherwise (Global Innovation Lab for Climate Finance 2022).

The CILRIF Technical Assistance and Subsidy Facility builds the municipalities’ institutional and financial capacity and provides grants and technical support to help them secure funding for climate adaptation measures. Initially, this facility is supporting the broader CILRIF structure with subsidies and grants until a sufficiently diversified pool of cities can stabilise the operation. Together, these mechanisms streamline risk management, facilitate access to affordable financing, and support urban resilience efforts.

Challenges faced by these types of instruments

CILRIF is a hybrid model that depends on debt-based instruments, financial risk management and results-based financing. Several barriers need to be addressed to ensure smooth operation of the fund over a long period. Climate adaptation is highly context-specific, and the lack of established indicators makes it difficult to measure the impact of adaptation measures implemented by municipalities. This limits the ability to develop a standardised method to reduce premiums based on the cities’ performance. Moreover, insurance providers face many barriers, such as high risk uncertainty due to limited climate data and modelling limitations, and a lack of reinsurance support to distribute extreme loss exposure to offering affordable products. This poses barriers to scalability and adoption of the model, particularly in lower-tier cities where financial resources are more constrained.

Additionally, pay-out triggers represent one of the most significant challenges in operationalising CILRIF, as it directly influences the reliability, timeliness, and credibility of disbursements. Predominantly parametric in nature, these triggers, based on predefined climate indicators like wind speed or rainfall thresholds, offer speed and transparency but carry substantial basis risk, often resulting in pay-outs that do not reflect actual damages or, conversely, in non-payouts despite significant loss. This misalignment undermines stakeholder confidence, particularly in developing economies where data infrastructure is limited and public trust in financial instruments is fragile.

Scope of replication

A model such as this relies heavily on a large project pipeline, and the support of private investors and Development Finance Institutions (DFIs) to provide commercial and concessional capital. A similar model for India will require national-level effort by the government, philanthropic organisations, and technical institutions to identify adaptation measures for cities based on periodic risk assessment, estimate threshold levels, generate private finance, and build the capacities of municipal corporations to implement adaptation measures. Additionally, a regulatory framework will also be required to legally enable municipal governments to procure long-term climate insurance products and enter into insurance-linked financial agreements (Bardhan and Balasubramani 2024). This would involve amendments or clarifications to state municipal laws to allow for the procurement of parametric and indemnity insurance, and provisions in public finance rules to enable long-term premium payments across budget cycles. Coordination with the IRDAI (Insurance Regulatory and Development Authority of India) will also be necessary, to define standardised parametric thresholds, product structures, and conditions for claim eligibility and settlements in the public sector. Given the lack of technical and financial expertise in managing such instruments, a national-level platform for urban climate risk insurance support platform should be established, providing cities with technical advisory, grant-based co-financing, and risk modelling services (Sood et al. 2025). This facility would help ULBs design climate-resilient infrastructure projects, estimate the potential for risk reduction, and monitor adaptation outcomes. Such efforts could encourage the muchneeded scaling of adaptation finance in India and directly contribute to the country’s efforts to build the resilience of its infrastructure.

