Council on Energy, Environment and Water Integrated | International | Independent

Suggested citation - Wadhawan, Shreya, Anushka Maheshwari, and Vishwas Chitale. 2026. Towards Climate-resilient Indian Industries: Bridging Governance, Data, and Infrastructure Gaps through Collective Action. New Delhi: Council on Energy, Environment and Water

Indian industries are increasingly exposed to climate risks such as extreme heat, flooding, water stress, and supply-chain disruptions. While some leading firms have begun implementing targeted adaptation measures, climate resilience across the broader industrial ecosystem remains uneven. MSMEs, which form the backbone of India’s industrial value chains, face significant constraints in accessing climate data, finance, and technical expertise required to respond effectively to these risks.

This paper examines the policy landscape shaping industrial climate resilience in India and highlights lessons from industry case studies on how firms are managing climate risks. It finds that while technical solutions exist, scaling resilience requires stronger coordination across industries, improved access to climate information and finance, and closer alignment between industry action and public policy.

The report presents actionable recommendations for both industry and government stakeholders to accelerate climate adaptation across India’s industrial ecosystem. The study argues that climate resilience cannot be achieved through isolated firm-level action. Instead, coordinated approaches, such as industry coalitions, shared risk assessments, collective infrastructure investments, and stronger policy alignment are essential to scale adaptation across industrial clusters and value chains.

Increasingly, Indian industries are being exposed to the physical impacts of climate change, including extreme heat, flooding, water stress, and supply chain disruptions. By 2030, heat stress alone is projected to reduce India’s GDP by 4.5 per cent (Kjellström et al. 2019). Concurrently, southwest monsoon rainfall is expected to increase by 10–14 per cent, while the Northeast monsoon could become 10–50 per cent wetter, reinforcing the likelihood of compound and cascading climate risks from heat, flooding, and water stress (Prabhu and Chitale 2024). However, climate adaptation is not yet systematically embedded in core business planning, regulatory compliance, financial decision-making, or micro, small and medium enterprise (MSME) support ecosystems. As a result, industries continue to respond to climate impacts in a largely reactive manner, even as disruptions become more frequent, severe, and economically consequential.

Climate risks disproportionately affect MSME and industrial clusters, while also undermining India’s broader economic growth, export competitiveness, and development objectives. The materiality of climate risk for industry becomes clear when specific hazards are mapped to their direct operational and financial impacts. According to a report by the United Nations Economic and Social Commission for Asia and the Pacific (UNESCAP), India’s annualised average loss (AAL) from biological hazards, slow-onset hazards, and extreme events is estimated to be USD 93 billion, or 3.35 per cent of the country’s GDP (UNESCAP 2019). While India has a comprehensive climate policy architecture anchored in the National Action Plan on Climate Change (NAPCC), the National Adaptation Plan (NAP), and State Action Plans on Climate Change (SAPCCs), policy intent has not consistently translated into industry-relevant, on-ground resilience outcomes. Consequently, climate risks are not systematically accounted for, leading to underestimation of system downtime and cascading supply chain impacts, especially for smaller firms embedded in larger valuechains.

This implementation gap is driven by a combination of fragmented institutional mandates, weak regulatory and financial incentives for adaptation, limited access to decision-grade climate data, the absence of standardised industry-relevant resilience metrics, and uneven policy execution across states. Crucially, the scale and systemic nature of physical climate risks, cutting across shared infrastructure, labour pools, logistics networks, and regional ecosystems, are too large for any individual firm to address in isolation. Meanwhile, climate mitigation policies are more clearly operationalised through compliance frameworks, incentives, and reporting requirements, whereas adaptation remains largely advisory or voluntary. In the absence of clear mandates and measurable indicators, resilience investments are difficult to justify, track, and prioritise within routine capital expenditure and enterprise risk management processes.

This white paper assesses the current status of industrial climate resilience in India, examines the economic and operational impacts of inaction, and identifies the structural, institutional, and capacityrelated barriers constraining systematic adaptation across sectors and regions. Complementing the policy analysis, the white paper presents case studies and best practices from Indian industries and corporations that have begun integrating climate risk into business strategy, workforce protection, water management, and supply chain planning in chapter 4. Based on these examples the paper demonstrates that resilience-building is feasible, commercially relevant, and scalable, when supported by collective action, enabling institutional frameworks, access to data, and targeted finance.

India’s annual average loss from climate hazards is estimated at USD 93 billion, or 3.35 per cent of GDP (ESCAP 2019).

Key gaps and challenges in advancing Indian industries’ climate resilience

Key gaps include fragmented implementation across sectors and states, limited industry-facing operational guidance, low internal capacity, particularly among MSMEs, and the absence of standardised, industryrelevant metrics to assess and report climate risk and resilience outcomes. Existing sustainability disclosure frameworks, including the Securities and Exchange Board of India’s (SEBIs) Business Responsibility and Sustainability Reporting (BRSR) requirements, prioritise environmental and governance indicators, but do not uniformly capture physical climate risk or resilience investments. As a result, climate resilience remains weakly integrated into business strategy, capital expenditure decisions, and investment assessments.

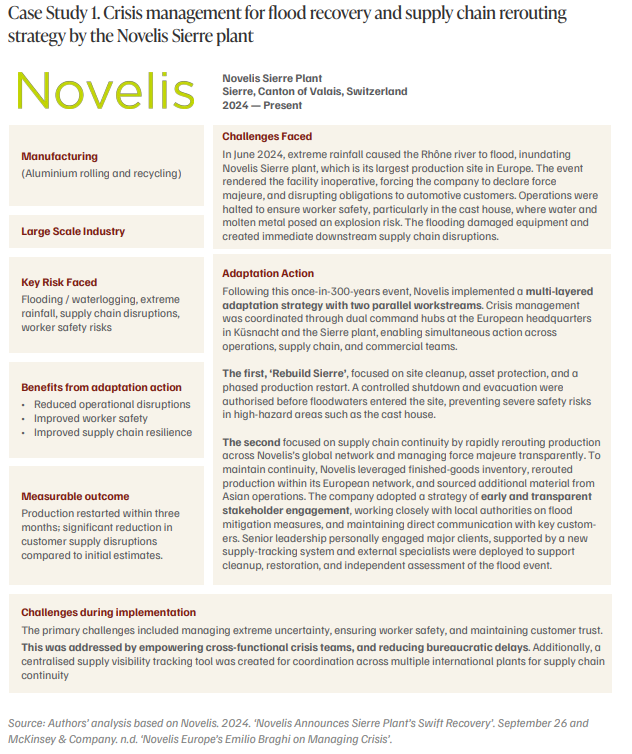

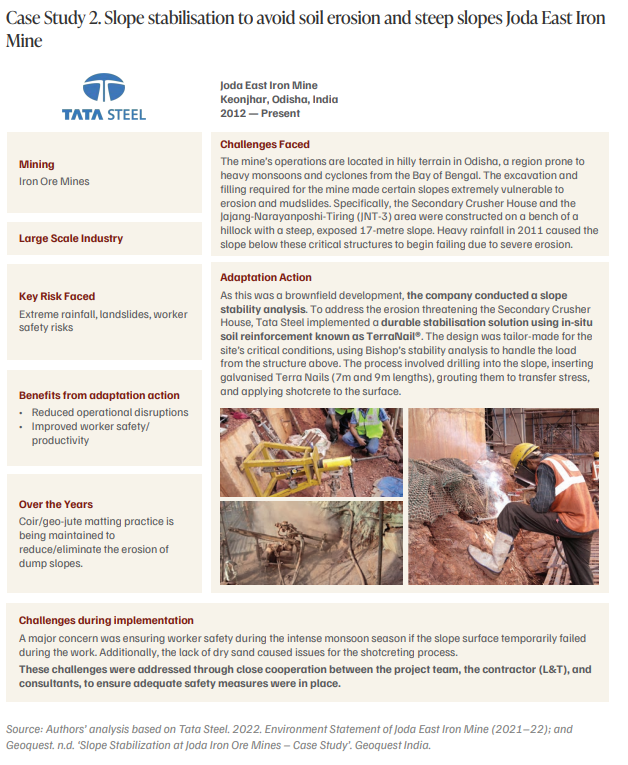

The case studies in this white paper illustrate severe physical risks, such as extreme rainfall in June 2024 flooded the Rhône River and inundated Novelis’s Sierre plant forcing a force majeure declaration at the facility, halting operations for safety, and disrupting automotive supply chains ( Novelis 2024). Similarly, heavy monsoons threatened critical infrastructure at Tata Steel’s Joda East Iron Mine, where slope erosion jeopardised the Secondary Crusher House (Tata Steel 2022). Furthermore, Godrej’s nature-based solutions sequester approximately 900,000 tons of carbon while acting as a buffer against storm surges and the urban heat island effect (Godrej 2025). Ultimately, proactive adaptation strategies enabled Novelis to restart production in under three months, significantly reducing downstream supply chain disruptions. These examples reinforce that climate adaptation is not a parallel safety function, but a core operational strategy that directly preserves human capital, productivity, and business continuity.

Why climate resilience matters now for India’s industrial competitiveness

Building climate resilience is not treated as a sustainability elective but a determinant of economic competitiveness. Several trends underscore why action is urgent:

• Continuity is becoming a market requirement: Global buyers increasingly expect resilient suppliers; climate-related disruptions can trigger order shifts and long-term loss of contracts.

• Finance and insurance are beginning to price physical climate risk: Premiums, exclusions, covenants, and due-diligence requirements are increasingly influenced by exposure to heat, floods, and water stress.

• Board-level relevance is rising: Physical climate risk is now an operational and financial risk, not a corporate social responsibility issue.

• Workforce constraints are intensifying: Heat stress, occupational safety risks, absenteeism, and productivity losses are growing across industrial regions.

• Shared infrastructure is a critical point of failure: Power, water, transport, and logistics systems underpinning industrial output are highly climate-exposed, amplifying systemic risk across value-chains.

Thus, this white paper notes that individual industry-level action alone is insufficient to address these systemic challenges. Instead, collective approaches are needed to reduce duplication of effort, improve access to climate risk information, and enable coordinated responses across value chains and industrial clusters.

Recommendations for Indian industry and private sector stakeholders

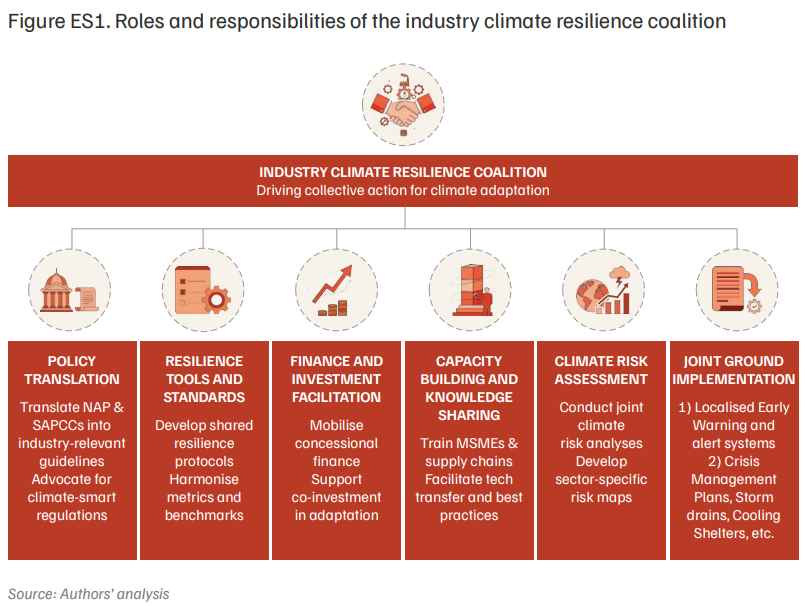

• Mainstream collective action and the role of industry collaboration

Drawing on global and domestic experience, the white paper makes the case for establishing a formal, cross-sectoral industry coalition on climate resilience to institutionalise collaboration and align private action with national and state adaptation priorities. The proposed coalition would function as a structured platform to translate climate policies into actionable, industry-relevant guidance. Its core functions would include developing shared climate risk assessment frameworks, harmonised resilience metrics, and sector-specific working groups focused on priority hazards such as extreme heat, flooding, and water stress.

By serving as an interface between industry and government, the coalition can strengthen investment readiness, lower the cost of adaptation through pooled investments, and support MSMEs that currently lack the capacity to act on identified risks.

• Conduct group-level physical climate risk assessment

Policymakers and industry bodies should encourage large industry groups and conglomerates to undertake group-level physical climate risk assessments, using a phased, materiality-based approach to manage cost, time, and resource constraints. This portfolio view enables prioritisation of high-risk assets, stress-testing of investments, and alignment of capital with long-term resilience, while generating spill over benefits for MSMEs and improving insurer, lender, and regulator engagement.

• Develop standardised site-level loss and damage guidelines

Develop integrated guidelines and SOPs for site-level assessment of climate-related loss and damage, covering asset damage, downtime, workforce impacts, supply-chain interruptions, and compliance costs aligning with global frameworks and IPCC methodologies. Standardised methodologies support consistent identification of vulnerabilities, prioritisation of adaptation actions, and comparability across sites, geographies, and sectors. The Resilience Coalition can facilitate wider adoption.

• Track adaptation investments and averted losses

Systematically quantify and disclose adaptation investments annually, alongside estimates of avoided losses and productivity gains over rolling five-year cycles. Standardised monitoring and evaluation metrics strengthen the business case for resilience, inform evidence-based policy and finance decisions, and create a feedback loop for improving adaptation strategies.

Policy recommendations for advancing industrial climate resilience in India

• Design a platform for government-industry climate resilience collaboration

Create a structured platform, hosted by the Ministry of Commerce and Industry (MoCI) and convened by the Department of Promotion of Industry and Internal Trade (DPIIT), to enable ongoing collaboration between industry coalitions and government. Recognised as implementation partners, coalitions, especially in manufacturing, infrastructure, energy, logistics, and MSMEs, will help embed climate resilience into industrial policy, approvals, land and corridor planning, and sector-specific guidance. State examples, like Telangana’s climate-adaptive industrial policy, show how risk-informed planning and resilient infrastructure standards can be mainstreamed nationally to strengthen regulatory clarity, investment certainty, and resilience outcomes.

• Establish dedicated financial and technical support mechanisms for industrial climate adaptation

The government should provide dedicated financial and technical support for industrial climate adaptation, tied to regulatory compliance. This includes subsidised climate risk assessments, concessional finance for resilient infrastructure, and technical assistance for climate-proofing supply chains, especially for MSMEs. Linking support to environmental clearances, industrial licensing, climate resilience certification for industry or their products, zoning approvals, or BRSR disclosures, would create consistent incentives. Global examples, like the EU’s LIFE Programme and OECD’s Adaptation Investment Framework, show how conditional finance embeds resilience into statutory planning, an approach that can be adapted for India.

• Strengthen the enabling ecosystem through data, capacity building, and regulatory reform

Improving access to high-resolution, decisionrelevant climate risk data; building technical capacity within state agencies, industrial clusters, and MSMEs; and piloting public-private adaptation initiatives are critical to overcoming capacity constraints. International experience, such as Japan’s Climate Change Adaptation Information Platform (A-PLAT), highlights the value of institutionally backed data platforms and public-private collaboration. Complementary updates to labour and occupational health and safety regulations, particularly for heat and flood risks, would further support worker-centred and operational resilience.

By positioning industry as one of the central actors in India’s adaptation agenda, rather than a passive recipient of climate impacts, this white paper outlines a pathway to strengthen industrial resilience, safeguard livelihoods, and support long-term economic stability. Institutionalised collaboration, supported by clear metrics, policy coherence, and targeted capacity-building, will be critical to ensuring that India’s climate policies translate into resilient industrial systems on the ground.

Collective approaches can reduce duplication, lower costs, and accelerate the diffusion of proven resilience solutions.

| Gap | What the gap looks like in practice | Why it matters for industry | Implication for policy and collective action |

|---|---|---|---|

| Fragmented policy and institutional landscape | Climate adaptation responsibilities sit primarily with MoEFCC, while industrial policy, competitiveness, and approvals are governed by the MoCI; disaster management frameworks remain oriented towards post-event response rather than anticipatory resilience. | This fragmentation prevents climate risk from being translated into actionable industrial policy. As a result, resilience considerations are weakly embedded in industrial approvals, compliance processes, infrastructure planning, and trade decisions, leaving firms without clear signals on when and how to invest in adaptation. | Establish an industry coalition as a structured interface for coordinated engagement with MoCI, MoEFCC, and NDMA, enabling climate adaptation priorities to be systematically embedded within industrial policy instruments and approval processes. |

| Limited access to decision-grade climate and extreme weather events data | Climate datasets exist at national or global scales but are not translated into site-, asset-, or cluster-specific operational insights usable by firms. | Without actionable data, firms struggle to assess material risks, prioritise investments, price insurance, or justify adaptation spending, constraints that are particularly binding for MSMEs with limited analytical capacity. | Enable coalition-led platforms to translate public climate data into actionable, sector- and cluster-level risk tools that directly support operational planning, investment decisions, and insurance engagement. |

| Limited financial and technical support for adaptation | Adaptation is largely framed as voluntary, with few incentives for climate risk assessments, resilient infrastructure upgrades, or supply-chain climate-proofing. | In the absence of financial or regulatory signals, firms defer resilience investments until losses materialise, reinforcing reactive rather than preventive responses and weakening the economic case for early action. | Use the coalition to aggregate demand, channel concessional and blended finance, and link adaptation actions to incentives, compliance mechanisms, and risk-based financing instruments. |