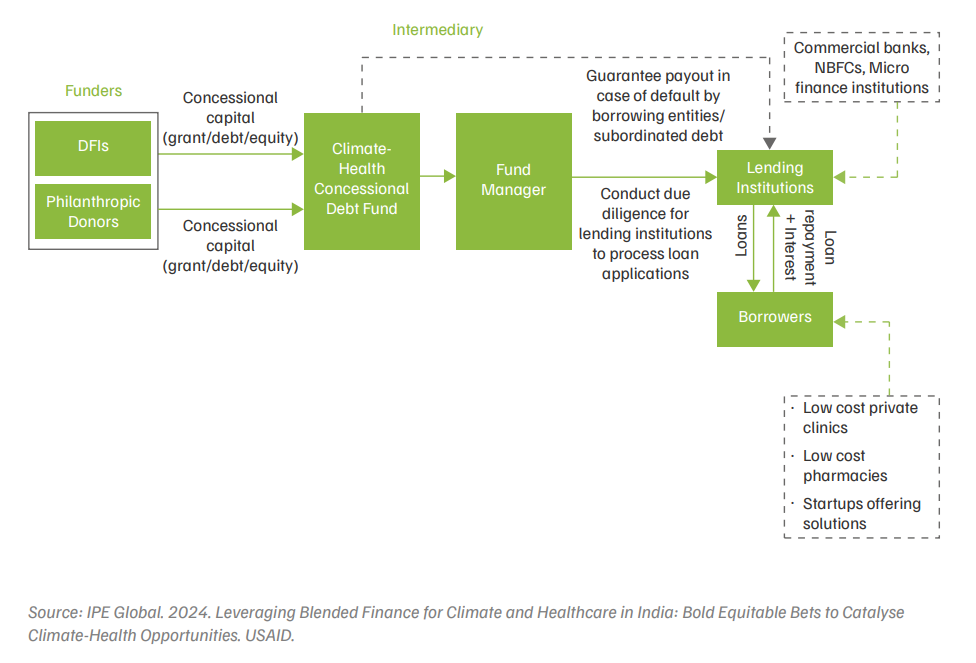

Climate smart health infrastructure fund (CSHIF)

According to XDI’s Global Hospital Infrastructure Physical Climate Risk Report, 2,700 of India’s 53,473 hospitals, are already classified as high risk for partial or complete shutdown due to extreme weather events (XDI 2023). Residents in poor metropolitan regions are especially vulnerable, facing limited access to healthcare facilities as a result of poor building conditions, unstable power supply, and inadequate sanitation and hygiene.

Given these challenges, financing adaptation measures to withstand the impacts of climate change is critical. India raised USD 22.5 billion for climate action in 2022, but only 4 per cent of this — about USD 1 billion — was allocated to projects at the intersection of climate change and health (Thakur et al. 2024). This highlights the insufficient mobilisation of financial resources for India’s climate-resilient health sector. Nonetheless, an analysis by Quadria Capital indicates there is a market opportunity of USD 3 billion annually for the private sector to engage in adaptation-focused strategies within the space of climate and health. The expansion of the blended finance ecosystem offers a promising pathway, with investments in India growing from USD 0.1 billion in 2010 to USD 1.1 billion in 2022, in which 8 per cent of funded activities were directed towards health initiatives in India (Thakur et al. 2024).

Recognising these gaps and potential, in 2024, the Samridh Healthcare Blended Finance Facility, with assistance from IPE Global, launched the Climate Smart Health Infrastructure Fund. This fund is designed to catalyse commercial capital from formal financial institutions, to scale climatesmart health infrastructure solutions across India (IPE Global 2024).

Instrument mechanics

This financial model, currently in the ideation phase, is designed to encourage the flow of commercial capital, from formal financial institutions such as NBFCs, commercial banks, and microfinance institutions, to entities providing climate infrastructure solutions. The objective is to scale up these solutions, strengthen healthcare infrastructure, and prepare India’s health systems for the impacts of extreme climate events.

The CSHIF utilises a blended finance structure to channel concessional capital from development funders, including DFIs and philanthropic organisations, so as to encourage the flow of commercial capital from formal financial institutions via low-cost loans that support the scaling of climate health infrastructure solutions. This concessional capital, in the form of grants, debt, or equity, flows into a concessional debt fund, conceptualised either as a credit guarantee or subordinated debt.

In both cases, the blended finance approach aims to reduce the perceived risk attached to commercial capital providers, making investments in climate-resilient health infrastructure more viable and scalable.

Figure 5. CSHIF instrument mechanics

This model includes a fund manager, who is responsible for conducting due diligence and screening loan applications before referring prospective borrowing entities to the lending institutions. Some borrowing entities that could benefit from this model to scale climate solutions in their health infrastructure include:

Challenges faced by these types of instruments

The design of the instrument faces several challenges that could impact its effectiveness. Integrating borrowing entities providing climate solutions as part of the value chain, requires that these entities remain aligned with the impact mandate of the instrument. Ensuring this alignment with the impact objective necessitates continuous monitoring, which can be complicated and resource-intensive.

Furthermore, climate resilience projects usually have longer development and payback cycles, which makes the duration of guarantees critical in determining the success of the projects. Therefore, conducting research to determine the optimal guarantee period is necessary to enable the success of the financial model, and to ensure that the duration of the guarantee matches the risk profile of each project.

Scope of replication

Countries in the building phase, with less-developed health systems and limited engagement from the private sector, may prefer to deploy simpler blended finance models such as technical assistance grants and guarantees to mobilise financial resources towards creating resilient climate health infrastructure. Countries in the transition phase, with more established health systems, can explore more complex models like impact bonds and funds to garner more attention from private investors (IPE Global 2022). India lies somewhere in the middle of these phases, with relatively better health infrastructure, but faces challenges of access and has financial markets that are still developing. While complex blended finance tools may not yet be viable, India’s primary healthcare sector presents significant market potential (IPE Global 2022).

Going forward, there is a pressing need to build a pipeline of commercially viable or market-based climate health solutions that can be scaled and purchased by the government or other actors. The blended finance models ideated by Samridh Healthcare and its partners can be instrumental in scaling market-driven climate health solutions. By creating viable business models, these approaches have the potential to ensure last-mile connectivity, bracing vulnerable populations for the impacts of climate change and ultimately improving access to, and better, healthcare infrastructure across the country.

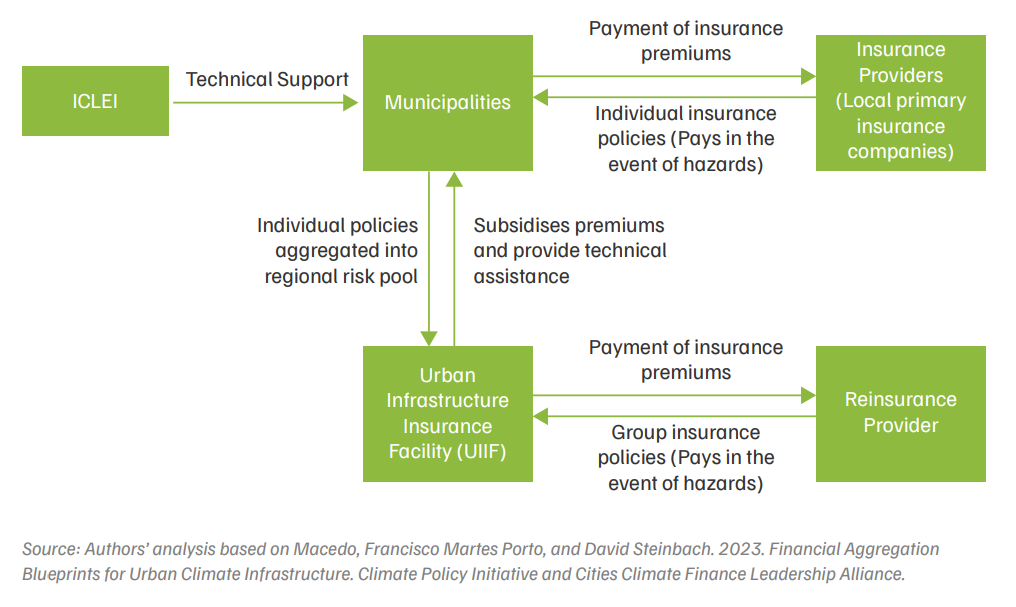

Urban infrastructure insurance facility (UIIF)

Uninsured losses, resulting from the increase in the intensity and frequency of extreme weather events, continue to strain the sub-national and national budgets of developing countries, limiting their ability to address other critical urban needs (UNDRR 2022). About 70 per cent of cities in Latin America and the Caribbean are affected by heatwaves, droughts, floods, and tropical storms. These cities often rely on central or state governments to pay for disaster response and recovery during extreme climate events (ICLEI n.d.). However, the lack of risk-transfer mechanisms, like parametric insurance for climate hazards, significantly delays the efforts of municipal corporations to manage climate shocks effectively.

To address this gap, ten cities in Mexico, Brazil, Jamaica, and Honduras have established a municipal pooled insurance mechanism which insures critical urban infrastructure and vulnerable populations from the impacts of extreme climate events (Macedo and Steinbach 2023).

Instrument mechanics

Implemented by the International Council for Local Environmental Initiatives (ICLEI), the Urban Infrastructure Insurance Facility (UIIF) is designed to help cities access insurance coverage for specific climate hazards through municipal pooled insurance mechanisms. In this model, several city governments collaborate to purchase insurance coverage at more favourable rates by pooling their risks and buying collectively rather than individually (Pinko et al. 2022). By doing this, cities benefit from lower premiums while maintaining the same expected loss levels for specific assets. This aggregation reduces the total capital required to insure these assets. (IDF 2019).