| Capacity constraints, especially among MSMEs | MSMEs face limited access to climate data, technical expertise, and upfront capital for adaptation. | High exposure among MSMEs creates weakest-link vulnerabilities across industrial value chains, undermining the resilience of even well-prepared lead firms and increasing systemic disruption risk. | Deliver cluster-level technical assistance, shared services, and pooled financing mechanisms through coalition-based programmes to strengthen value-chain-wide resilience. |

| Absence of standardised resilience metrics and disclosures | Existing reporting frameworks, including BRSR, emphasise environmental metrics with limited requirements on physical climate risk exposure or resilience outcomes. | Without standardised metrics, resilience investments remain invisible to boards, investors, insurers, and regulators, weakening accountability, comparability, and incentives for sustained adaptation. | Co-develop and pilot standardised, industry-relevant physical risk and resilience indicators through the coalition to improve transparency and investment decision-making. |

| Uneven state-level implementation | SAPCCs are weakly linked to state industrial policies, land-use planning, and regulatory approvals, with wide variation in implementation capacity across states. | Firms operating across states face inconsistent expectations, regulatory uncertainty, and limited guidance on integrating adaptation into investment and operational decisions. | Use the coalition to support alignment between SAPCC priorities, state industrial policies, and on-ground implementation mechanisms, improving consistency and scalability. |

Source: Author's analysis

Indian industry is already operating under conditions of heightened physical climate risk. Extreme heat, flooding, water stress, cyclones, and increasingly erratic rainfall patterns are no longer episodic shocks but persistent and material stressors shaping operational continuity, workforce safety, and asset performance. However, despite the growing severity and frequency of these hazards, climate adaptation remains weakly embedded in core business planning, regulatory compliance, financial decision-making, and MSME ecosystems. As a result, climate risk is often addressed reactively, rather than being systematically anticipated, priced, and managed.

This implementation gap is not due to a lack of policy intent or scientific evidence. India has a well-established climate governance architecture anchored in the National Action Plan on Climate Change (NAPCC), State Action Plans on Climate Change (SAPCCs), and the National Adaptation Plan (NAP). Yet, translation into industry-relevant action remains uneven. Fragmented institutional mandates, weak incentives for proactive investment, limited access to decision-grade climate data, the absence of standardised resilience metrics, and variable statelevel implementation collectively constrain action. These structural barriers are particularly acute for MSMEs, which form the backbone of India’s industrial supply chains but often lack the financial, technical, and informational capacity to assess and manage climate risks independently.

The implications of this disconnect are increasingly visible. Climate risks frequently remain unaccounted for in operational planning, resulting in unpriced system downtime, delayed restart times, and cascading supply-chain disruptions. Asset damage from floods and cyclones is compounded by prolonged recovery periods, while rising heat stress directly undermines labour productivity, occupational health, and worker safety. Waterand energy-intensive industries face growing exposure to resource volatility, and logistics and port disruptions amplify risks for export-oriented sectors. Together, these impacts translate into lost output, higher operating costs, workforce attrition, and rising exposure to insurance exclusions and tighter financing terms. These, in turn, become risks that are difficult to justify, monitor, or recover without systematic adaptation frameworks.

1.1 India’s escalating physical climate risk profile

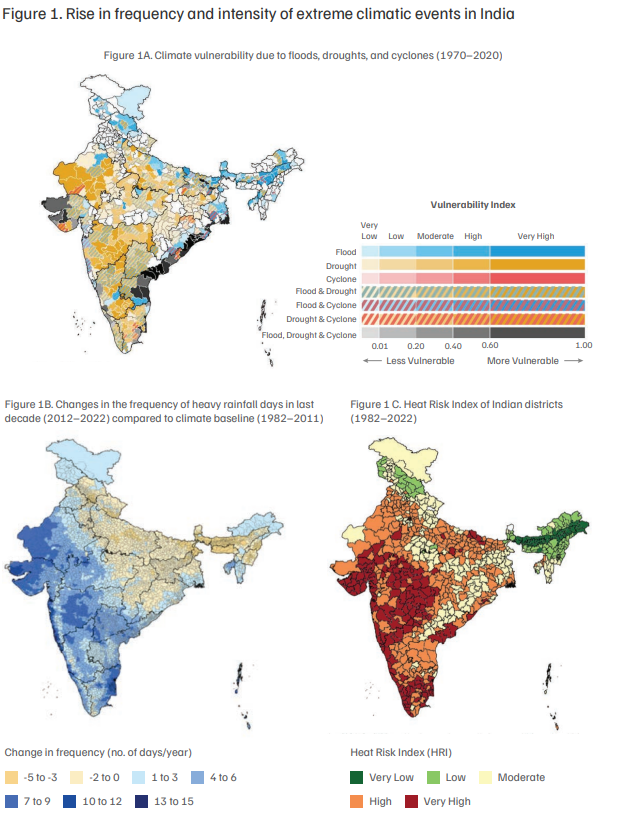

India’s climate hazard profile underscores the urgency of embedding resilience within industrial systems. Since 2005, the frequency and intensity of extreme weather events have significantly exceeded levels observed between 1970 and 2005 (Mohanty 2020). The Climate Vulnerability Index (CVI) shows that 75 per cent of Indian districts are hotspots for extreme climate events, exposing nearly 80 per cent of the population to compounded risks from floods, droughts, and cyclones (Mohanty and Wadhawan 2021). Nearly 40 per cent of districts exhibit ‘swapping trends’, where historically flood-prone regions increasingly experience droughts and viceversa, complicating risk planning and infrastructure design.

Extreme heat has emerged as a dominant and rapidly intensifying risk. In 2024, India recorded its hottest year on record, with several of the 23 heatwave-prone states experiencing their longest heatwave durations since 2010 (WHO 2024; IMD 2023). Warm nights are increasing at nearly twice the rate of hot days, approximately 8–10 additional warm nights per year compared to 4–5 additional hot days, severely constraining physiological recovery and labour productivity. Increase in heat stress estimates to bring productivity loss equivalent to 80 million jobs (ILO 2019). The World Health Organization attributes 37 per cent of heat-related deaths to human- induced climate change (WHO 2023). Heat-related deaths among those over age 65 have risen by 70 per cent in the last two decades. Over the last decade, nearly 70 per cent of districts experienced at least five additional warm nights per summer relative to historical baselines, with urban and industrial districts particularly affected due to heat island effects and rising humidity. Approximately 60 per cent of Indian districts are now classified as facing high to very high heat risk, where natural cooling thresholds are increasingly exceeded (Prabhu et al. 2025).

Rainfall patterns have simultaneously become more erratic and spatially uneven. Between 2012 and 2022, 55 per cent of India’s tehsils, many in historically drier states such as Rajasthan and Gujarat, recorded rainfall increases exceeding 10 per cent, while 11 per cent of tehsils, particularly across the Indo-Gangetic plains and Northeast India, experienced declines of up to 20 per cent in annual rainfall (Prabhu and Chitale 2024). The Northeast monsoon has intensified, increasing rainfall by over 10 per cent across several peninsular states, and nearly 48 per cent of tehsils have seen higher October precipitation, indicating delayed monsoon withdrawal and elevated post-monsoon flood risk (Prabhu and Chitale 2024).

This challenge is further compounded by increasingly erratic rainfall patterns, where intense precipitation over short durations overwhelms existing drainage and flood management systems.

Future projections point to further intensification of these risks. Under high- emission scenarios, average temperatures in India could rise by approximately 4.4°C by 2100, with a 70 per cent increase in warm nights and heatwaves occurring three to four times more frequently than historical norms (Krishnan et al. 2020).

Source: Mohanty, Abinash, and Shreya Wadhawan. 2021. Mapping India’s Climate Vulnerability. CEEW; Prabhu, Shravan, and Vishwas Chitale. 2024. Decoding India’s Changing Monsoon Patterns. CEEW, and Prabhu, Shravan, et al. 2025. How Extreme Heat is Impacting India. CEEW

1.2 Climate impacts on industrial operations

Climate-sensitive critical infrastructure systems, such as power, water supply, and transportation networks, are essential to uninterrupted industrial operations. However, the high climate sensitivity of these systems increases overall vulnerability and their impacts on businesses (UNEPFI 2023). Climate risks affect all layers of the industrial supply chain, ranging from physical assets to raw material availability, logistics and transportation, labour productivity, and finished goods. In 2021 alone, extreme heat led to an estimated loss of USD 159 billion in labour capacity across sectors, which is equivalent to 5.4 per cent of India’s GDP. The Department of Economic and Policy Research (DEPR) of the Reserve Bank of India (RBI) further estimates that up to 4.5 per cent of GDP could be at risk by 2030 due to lost labour hours from heat and humidity (RBI 2023).