Ten cities have been selected for the UIIF based on their diverse physical and urban environments and their exposure to climate hazards. The cities will decide which climate hazards they want to be insured against. ICLEI will provide technical support to help city governments better understand their risk profile, and protect their critical infrastructure and vulnerable populations. Once this assessment is complete, cities will purchase individual insurance policies from local insurance providers by paying annual premiums. To further support the initiative, the UIIF will subsidise premium payments for the first three years, easing the financial burden on cities and making insurance more affordable during the initial stages.

Figure 6: UIIF instrument mechanics

With the support of a specialised agency, the UIIF will aggregate the individual policies purchased by the ten participating cities into a regional pool. This pooled structure will enable the purchase of group reinsurance, and allow the UIIF to pay premiums to an international reinsurer. Additionally, UIIF will provide technical support to build the cities’ disaster risk-reduction capacities through policy design and strategy development. In the event of climate hazards, primary insurance providers will make direct pay-outs to the affected cities. If the pay-outs cross a specified threshold, the reinsurer will reimburse the UIIF, offering further support to both municipalities and primary insurers.

During climate shocks that require high pay-outs, transferring risk to the reinsurer allows primary insurance providers to offer better rates to municipalities. The UIIF is currently in the design phase and will be operational in 2025. The facility is financed by Kreditanstalt für Wiederaufbau (KfW) (Credit Institute for Reconstruction) on behalf of Bundesministerium für wirtschaftliche Zusammenarbeit und Entwicklung (BMZ) (German Federal Ministry for Economic Cooperation and Development) (Macedo and Steinbach 2023).

Challenges faced by these types of instruments

Municipal insurance pooling is still an emerging concept within the disaster risk management community. Although ICLEI has conceptualised this idea and channelled significant resources into fine-tuning the instrument’s purpose, the lack of existing examples in both developing and developed countries means that there are fewer opportunities for similar instruments in the design phase to learn from, so they can attract the right mix of municipalities and insurance providers. Moreover, although the UIIF has brought together diverse cities committed to enhancing climate resilience, aligning them around shared objectives and helping them to understand region-specific climate change-induced vulnerabilities demands both time and resources.

Scope of replication

Given the absence of operational municipal insurance pools in developing countries, it is challenging to foresee all the potential mechanisms to replicate a similar risk pool. However, it may still be possible to identify enabling factors for the implementation of such pooled solutions:

By establishing dedicated budgets for insurance payments and financial delivery mechanisms, ULBs can take swift action, enabling them to promote business continuity and accelerate reconstruction efforts following extreme climate events.

The current financial capacity of ULBs in India is insufficient to implement solutions for the enhancement of urban infrastructure resilience (Jena 2021). To bridge this gap, it is essential to identify innovative financing pathways that cater to the socio-economic conditions of a diverse set of ULBs, and different adaptation solutions that may or may not be resource and capitalintensive (Knight and Negreiros 2022). Private finance has significant potential to address the financial gap. It could furthermore provide benefits such as compliance with Corporate Social Responsibility (CSR) requirements and resilience in industrial supply chains through building infrastructure resilience (OECD 2024).

However, scaling private finance for climate adaptation presents significant challenges, stemming from various factors including the lack of localised climate data, insufficient evidence of successful financing mechanisms, investor bias, low returns on investment, and a smaller market size and project pipeline (Singh, Ahuja, and Malhotra 2021). Additionally, uncertainty due to evolving climate risks further complicates the process of measuring and monitoring the effectiveness of adaptation actions. Addressing these challenges will require innovative financial solutions that have the potential to be scaled across multiple cities. Moreover, such financial solutions will need to be supplemented with comprehensive climate risk assessments that incorporate future risks, enhanced collaboration between public and private entities, and the successful execution of pilot projects over extended periods, to establish an evidence base and build investor confidence.

An analysis of the case studies identified for the study highlights that the majority of financial instruments utilised to generate adaptation finance fall under the categories of debt-based or financial risk management instruments. Concessional debt instruments, such as loans or pooled investment funds that blend commercial and concessional capital, along with insurance mechanisms, are particularly prominent. These instruments provide the necessary funding for adaptation projects and build investor confidence by mitigating risks through guarantees in cases of default (OECD 2023). The effectiveness of these instruments lies in their ability to distribute risk among multiple stakeholders, thereby reducing the likelihood of significant financial losses for any single entity. Globally, there is a noticeable trend toward prioritising financial risk management instruments over debt-based mechanisms. This is because debt-based instruments lead to an increase in the debt burden of stakeholders, especially those located in the Least Developed Countries (LDCs), since they already face significant debt burdens due to poverty and development-related challenges (IIED 2024). In India, where most municipalities lack adequate financial resources to independently take on debt, financial risk management instruments that share the repayment burden across multiple entities should be prioritised to ensure sustainable financing for adaptation initiatives.

Results-based financial instruments, while holding significant potential, encounter the most challenges in the context of climate adaptation. These difficulties extend beyond funding limitations, and arise from the technical complexities associated with adaptation actions. Some of these challenges include identifying and measuring adaptation benefits, ambiguity in distinguishing development activities from adaptation measures and a lack of project pipelines in urban areas to utilise funds effectively (Escalante and Orrego 2021). Additionally, instruments such as credits (green credits, biodiversity credits, etc.) often struggle to generate sufficient revenue from the implementation of adaptation actions (Micale, Tonkonogy, and Mazza 2018). Despite these challenges, results-based instruments offer several benefits, including increased transparency and guarantees that the adaptation benefits will reach the local level (World Bank 2021). Innovative approaches are required to ensure these instruments generate adequate financing for their scaling across multiple cities. Additionally, to successfully implement resultsbased financial instruments, it is necessary to build the financial and technical capacity of the public entities responsible for implementing adaptation actions, to ensure proper financial management and reporting of generated benefits. This is especially important for India, where the government launched the Green Credit Rules to scale adaptation finance (MoEFCC 2023b). This financial solution is an innovative market-based mechanism designed to incentivise voluntary environmental actions across diverse sectors by various stakeholders, such as individuals, communities, private sector industries, and companies.

The case studies discussed illustrate financial solutions that have a high potential for replication in India, focusing on innovative approaches to support climate adaptation actions. Among these, the Vadodara Green Municipal Bond and the CSHIF are ones that have either already been implemented or have been ideated to be implemented in India. While the Vadodara Green Municipal Bond has been successfully implemented, raising almost INR 240 crore, the CSHIF is still in its ideation phase, but it shows promise in the generation of finance to enhance the resilience of healthcare infrastructure. Both solutions leverage support from public entities, such as the Government of India and the Government of Uttar Pradesh, and international institutions like DFIs, to build investor confidence and secure concessional debt from private entities.

Adaptation actions with clear revenue streams, such as the development of green parks to mitigate heat and flood risks, can adopt models like the Vadodara Green Municipal Bond. Similarly, sectors where private entities provide essential services, such as road infrastructure or healthcare clinics, could benefit from a framework similar to the CSHIF. However, for successful replication, certain prerequisites must be met. The Vadodara Green Municipal Bond was feasible primarily due to the high credit rating of the municipal corporation, which boosted investor confidence. In the case of the CSHIF, only private healthcare units that could provide substantial evidence of debt repayment could be considered eligible for concessional loans. This underscores the importance of enabling or supporting borrowers to develop financially and technically sound proposals that highlight the potential of adaptation projects in generating revenue streams, good credit ratings and consideration of future climate risks, which will qualify their projects for funding through innovative financing mechanisms.

Expanding ULBs’ access to financial solutions such as the CILRIF and the UIIF will require systemic improvements. ULBs need enhanced technical capacity and adequate human resources to manage such solutions effectively. Additionally, extensive capacity-building trainings and decentralised monitoring systems are critical for ensuring that ULBs perform fundamental tasks, such as the timely publication of audited annual financial statements, which is a basic requirement for improving credit ratings and accessing capital markets.