Extreme weather events have both local and global effects on the supply chains and the industry. For example, a protracted drought in the Panama Canal in 2023–24 reduced the number of transiting cargo vessels by 36 per cent. This resulted in a 14 per cent increase in dry bulk shipping costs and an average delay of four additional sailing days, forcing businesses worldwide to reorganise supply chains at higher cost (McKinsey & Company 2024). The Chennai floods of 2015 were India’s most expensive disaster of the year, with estimated economic losses of USD 3 billion (NIDM 2021). Chennai’s business districts suffered significant operational losses; industrial hubs were shut down for weeks; and supply chain interruptions resulted in losses estimated at INR 15,000 crore.

Beyond direct asset damage, supply chain delays, and financial losses, sector-specific exposure to climate risk further illustrates the scale of vulnerability. Table 1 below provides an overview of the same. Capital-intensive sectors such as steel, cement, and aluminium face heightened exposure to flooding, heat stress, cyclones, and water scarcity, while labour-intensive sectors such as textiles, food processing, and logistics are particularly vulnerable to heat stress, workforce disruption, and infrastructure failures. Despite these risks, recognition and management of physical climate risk across industry remain at an early stage.

India’s mandatory Business Responsibility and Sustainability Reporting (BRSR) framework is at a very nascent stage for physical risk reporting, restricting disclosure to a brief 100-word description of disaster management plans, without explicitly mentioning or requiring detailed physical climate risk assessment (Prabhu et al. 2024). Data deficiencies, stemming from fragmented monitoring infrastructure and inconsistent datasets, limit the integration of real-time climate insights into business planning and reporting, creating significant challenges for industry compliance (Deloitte Touche Tohmatsu India LLP and Rainmatter Foundation 2025). As a result, climate adaptation is often perceived as a regulatory or compliance cost, rather than a strategic investment, particularly in the absence of standardised assessment frameworks and reliable local-scale data (CII 2025).

While some large corporations are diversifying supply chains (Nestlé’s 2021) and investing in water security (Ultratech n.d), a significant adaptation gap remains. This is particularly acute for MSMEs, which lack the financial and technical resources to implement robust adaptation measures (Ahuja et al. 2024). Given the interdependent nature of industrial production, vulnerabilities among suppliers, ancillary units, and logistics partners can undermine resilience, even where lead firms have invested in adaptation, highlighting the limits of isolated, firmlevel responses.

In 2021, extreme heat caused USD 159 billion in labour losses, about 5.4 per cent of India’s GDP (RBI 2023).

| Industry sector | Key sector importance* | Flooding/ waterlogging | Heat stress/ heatwaves | Cyclones/ storm surges | Drought/ water scarcity |

|---|---|---|---|---|---|

| Heavy industry (Steel, cement, aluminium) | Basic metals are the highest contributor to the country's Gross Value Added, contributing 11.56%. Basic metals also had the highest fixed capital invested, at 17.42% | Submerged furnaces, corrosion of equipment, long restart times, and high repair costs | Furnace efficiency loss, increased energy demand, and worker safety risks | Port damage affects raw material and export flows | Severe water constraints for cooling and processing forced capacity reduction |

| Agriculture and agro-processing | 54.6% of the population is engaged in agriculture and allied activities (Census 2011), and it contributes 17.4% to the country's GVA** | Crop loss, raw material shortages, contamination of storage facilities | Yield loss, livestock stress, processing inefficiencies | Plantation damage, input supply disruption | Crop failure, raw material price volatility |

| Food and beverage processing | Highest number of people engaged, ~2.16 million | Facility contamination, cold-chain breakdown, and inventory loss | Higher refrigeration loads, worker fatigue | Logistics and cold-chain disruptions | Water shortages for cleaning and processing |

| Textiles and garments | Second highest number of people engaged, ~1.71 million | Damage to looms and fabric stock, dye contamination | Heat stress affects labour-intensive operations | Supply chain delays, infrastructure damage | Water scarcity affects dyeing and finishing |

| Pharmaceuticals and chemicals | 7.24% share in GVA | Contamination risk, reactor shutdowns, compliance issues | Temperature-sensitive process risks, storage issues | Damage to hazardous material storage, transport risks | Water dependency for processing and safety systems |

| Transport and logistics | Supporting industry to all industries | Road, rail, port closures; cargo damage; supply chain delays | Reduced labour productivity, equipment overheating | Port shutdowns, vessel damage, and route disruption | Reduced inland water transport viability |

Source: Authors' analysis based on **MOSPI. 2018. Annual Survey of Industries, Chapter 8. Ministry of Statistics and Programme Implementation; and * MOSPI. 2025. Annual Survey of Industries 2023–2024 Summary Results.

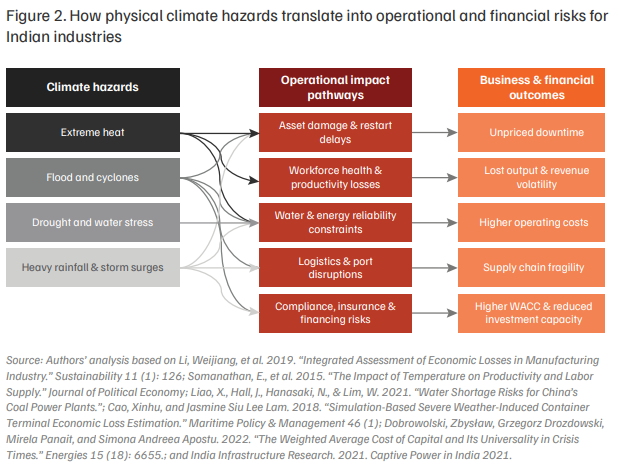

However, physical climate risks do not manifest as isolated environmental shocks; they propagate through identifiable impact pathways that translate meteorological hazards into operational disruptions, financial losses, and strategic constraints. Mapping these pathways is critical to understanding why climate adaptation is a core business and economic issue for industry, rather than a peripheral environmental concern.

These impacts increasingly propagate across value chains, shared infrastructure, and labour ecosystems, exposing the limits of firm-by-firm adaptation. While individual investments are necessary, they are insufficient to address risks that are systemic, spatially correlated, and interdependent across industrial clusters.

Moreover, as global buyers, financiers, and insurers increasingly incorporate physical climate risk into sourcing, pricing, and due-diligence decisions, these gaps carry direct implications for industrial competitiveness. They affect productivity, workforce safety, supply-chain reliability, and investment readiness, underscoring the need to reposition climate resilience as a core operational and economic priority rather than a peripheral sustainability concern.

Physical climate risks cascade into operational, financial, and strategic impacts.

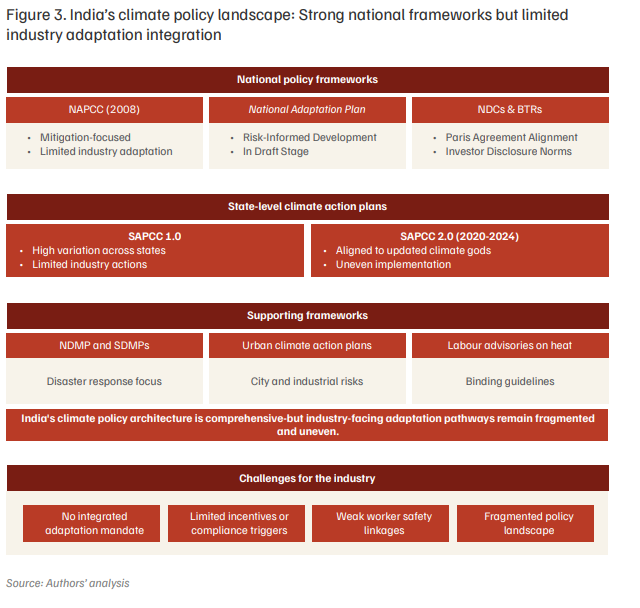

India’s climate governance and industrial policy environment comprises a layered ecosystem of national, state and sectoral instruments that influence how industries perceive and respond to climate risks. At the apex is the National Action Plan on Climate Change (NAPCC), established in 2008, which outlines strategic missions spanning energy efficiency, sustainable habitats, water, and strategic knowledge for climate resilience (MoEFCC 2008). These missions are designed to align climate mitigation and adaptation objectives with broader socioeconomic priorities; however, they have historically emphasised mitigation and energy transition outcomes over systematic adaptation planning for industrial sectors (Climate Change Academy. n.d.).

Additionally, state-level instruments such as State Action Plans on Climate Change (SAPCCs) articulate region-specific vulnerability and resilience priorities. These plans represented one of the largest subnational climate planning exercises in the world, providing initial frameworks for understanding local climate risk and guiding early adaptation measures. However, the articulation of industry-relevant actions varied substantially across states, often lacking harmonised metrics, dedicated implementation funding and mechanisms to support private-sector engagement. Recognising the need to update SAPCCs to reflect evolving national and international commitments, such as India’s Nationally Determined Contributions (NDCs) under the Paris Agreement, states have begun preparing revised SAPCC 2.0 documents since 2020 (Times of India 2025), with a growing number of updated plans emerging through 2024, including in major industrial states such as Delhi, Chandigarh, Odisha, Maharashtra and others1 . These revised plans aim to align state priorities with newer climate goals, integrate cross-sectoral resilience strategies and provide a stronger basis for coordinated implementation; however, many SAPCCs are still in draft or approval stages, and systematic integration of industry resilience remains uneven (GIZ 2024). Annexure A provides an overview of the status of SAPCC 1.0 and 2.0 for key states in India.

To address adaptation more explicitly, India is advancing a National Adaptation Plan (NAP) process to embed structured adaptation planning across sectors and scales. The NAP is intended to systematically integrate climate risk and vulnerability assessments into development planning, public investment and budgeting cycles, with clear relevance for industrial siting, infrastructure design, supply-chain management and workforce protection. As of January 2026, India’s NAP is understood to be in an advanced draft stage, with publication expected in the near term alongside updates to India’s climate reporting architecture, including NDC 3.0 and its first Biennial Transparency Report (BTR)2 (Business Standard 2025; Business Standard 2025; News On Air 2025). This alignment reflects a growing emphasis on adaptation as a core pillar of India’s climate commitments under the Paris Agreement, rather than a subsidiary component of mitigationfocused planning.

From an international negotiations perspective, the NAP intersects with emerging transition risks for Indian industry in the context of evolving global disclosure norms, climate-related trade measures and investor expectations. Transition risks3 , the financial and strategic risks associated with the global transition to a low-carbon economy, include changes in policy and legal frameworks, technology shifts, market preferences and investor behaviour that can materially affect asset values and corporate competitiveness, particularly for carbonintensive firms and sectors exposed to climate policy developments. Global climate risk disclosure frameworks such as the Task Force on Climaterelated Financial Disclosures (TCFD)4 and evolving regulatory proposals for climate risk reporting illustrate how investor expectations and market norms are shaping corporate governance and risk management practices worldwide (CPI 2018; Las 2025).

While adaptation planning under the NAP signals a shift towards risk-informed development, operational pathways for systematic industry engagement, such as sector-specific adaptation targets, incentives and integrated reporting mechanisms, remain under development. This limits the ability of firms to anticipate and respond to both physical and transition risks in an increasingly interconnected climate policy and market landscape. Figure 3 below illustrates this flow from national to state level policies.

Additionally, an important but often under-recognised dimension of industrial resilience are the working conditions of the labour under the ever-increasing extreme heat. The Ministry of Labour and Employment has repeatedly highlighted the need for protective measures for workers exposed to extreme hot weather. For instance, a statement released by the ministry outlines multi-sectoral recommendations for employers and industries to reschedule working hours, ensure adequate drinking water, improve ventilation, provide shaded rest areas, and conduct regular health check-ups for outdoor and manual workers to mitigate adverse effects of heat stress, and safeguard worker health and productivity (PIB 2024). However, despite these advisories, there is no legally binding standard in Indian labour law that mandates enforceable heat-specific occupational safety requirements, leaving significant gaps in protection for large segments of the workforce, including those employed in industrial, construction and supply chain activities (Acharjee 2025, UNDRR 2024). This absence of enforceable heat stress regulations constrains firms’ ability to integrate worker-centred climate adaptation measures into routine operational compliance frameworks, thereby weakening overall industrial resilience.

Complementary instruments such as the National Disaster Management Plan (NDMP) and state disaster management plans (SDMPs) provide procedural guidance for risk assessment and emergency response, which are pertinent for industrial continuity planning. Urban climate strategies, including City Climate Action Plans such as the Mumbai Climate Action Plan, integrate heat, flood, and infrastructure risks into metropolitan planning, signalling the relevance of resilience planning for industrial clusters embedded within urban ecosystems.

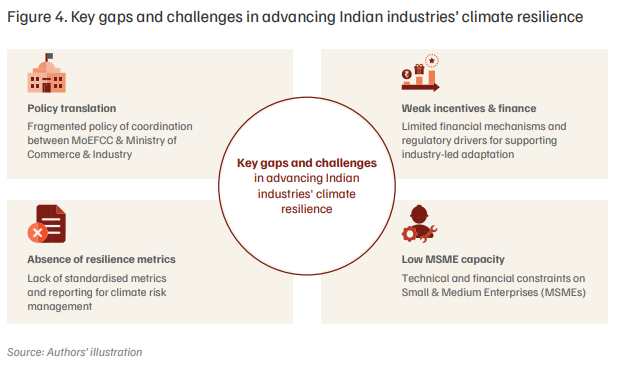

Despite a comprehensive national and state-level climate policy architecture, several structural, institutional, and operational gaps continue to limit the translation of policy intent into enhanced industrial climate resilience. These gaps constrain industries’ ability to anticipate, plan for, and systematically manage growing physical climate risks, even in the presence of sectoral guidelines and adaptation frameworks. The following sub-sections outline the key challenges shaping the current adaptation landscape for Indian industry.

3.1 Fragmented policy and institutional landscape

In India, climate resilience for industry is shaped by a fragmented policy and lack of a robust institutional environment. Climate change and adaptationrelated mandates are primarily anchored within the Ministry of Environment, Forest and Climate Change (MoEFCC), while industrial regulation, trade competitiveness, and sectoral promotion fall under the Ministry of Commerce and Industry (MoCI). Disaster management frameworks, meanwhile, remain largely oriented towards emergency response rather than proactive resilience-building and fall under the National Disaster Management Authority (NDMA) of India. The absence of structured coordination mechanisms across these domains has resulted in climate resilience being weakly embedded within industrial policy, investment approvals, and trade-related decision-making. Industries are often required to navigate overlapping mandates without clear guidance on prioritising resilience investments or aligning climate risk management with core industrial compliance requirements. As a result, adaptation remains peripheral to industrial strategy, with limited enforceable or incentive-based mechanisms to drive systematic uptake across value chains.

3.2 Limited access to decision-grade climate risk data

Access to high-resolution, decision-grade climate data remains a critical constraint for industry. While climate projections and hazard datasets exist at national and global scales, they are often not available in formats that support site-level decision-making, capital planning, or operational risk management. Industries, particularly MSMEs, face challenges in interpreting climate data, linking hazards to business impacts, and applying projections to asset design, supply-chain planning, or workforce management. This data gap leads to duplicated efforts, where firms independently commission risk assessments using varying assumptions and methodologies, resulting in inconsistent outputs that are difficult to compare, aggregate, or align with regulatory and financial requirements. The absence of trusted, standardised data platforms also weakens engagement with financiers and insurers, who increasingly seek credible, comparable assessments of physical climate risk.

3.3 Limited financial and technical support for adaptation actions

Financial and technical support mechanisms for industrial climate adaptation remain limited, fragmented, and weakly linked to regulatory frameworks. While mitigation-oriented incentives, such as energy efficiency subsidies and marketbased instruments, are embedded within compliance systems and linked to measurable outcomes, adaptation continues to be positioned largely as a voluntary or discretionary activity.

Support for climate risk assessments, resilient infrastructure upgrades, and supply-chain climateproofing is sporadic, and rarely tied to mandatory compliance obligations. This asymmetry weakens the business case for proactive adaptation, as firms face limited regulatory or financial signals to invest in resilience until climate impacts materialise. Consequently, adaptation investments are often deferred, reinforcing short-term decision-making and constraining the systematic integration of resilience into capital expenditure and operational planning.

India’s climate policy architecture demonstrates a clear contrast between how mitigation and adaptation are operationalised for industry. Mitigation actions are typically embedded within mandatory or quasi-mandatory compliance frameworks, supported by explicit incentives and penalties. For example, the Perform, Achieve and Trade (PAT) scheme links energy efficiency improvements to tradable efficiency certificates, while renewable energy obligations and disclosure requirements under BRSR create regulatory and market signals that reward compliance and penalise non-performance. These instruments reduce uncertainty for firms by clearly defining expected actions, timelines, and economic implications.

In contrast, adaptation measures, such as climate risk assessments, resilient infrastructure retrofits or supply-chain climate-proofing, are largely framed as voluntary or advisory, with limited linkage to compliance mechanisms or financial incentives. As a result, adaptation investments are often deferred, treated as discretionary costs rather than core operational requirements, despite growing physical climate risks. This policy asymmetry reinforces short-term decision-making and weakens incentives for industries to integrate resilience into routine planning and capital expenditure cycles.

Global evidence suggests this view is economically counterproductive: investing in adaptation can yield substantial returns, often exceeding USD 10 in benefits for every USD 1 spent over a decade when avoided losses, economic gains, and broader social benefits are accounted for, and average returns on analysed projects have been estimated at around 27 per cent (WRI 2025; WRI 2 2025; OECD-IEA 2022). By failing to embed adaptation into compliance and finance frameworks, regulators and firms miss significant opportunities to reduce future loss and damage, while enhancing long-term economic performance.

Source: Authors' analysis

3.4 Capacity and financing constraints, particularly for MSMEs

Capacity constraints remain a significant barrier to industrial adaptation, particularly for MSMEs. Many MSMEs lack in-house expertise to conduct physical climate risk assessments, limited access to actionable climate data, and insufficient financial buffers to absorb upfront adaptation costs. These constraints restrict their ability to retrofit infrastructure, climate-proof supply chains, or implement workforce protection measures, especially within climate-exposed industrial clusters (UNEPFI 2023; RBI 2023). As a result, resilience investments are frequently deprioritised in favour of short-term operational expenditures, even as climate risks increasingly disrupt labour productivity, logistics, and business continuity.

However, emerging experience demonstrates that MSMEs can act as early movers in adaptation when supported by enabling ecosystems. For instance, the Ghana Climate Innovation Centre has enabled climate-smart MSMEs through technical advisory services, early-stage finance, and incubation support (World Bank 2019; GCIC n.d.). Similar cooperative models in Kenya and Namibia have supported MSME-led adaptation through shared infrastructure and local knowledge systems (UNEPCC 2018). In India, initiatives such as WRI India’s Resilient, Inclusive, and Sustainable Enterprises (RISE) programme have strengthened MSME adaptive capacity by providing access to climaterisk tools, data, and technical guidance (WRI India 2022). These examples highlight that while capacity constraints remain structural, targeted support can unlock scalable MSME-led resilience.

3.5 Absence of standardised industry-relevant metrics and reporting frameworks

The lack of standardised, industry-relevant metrics for physical climate risk and resilience outcomes remains a critical gap. Existing sustainability reporting frameworks, most notably BRSR, focus predominantly on environmental disclosures and do not uniformly mandate quantified physical climate risk or resilience indicators (SEBI 2023; T20 Brazil 2024). Current requirements often capture only highlevel qualitative information, such as brief references to disaster management plans, limiting comparability across firms and sectors.

This absence of harmonised metrics reduces the visibility of resilience investments to boards, investors, and regulators, weakening incentives for proactive adaptation (CII IESD 2025; G20 Finance Working Group n.d.). For SMEs embedded within value chains, the cost and complexity of data collection further exacerbate uneven disclosure and potential trade barriers. Strengthening disclosure frameworks to incorporate standardised, costeffective, and interoperable physical climate risk indicators, aligned with SAPCC priorities and the National Adaptation Plan, would be critical to improving transparency, accountability, and decisionmaking for industrial resilience (OECD 2019; Prabhu et al 2024).

3.6 Uneven state-level implementation and limited access to decision-grade climate data

State Action Plans on Climate Change (SAPCCs) are intended to operationalise national adaptation priorities by articulating state-specific vulnerabilities and sectoral actions. Where SAPCCs are relatively mature and institutionally anchored, they provide a useful platform for engagement with industry on risk assessment, infrastructure resilience, and workforce protection. However, across many states, SAPCCs remain weakly linked to industrial policy instruments, land-use planning, and regulatory approvals, with limited specification of industry-facing actions, timelines, or accountability mechanisms.

In the absence of standardised metrics, dedicated budgets, and clearly defined institutional mandates, SAPCCs often function primarily as strategic planning instruments rather than fully operational frameworks. Implementation is further influenced by varying levels of technical capacity within state climate cells and coordination challenges between environment departments and industryfacing agencies, affecting the pace and consistency of on-ground action (GCA 2024). As a result, firms operating across multiple states encounter uneven expectations and limited guidance on integrating adaptation into investment and operational decisions.

Compounding these challenges, access to decisiongrade climate data remains limited. While national and global datasets exist, they are rarely translated into high-resolution, site-specific insights required for plant-level adaptation, infrastructure design, or supply-chain planning. This data gap constrains risk assessment, investment prioritisation, and the effective scaling of resilience measures, particularly for MSMEs and firms operating in climate-exposed clusters.

In sum, while India’s climate policy architecture provides a strong foundation for industrial climate resilience, realising its potential requires targeted enhancements. Stronger linkage between mitigation and adaptation within industrial strategies, dedicated financial and technical support mechanisms, standardised resilience metrics, improved access to decision-grade climate data, and strengthened institutional capacity at the state level are all critical. Addressing these gaps will be essential to enabling industries to systematically integrate climate resilience into strategic planning and operational execution.

The lack of standardised, industryrelevant metrics for physical climate risk and resilience outcomes remains a critical gap.

This section presents a set of case studies and best practices drawn from individual industries, corporations, and conglomerates that illustrate emerging efforts by the private sector to build climate resilience and advance adaptation. The examples highlight how leading firms are assessing physical climate risks, investing in adaptive infrastructure and processes, and integrating resilience considerations into operational planning, supply chain management, and workforce protection. While these initiatives remain uneven and largely voluntary, they demonstrate the practical pathways through which industry can operationalise adaptation, complement public policy objectives, and contribute to longterm economic resilience under increasing climate variability.

| Resilience capability | Illustrative case | What was done | Why it matters |

|---|---|---|---|

| Supply-chain agility as a core resilience capability | Novelis—Sierre plant | Pre-defined crisis playbooks enabled rapid rerouting of production across global facilities; decentralised decision-making allowed real-time operational responses and transparent force majeure management. | Asset protection alone is insufficient; flexibility and decision autonomy across supply chains are critical to minimising downtime and customer disruption during extreme events. |

| Site-specific technical solutions for climate-exposed assets | Tata Steel—Joda East Iron Mine | Tailored slope stabilisation, soil reinforcement, and drainage systems designed for monsoon-intensive conditions | Generic engineering standards fail in high-risk geographies; granular risk assessment and context-specific design are essential to reduce erosion, landslides, and operational disruption. |

| Nature-based solutions as functional resilience infrastructure | Godrej—Vikhroli Campus | Scientific conservation and management of mangrove ecosystems to buffer storm surges, reduce coastal erosion, and mitigate urban heat. | Nature-based solutions can operate as 'green infrastructure', delivering asset protection alongside co-benefits such as water security, heat reduction, and carbon sequestration. |

| Resilience beyond the fence-line through upstream value-chain engagement | ITC—Mission Sunehra Kal | Community-level interventions in water stewardship and climate-smart agriculture to stabilise raw material supply | For agro-based and water-dependent industries, resilience depends on strengthening adaptive capacity across rural supply bases, not just within factory boundaries. |

| Standardised protocols for scalable workforce protection | Aditya Birla Group—Heat Stress Framework | Group-wide, data-driven heat stress management using a three-step approach, from qualitative risk screening to physiological monitoring and engineering controls. | Harmonised protocols enable consistent identification and mitigation of occupational climate risks across diverse sites, improving scalability and compliance. |

| Worker safety as an integral component of operational resilience | Cross-cutting across all cases | Flood protection, slope stabilisation, and heat mitigation measures designed to protect both assets and workers. | Climate adaptation is a core operational strategy that preserves human capital, productivity, and business continuity is not a parallel safety function. |

4.2 The need for collective climate action

The sectoral risk analysis and industry case studies presented in this paper reveal a clear divergence in industrial climate resilience. Leading firms, including Novelis, Tata Steel, ITC, Godrej, and the Aditya Birla Group, demonstrate that climate resilience is achievable through targeted technical and organisational interventions. These range from asset-level flood protection and heat mitigation to water stewardship, supply-chain diversification, and workforce protection measures. Collectively, these examples confirm that adaptation solutions exist and can deliver tangible business value by reducing downtime, stabilising operations, and safeguarding productivity. However, these efforts remain isolated pockets of excellence, rather than system-wide norms. Despite the availability of technical solutions, resilience has not scaled across industrial clusters or value chains.

MSMEs, which form the backbone of India’s industrial ecosystem, often lack the financial capacity to replicate capital-intensive interventions undertaken by larger firms. At the same time, access to decisiongrade climate data remains limited, standardised resilience metrics are largely absent, and uneven state-level implementation of climate policies creates regulatory uncertainty for firms operating across multiple jurisdictions. Together, these constraints make resilience investments difficult to prioritise, justify, and track, particularly beyond individual facilities. Moreover, the barriers identified are not merely firm-level capacity gaps but structural, collective-action challenges. Firms operating within the same geographies or value chains often face common hazards, such as extreme heat, flooding, or water stress, yet continue to undertake climate risk assessments and adaptation planning in isolation.

Several of the most binding constraints are, therefore, inherently collective in nature. These include duplication of climate risk assessments, weakest-link vulnerabilities in supply chains, free-rider dynamics around shared infrastructure, and coordination failures in workforce protection and emergency preparedness.

Individual firm-level adaptation, while necessary, is insufficient to protect interconnected industrial systems or ensure continuity across value chains, particularly where MSMEs and ancillary units remain exposed.

Global experience demonstrates that collective approaches can help overcome these barriers. Shared knowledge platforms and pooled technical expertise have enabled firms and investors to translate climate science into decision-relevant metrics. For example, the Coalition for Climate Resilient Investment (CCRI) facilitated the joint development of physical climate risk assessment methodologies that improved investment decision-making for infrastructure and industrial assets (CCRI 2021; World Economic Forum 2022). Such collective mechanisms decrease transaction costs, and expand access to high-quality risk information, especially for smaller firms.

Similarly, early warning systems (EWS) for extreme heat, flooding, and cyclones are most effective when designed at the scale of industrial clusters rather than individual facilities. Evidence from India’s citylevel heat action plans shows that timely warnings, supported by coordinated preparedness actions, can significantly reduce mortality and productivity losses (WMO 2021; WHO 2023). Extending such shared climate intelligence systems to industrial estates can enable anticipatory actions such as shift rescheduling, equipment protection, logistics rerouting, and workforce safety measures, particularly where firms rely on common infrastructure and labour markets.

Collective investment in adaptation infrastructure also offers significant efficiency gains. Measures such as stormwater drainage upgrades, flood retention systems, water recycling infrastructure, and cooling and shading interventions are often more costeffective when implemented at the level of industrial estates or economic zones. International experience with eco-industrial parks demonstrates how shared infrastructure planning can reduce climate-related disruptions while improving resource efficiency (UNIDO 2017; UNEP 2021), particularly in climateexposed coastal and riverine regions.

For MSMEs, collective platforms can play a critical role in lowering barriers to adaptation by pooling resources, providing shared technical assistance, and enabling access to finance through aggregated demand. Evidence from cluster-based programmes indicates that MSMEs are more likely to adopt adaptive practices when supported through cooperative models and shared services (World Bank 2019; UNEPFI 2023). Embedding MSMEs within collective initiatives, such as shared risk assessments, joint training, and common infrastructure upgrades, strengthens resilience across entire value chains rather than concentrating it within a few large firms.

Beyond operational benefits, collective industry action also provides strategic value for policy alignment and scale. Structured industry platforms offer governments a practical interface to translate national and state adaptation priorities, such as those under the National Adaptation Plan and SAPCCs, into implementable, sector-specific actions. Global experience suggests that adaptation advances most effectively when collective industry efforts are aligned with public policy objectives, and supported by enabling regulatory and financial frameworks (OECD 2024; Global Commission on Adaptation 2019).

4.3 The role of insurance and parametric solutions in industrial climate resilience

An important but underdeveloped dimension of industrial climate resilience is the role of insurance as both a risk-transfer and risk-signalling mechanism. Traditional indemnity-based insurance often performs poorly under climate extremes due to delayed payouts, high transaction costs, and limited coverage for indirect losses such as downtime and supply-chain disruption.

Parametric insurance, which triggers payouts based on predefined hazard thresholds (e.g., rainfall, temperature, wind speed), offers faster and more predictable liquidity, particularly when designed using sub-national or cluster-level climate data. For industry, integrating insurance alongside physical adaptation measures can help manage residual risk, stabilise cash flows, and improve engagement with lenders and investors. At the same time, insurers require decision-grade, locationspecific climate risk data to price products accurately and scale coverage, especially for MSMEs. Collective industry platforms can help bridge this gap by aggregating demand, sharing risk assessments, and enabling pooled insurance arrangements, making insurance a viable component of systemic industrial resilience rather than a standalone financial product.

In India, parametric insurance has been piloted primarily in the agriculture and disaster risk management space, but its relevance for industry is increasingly recognised. For instance, rainfall- and cyclone-triggered parametric products developed with support from global reinsurers and multilateral agencies have enabled faster post-event payouts to state governments and local institutions, reducing fiscal stress after extreme events.

Similar approaches are now being explored for urban flooding and extreme heat, including city-scale heatrisk financing mechanisms linked toHeat Action Plans. Extending these models to industrial clusters, ports, and logistics corridors, using location-specific thresholds and shared exposure data, could help industries manage escalating physical climate risks while improving engagement with insurers and lenders.

Taken together, the evidence indicates that scaling industrial climate resilience in India requires moving beyond fragmented, firm-byfirm responses. Collective action is not merely a coordination mechanism, but a necessary enabler of scalable, cost-effective, and inclusive adaptation, capable of addressing shared risks, strengthening value-chain continuity, and translating policy intent into durable industrial practice.

Drawing on the evidence from sectoral risk analysis, case studies, and policy gaps identified in the preceding sections, this chapter outlines a set of targeted recommendations to strengthen climate resilience across Indian industry. The recommendations are structured to reflect the differentiated roles of industry, policymakers, and financial actors, while emphasising the need for coordinated and scalable action.

5.1 Recommendations for industry partners

Industry actors are central to translating climate risk recognition into operational resilience. The following recommendations focus on actions that industry partners can undertake, individually and collectively, to embed climate adaptation within strategic planning, investment decisions, and value-chain management, while aligning with emerging national and state policy priorities.

Industry partners should establish a formal coalition to institutionalise collaboration on climate resilience.

This should be a cross-sectoral coalition, align private sector action with public policy priorities, and accelerate the uptake of adaptation solutions. The coalition should function as a structured platform to translate national and state climate policies, particularly the NAP and SAPCCs, into actionable, industry-relevant guidance and implementation pathways. Global and national precedents demonstrate the feasibility and value of such coalitions. The Coalition for Climate Resilient Investment (CCRI), launched at the UN Climate Action Summit in 2019, shows how cross-sector coalitions can translate physical climate risk into investmentgrade metrics through shared methodologies and strong anchoring in global policy processes, with participation from financial regulators and multilateral development banks (CCRI 2021; WEF 2022). Similarly, the UN Global Compact’s CEO Water Mandate illustrates how collective industry platforms aligned with public governance priorities can harmonise metrics, enable co-investment in resilience, and demonstrate business value through reduced operational and supply-chain risks (UN Global Compact 2023).

Thus, the coalition should focus on operationalising existing climate risk assessment frameworks, such as the Physical Climate Risk Assessment Framework (PCRAF)5 by CII and CEEW, and the physical climate risk investor playbook6 by UNEP to reduce duplication of effort and implement strategic action. Further, the coalition should work towards developing harmonised resilience metrics, and sector-specific working groups addressing priority hazards such as extreme heat, flooding, and water stress. Membership should be inclusive, with differentiated engagement models for large firms, MSMEs, and industrial clusters, enabling collective action while recognising varying capacities. Positioned as an interface between industry and government the coalition can strengthen investment readiness, reduce duplication of effort, and scale proven resilience practices across value chains.

Bridging the policy-practice gap: India has a growing suite of climate and industrial policies, yet uptake by industry remains uneven due to fragmented guidance and limited implementation support. A formal coalition can act as a translation mechanism, converting policy intent under SAPCCs, labour advisories, disaster management plans, and industrial guidelines into operational standards, toolkits, and sector-specific action plans that firms can adopt at scale.

Strengthening the business case through quantification: Global evidence consistently shows that investment in adaptation delivers high economic returns. The Global Commission on Adaptation estimates that every USD 1 invested in climate adaptation can generate USD 2–10 in net economic benefits, through avoided losses, productivity gains, and reduced disruption (GCA 2019). For heat-related risks alone, the ILO estimates global productivity losses could reach USD 2.4 trillion annually by 2030, underscoring the economic rationale for proactive industry-led resilience (ILO 2019). A coalition can standardise methodologies to quantify avoided losses, return on resilience investments, and productivity gains, strengthening board-level and investor confidence.

What the coalition enables:

Addressing low-capacity and high-risk contexts: For many MSMEs and smaller industrial actors, risk identification alone does not translate into action due to limited technical expertise, data access, and financial headroom. Collective mechanisms, such as shared climate risk assessments, pooled technical assistance, and common access to climate data platforms, can significantly lower entry barriers. By sharing resources and expertise, the coalition can enable firms operating in low-capacity contexts to move from awareness to implementation.

How the coalition helps:

Mobilising finance and protecting supply chains and workers. Coalitions can unlock joint financing mechanisms, blended finance partnerships, and pooled procurement of resilience solutions, reducing costs for individual firms. Coordinated action across supply chains can enhance continuity and reduce cascading disruptions. In parallel, collective adoption of worker protection measures, such as heat action protocols aligned with government advisories, can safeguard labour productivity and reduce occupational health risks under rising temperature extremes.

Source: Author's analysis

Industry should undertake group-level physical climate risk assessment

Policymakers and industry bodies should encourage large industry groups and conglomerates to undertake group-level physical climate risk assessments, using a phased, materiality-based approach to manage cost, time, and resource constraints. An initial light-touch screening or heat-mapping exercise across all assets and operations, domestic and international, can be used to identify priority geographies, asset classes, and value-chain nodes exposed to high climate risk. This first stage enables firms to rapidly distinguish material risk hotspots from lower-risk assets without undertaking resource-intensive sitelevel analysis across the entire portfolio.

Building on this screening, firms can then undertake deeper, site-specific risk assessments for identified hotspots, using structured frameworks such as PCRAF (CII 2025), RISE (WRI 2023), or the ITC Next Strategy (ITC 2023). This sequenced approach allows companies to move beyond isolated site diagnostics towards a portfolio view of exposure, while ensuring that analytical effort and capital are directed where risks are most acute. Group-level assessments conducted in this manner support prioritisation of high-risk assets, stress-testing of investment plans, and alignment of capital allocation with long-term resilience objectives.

Incentivising such phased group-level assessments can also generate spillover benefits for MSMEs embedded in industrial value chains, by identifying shared risks and enabling targeted support where vulnerabilities are concentrated. In addition, a structured, portfolio-level understanding of climate exposure can improve disclosure quality and enable more consistent engagement with insurers, lenders, and regulators, without imposing disproportionate upfront burdens on firms.

Standardised methodologies with sector-specific SOPs and checklists can enable firms to identify vulnerabilities, and prioritise adaptation actions.

Develop and implement standardised guidelines for site-level L&D assessment

Industry bodies should develop refined, integrated guidelines for site-level assessment of climaterelated loss and damage (L&D) for industrial facilities. These guidelines should define what constitutes L&D, covering direct asset damage, production downtime, workforce disruption, supplychain interruptions, environmental remediation, and compliance-related costs. A standardised methodology with sector-specific SOPs and checklists can support consistent application across industries and geographies, enabling firms to systematically identify vulnerabilities, prioritise adaptation actions, and embed climate risk considerations into routine operational and safety planning. Such guidance would also improve comparability across sites and states, strengthening the credibility of reported impacts. Such guidelines could also be operationalised through the Industry Resilience Coalition to enable a wider uptake and implementation across sectors.

Institutionalise tracking of adaptation investments and averted losses at the site level

To strengthen the economic case for resilience, industries should be encouraged to systematically quantify and disclose adaptation investments at the site level on an annual basis, alongside estimates of losses averted due to these interventions. A structured monitoring and evaluation (M&E) framework should require firms to assess avoided downtime, reduced asset damage, and productivity gains over a rolling five-year cycle, aligned with financial planning and asset lifecycles. Standardising these metrics would enable better evaluation of return on adaptation investments, support evidence-based decisionmaking by financiers and insurers, and create a feedback loop to refine adaptation strategies over time. At the policy level, such data can inform targeted incentives, risk-based regulation, and public–private co-investment in resilience.

5.2 For government stakeholders

Government action is critical to creating the enabling conditions for industrial climate resilience. While industries can undertake risk assessments and implement adaptation measures, scaling resilience across sectors and value chains requires coherent policy signals, institutional coordination, and integration of climate risk considerations into core economic planning and regulatory frameworks. The following recommendations focus on how government stakeholders can move from fragmented, advisory approaches towards structured, implementation-oriented engagement with industry.

Establish a platform for governmentindustry engagement on climate resilience

A structured platform of engagement should be created to enable continuous collaboration between industry coalitions and government stakeholders to mainstream climate resilience into industrial policy, investment planning, and regulatory frameworks. This platform should be hosted by the Ministry of Commerce and Industry (MoCI), with the DPIIT convening meetings and facilitating coordination with other relevant ministries, including Environment, Labour, Power, Steel, Heavy Industries, MSME, Ports, and Logistics. Under this platform, the industry coalitions should be formally recognised as implementation partners, particularly for priority sectors such as manufacturing, infrastructure, energy, logistics, and MSMEs.

The platform should focus on embedding climate resilience into core industrial planning instruments by issuing sector-specific adaptation guidance, integrating climate risk screening into industrial approvals, land allotments, corridor planning, and expansion plans, and aligning objectives across industrial, environmental, labour, and disaster management policies. State-level examples, such as Telangana’s climate-adaptive industrial policy, illustrate how risk-informed site planning, water security, heat mitigation, and resilient infrastructure standards can be integrated into industrial development rather than treated as standalone environmental measures (Telangana Industrial Infrastructure Corporation 2016). Scaling such approaches nationally through the platform will enhance regulatory clarity, strengthen resilience outcomes, and provide long-term certainty for investment and competitiveness.

Establish compliance-linked financial and technical support for industrial adaptation

Government stakeholders should establish dedicated financial and technical support mechanisms for industrial climate adaptation that are explicitly linked to regulatory and policy compliance frameworks. Building on the success of mitigation-oriented instruments, adaptation support should move beyond voluntary guidance towards structured incentives and conditionalities. This can include subsidised or co-financed climate risk assessments, concessional finance for resilient infrastructure upgrades, and targeted technical assistance for climate-proofing supply chains, particularly for MSMEs embedded within industrial value chains. Linking access to such support with compliance instruments, such as environmental clearances, industrial licencing, climate resilience certification for industry or their products, zoning approvals, or BRSR-linked disclosures, would create clearer and more consistent signals for industry action.

Global experience demonstrates the effectiveness of linking adaptation finance with regulatory requirements. For instance, the European Union’s LIFE Programme, with a budget of EUR 5.4 billion, co-finances business-led adaptation projects, with eligibility often linked to compliance with regional development plans and environmental regulations, thereby embedding resilience within statutory planning processes (ClimateAdapt 2020). Similarly, the OECD’s Climate Adaptation Investment Framework highlights how public financial institutions and development banks use concessional debt finance and blended finance instruments to support enterprises’ adaptive capacity, including loans conditioned on resilience and risk management criteria (OECD 2024). Embedding such conditional adaptation finance within India’s regulatory ecosystem would help normalise resilience as a core operational requirement rather than a discretionary investment.

Strengthen the enabling ecosystem for private-sector adaptation through data access, capacity building, and regulatory reform

In parallel, governments should strengthen the enabling ecosystem for private-sector adaptation by improving access to decision-relevant climate data, technical capacity, and institutional support. This includes providing high-resolution, localised climate risk information that is usable at industrial and operational scales; supporting capacity building for state officials, industrial clusters, and MSMEs; and co-developing pilot projects with industry coalitions to translate policy intent into on-ground resilience outcomes. Such measures are critical for addressing persistent capacity constraints that limit the uptake of adaptation actions, especially among smaller firms.

Additionally, India can learn from Japan’s Climate Change Adaptation Information Platform (A‑PLAT), which is deployed as a centralised information platform to help stakeholders, both public and private, access climate risk information and develop adaptation measures (IEA 2021). This platform is underpinned by Japan’s Climate Change Adaptation Law, which institutionalises adaptation planning and promotes public-private collaboration on resilient infrastructure and business risk management. Complementing data and capacity support with updates to labour, occupational health, and safety regulations, particularly to address risks such as extreme heat and flooding, would further enable firms to integrate worker-centred adaptation into routine compliance frameworks, strengthening industrial resilience holistically.

Government stakeholders should establish dedicated financial and technical support for industrial climate adaptation, linked to regulatory compliance.

India’s policy architecture on climate change, industrial development, and disaster risk reduction provides a strong foundation for advancing industrial climate resilience. However, as this white paper demonstrates, resilience outcomes will remain uneven unless adaptation is systematically embedded within industrial policy, compliance frameworks, investment decisions, and state-level implementation processes. Escalating physical climate risks, such as heat stress, flooding, water scarcity and supply-chain disruption are no longer peripheral concerns, but material determinants of industrial productivity, workforce safety, and long-term competitiveness. Addressing these risks requires a decisive shift from fragmented, advisory approaches towards coordinated, risk-informed, and implementation-oriented action across government and industry.

A critical priority for the coming decade is to institutionalise climate resilience within India’s economic governance systems. This includes strengthening coordination between climate and industrial ministries, embedding adaptation considerations within approvals, zoning, and licencing processes, and aligning national instruments such as the NAP with SAPCCs and industrial development strategies. Equally important is streamlining the current policy asymmetry between mitigation and adaptation by establishing dedicated financial and technical support mechanisms for resilience that are explicitly linked to compliance and incentives. Global evidence consistently shows that early investment in adaptation yields high economic returns by avoiding future losses, protecting labour productivity, and safeguarding infrastructure.

At the same time, industry must move from isolated firm-level responses to collective, systems-oriented action. Shared climate risks, such as flooding within industrial estates, heat stress affecting workforces, and disruptions to common logistics and water infrastructure, cannot be effectively managed by individual firms alone. Formal industry coalitions on climate resilience can play a catalytic role by translating national and state policies into actionable guidance, pooling data and technical expertise, developing harmonised risk metrics, and enabling joint investments in early warning systems and shared adaptation infrastructure.