For greater access to commercial debt, ULBs must focus on showcasing their financial health. This includes demonstrating revenue diversification, reduced dependency through revenue generation or adequate support to pay interests, and established liquidity reserves (Jena 2021). The government and regulatory bodies also play an important role in facilitating these processes. They must establish a supportive policy environment and conduct comprehensive capacitybuilding programs to ease the procedural and reporting burden on ULBs. To address some of these challenges, ULBs can leverage technical and advisory support from Climate Centre for Cities (C-Cube), established under the National Institute of Urban Affairs (NIUA). C-Cube assists in the preparation of city-based climate action plans, offering ULBs support in navigating climaterelated planning (Sood et al. 2025). Tools such as the Climate Data Observatory, set up under C-Cube can provide ULB officials and other relevant stakeholders with insights from climaterelevant data to plan more need-based and targeted climate actions. Furthermore, preparing municipal accounting statements in accordance with the National Municipal Accounts Manual (NMAM) can ensure the timely and accurate recording of financial transactions. Having a standardised accounting framework will not only help ULBs build their credibility among investors and funding agencies, but will also help them overcome existing constraints and mobilise investment in necessary infrastructure (RBI 2024). This will ensure stringent eligibility and reporting requirements do not deter ULBs from accessing financial instruments such as bonds or foreign capital markets.

In summary, while innovative financial instruments hold promise for addressing financing gaps for climate adaptation in urban India, a one-sizefits-all approach will not work. Debt-based instruments suit large cities with stronger credit ratings, while financial risk management instruments are preferable for smaller ULBs with constrained fiscal space. Results-based instruments, though challenging, offer the long-term benefits of accountability and performance incentives. Therefore, tailoring solutions to the financial health and institutional capacity of ULBs will be crucial to scaling adaptation finance sustainably.

To effectively access private capital, ULBs need to adopt structured capacity-building programmes. These may include:

The study underscores the importance of exploring innovative financial solutions to address the growing challenges of climate resilience in urban areas, and the adaptation finance gap. While various financial instruments and mechanisms have demonstrated significant potential to mobilise resources for climate adaptation, their successful implementation depends on a thorough understanding of the contextual requirements and unique socio-economic conditions of municipalities.

Municipal corporations must assess their financial, technical, and institutional needs before adopting a financial solution. This involves evaluating factors such as the revenue-generating potential of adaptation projects, the scale and scope of climate risks the regions face, and the existing capacity of local government bodies to implement and manage complex financial instruments. In the absence of such an understanding, even well-designed solutions may face operating or scalability challenges.

Furthermore, collaboration between public and private stakeholders is necessary to mitigate investment risks and ensure the sustainability of financial solutions. Policymakers and regulators must support municipal corporations by creating enabling environments, such as by offering technical assistance, reducing procedural burdens, and establishing frameworks for pooled financing. These measures will help cities unlock new financial resources and accelerate the implementation of climate-resilient infrastructure projects.

To translate these insights into action, ULB decision-makers should prioritise four immediate actions to enable adaptation finance:

These steps, combined with supportive policy frameworks from state and national governments, can help mainstream adaptation finance for urban development plans.

Traditional sources such as government grants and loans remain important but are insufficient to meet the additional adaptation financing needs. Innovative instruments like green bonds, pooled funds, and insurance mechanisms offer ULBs new ways to mobilise private capital, diversify their funding sources, reduce dependence on public finance, and improve their financial sustainability.

Without quantifying climate risks, ULBs cannot develop adaptation strategies and accurately estimate their financial needs or design bankable adaptation projects. Embedding risk assessments into the planning process helps cities prioritise investments in resilience-building infrastructure, and align them with financing instruments.

Because limited creditworthiness and narrow revenue bases make it difficult for smaller ULBs to raise capital independently from debt-based instruments like green municipal bonds. Pooled financing and insurance-based mechanisms reduce individual fiscal stress and give such municipalities collective bargaining power to buy insurance for their assets from climate change induced risk.

The compendium draws from both Global North and Global South experiences but prioritises examples from the Global South, given their socio-economic similarities to India and higher potential for replication.

State governments can unlock access by enabling pooled financing, offering credit enhancements, and creating clear regulatory pathways. Development partners and donors can complement these efforts by providing concessional finance, technical assistance, and capacity building to help ULBs pilot and scale resilience-focused instruments.

Roadmap of the methodology to assess the climate co-benefits of the SUP ban in Tamil Nadu

Unlocking finance for NbS in Indian Cities

Locally-led Climate Action in the Global South

Roadmap of the methodology to assess the climate co-benefits of the SUP ban in Maharashtra

Towards Climate-resilient Indian Industries: