Council on Energy, Environment and Water Integrated | International | Independent

Suggested citation: Kesh, Christi, Aparna Sharma, and Vaibhav Chaturvedi. 2025. Unlocking India’s Voluntary Carbon Market: Challenges and the Path Forward. New Delhi: Council on Energy, Environment, and Water.

India has launched an offset mechanism within its Carbon Credit Trading Scheme, which now would be operating alongside private voluntary standards, to channel finance toward high‑integrity mitigation. In this issue brief, we analyse early‑stage procedural bottlenecks, especially project registration, in India's voluntary carbon market using available private registry data and stakeholder interviews, with the goal of informing efficient design of the CCTS offset mechanism. We recommend an institutionalised, quarterly briefing to the National Steering Committee for Indian Carbon Market (NSCICM) and a set of operational fixes to minimise early-stage delays and innovative approaches to diversify the project pipeline.

The Government of India has launched the Carbon Credit Trading Scheme (CCTS) offset mechanism under the Indian Carbon Market (ICM) framework. This mechanism will serve as a government‑certified standard within the voluntary carbon markets in India, distinct from independent certification standards such as Verra, Gold Standard etc. This new mechanism mirrors the operational structure of the private voluntary markets and involves a similar set of stakeholders. India has a long history with carbon markets—starting with its participation in the Clean Development Mechanism (CDM) under the Kyoto Protocol to its engagement with current voluntary markets—all of which have been offset-based systems.

While these markets have immense potential to boost climate ambition, they might also introduce significant uncertainty. Key challenges arise from informational silos, misaligned interests, and unequal resource distribution among stakeholders. These issues often manifest as operational inefficiencies that can limit the overall effectiveness of the market.

In this study, we examine the procedural dynamics and assess the key challenges faced by offset-based projects in India, with a particular focus on existing VCMs. Our analysis focuses explicitly on the early stages of the credit issuance cycle—particularly the registration phase to identify early-stage procedural bottlenecks, such as project registration delays, sectoral vulnerabilities, and related issues such as limited sectoral participation—that hinder market operations. The objective is to inform the development of the offset mechanism within the ICM. Our research combines quantitative analysis of project timeline delays with qualitative insights from expert stakeholders on these quantitative findings. Our study interprets data from the Verra Verified Carbon Standard (VCS) Registry, which contains over 70 per cent of the world’s offset projects.

The Verra VCS divides project types into 16 sectoral scopes. Under these scopes, various projects, activities, and methodologies can be developed. Projects can be grouped with various components, such as other scopes and ongoing projects, to scale mitigation efforts. We designed a mixed-methodological framework to evaluate registration timelines, sectoral participation patterns, and delays in the early stages, specifically in project registration In India and the rest of Asia within the existing VCMs. Our study uses data processing, descriptive statistical techniques, and expert stakeholder interviews to examine challenges and provide recommendations to mitigate them in the upcoming CCTS offset mechanism.

The comprehensive dataset, which includes registered and unregistered projects, included 2,800 projects from 80 countries; we focused the scope of our work on India and the ROA. We calculated registration timelines as the difference between listing and registration dates. We determined the interquartile range to assess registration delays and used the third quartile (Q3) values to benchmark registration timelines. Consequently, we compared these benchmarks against all the remaining unregistered projects in India within the VCS pipeline to identify registration delays. Additionally, data were analysed for sectoral vulnerabilities and participation to provide more robust insights. Furthermore, we interviewed three expert industry stakeholders using unstructured interviews to validate these results and understand their views and perspectives on the delays.

To address these challenges, we recommend an institutionalised monitoring and reporting structure to regularly brief the National Steering Committee for Indian Carbon Market (NSCICM) and take its guidance on various challenges that the ICM faces. Specifically, we recommend that the NSCICM be briefed quarterly vis-à-vis:

Carbon markets will be a game changer in advancing climate action (World Bank 2024). There is a global need to raise emission reduction ambitions to combat global warming. To this end, well-operating carbon markets are essential to accelerate carbon reduction and removal as well as support the financing of decarbonisation, especially in developing economies.

Currently , carbon markets operate in two main forms. The first is through emission trading schemes (ETS), whereby companies are expected to meet intensity-based or absolute targets for emission reductions. To do so, they can buy and sell allowances/carbon credits. For example, the Government of India’s CCTS includes a compliance mechanism based on a baseline and credit system: companies that emit less than the assigned baseline earns carbon credits, which can then be sold to companies that exceed their limits. Similarly, the European Union’s ETS follows a cap-and-trade model, where in the total amount of emissions permitted is set, and companies must hold enough allowances to cover their emissions, trading these as needed. The second is project-based carbon markets, also called offset-based carbon markets, which include mechanisms that enable emission reduction projects to generate tradable carbon credits. These include the compliance offset markets under Article 6 of the Paris Agreement; the erstwhile CDM under the Kyoto Protocol (Broekhoff et al., 2025); privately operated voluntary carbon markets (VCMs)- such as Verra and Gold Standard; and government-run voluntary schemes, such as India’s CCTS - offset, which was launched in December 2023.

Thus, carbon offsetting is a sub-category under the larger umbrella of carbon markets. While the terms’ carbon offset’ and ‘carbon offset credit’ may be used interchangeably, they represent two related but different activities. A carbon offset refers to a project/activity undertaken to reduce or remove GHG emissions to compensate for emissions that occur elsewhere. In contrast, a carbon offset credit is a transferable instrument certified by a government or independent certification body that represents an emission reduction of 1 metric tonne (Mt) of CO2 or an equivalent amount of other GHGs. The purchaser of an offset credit can ‘retire’ these credits to meet their GHG reduction goals.

Offset credits are used by countries, companies, and individuals to balance their emissions by paying for climate-positive activities undertaken by a separate entity. This is because GHGs mix globally in the atmosphere, so it does not matter where they are reduced. Consequently, if an organisation (a) halts an activity that causes emissions or (b) causes/finances emission-reducing activities elsewhere in the world, the overall impact on climate change remains the same. Properly functioning carbon markets can provide the most efficient and cost-effective emission reduction options.

India has rich experience in the offset markets. The CDM has been operational since 2006 and remained highly relevant in the early 2000s with the introduction of EU-ETS until 2012. CDM enabled emission reduction and removal projects in developing countries to earn certified emission reductions (CERs), each equivalent to 1 tonne of CO2 (e). These credits could be traded, sold, and used by industrialised countries to meet a part of their emission reduction targets under the Kyoto Protocol. It was estimated that India would produce 16 per cent of the world’s CERs by 2010 and would become one of the most significant contributors globally by 2012 (The Economic Times 2010).

In the early 2000s, parallel to the development of market mechanisms under the Kyoto Protocol and the introduction of the European Union’s ETS, the voluntary market emerged and strengthened rapidly after 2007 (Kärt Johanna Ojamäe 2024). The formation of certification bodies such as Gold Standard (2003), Verra (2005), and Climate Action Reserve (2001) helped mobilise private-sector players to make voluntary commitments towards offsetting their GHG emissions.

Currently, the major VCM certifiers include the Verified Carbon Standard (VCS; 2006) and the Sustainable Development Verified Impact Standard (SD Vista; 2024) launched by Verra, the Gold Standard established by the World-Wide Fund for Nature (WWF) in 2003, and the Plan Vivo Standard created by the Plan Vivo Foundation in 2001. Economies in South Asia, South America, the Caribbean, and Africa are significant suppliers to VCMs. India, in particular, is a major contributor (Dyck et al., 2023). For example, between 2010 and 2022, India issued 278 million carbon credits traded in VCMs, accounting for 17 per cent of the global supply. Despite the many challenges surrounding integrity, demand and credit prices around project-based offsets within the voluntary market, India’s revenue from voluntary carbon credits is projected to reach USD 20–40 billion by 2030 (Singh and Ghosh 2023; India’s national carbon market to seek links with international registries. S&P Global Commodity Insights).

In December 2022, the Government of India amended the Energy Conservation Act, 2001, establishing a framework for the Indian carbon market (ICM). Subsequently, in June 2023, the central government notified the CCTS. The CCTS includes an offset mechanism that allows nonobligated entities to register projects that use government-established sectoral methodologies to account for GHG reductions and removals. These projects are then allowed to issue carbon credit certificates (CCCs).

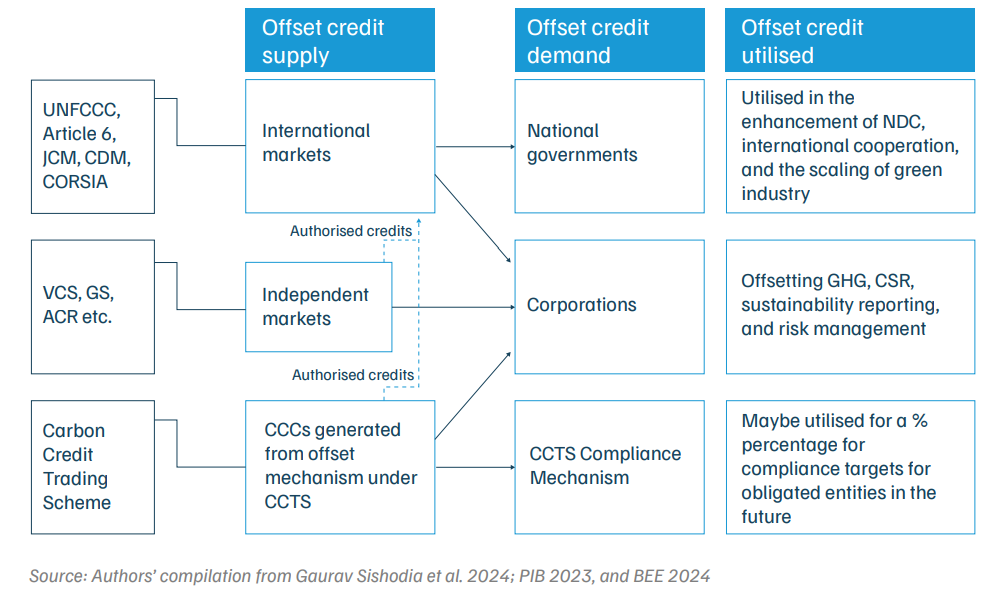

In India, offset market credits are used in several ways: in the United Nations Framework Convention on Climate Change (UNFCCC) compliance markets under Article 6, a voluntary offset mechanism within the CCTS for non-obligated entities, and other private VCMs. Figure 1 illustrates the various types of carbon markets and interlinkages in India.

Figure 1. Types of offset markets currently operating in India

Carbon markets are complex governance arrangements (Ahonen et al. 2022). They are driven by policy and operate across various governance levels, involving both public and private sectors. These markets have independent governance structures, connected through formal market links or aligned through information exchange, capacity building, and the shared aim of meeting international climate mitigation commitments (Burtraw et al. 2013).

While these market mechanisms have the potential to enhance climate ambition, they also introduce uncertainty. The VCMs are fragmented and unregulated, leading to regulatory gaps and inefficiencies. Further complications may arise due to the presence of informational silos and the misalignment of interests and resources among stakeholders (Betz et al. 2022). As discussed earlier, India has a high volume of offset projects registered with various independent certifying authorities, which engage a wide range of actors in this ecosystem. Effective management of offset projects is imperative for India to secure climate investment, advance sustainable development, integrate corporate climate ambitions, supply high-integrity credits, and develop robust processes to facilitate the effective management of project resources.

In this study, we investigate the procedural dynamics of project-based offset systems, focusing on the registration phase of the project cycle using data from the Verra VCS Registry. We aim to identify inefficiencies in this phase and make recommendations to mitigate issues early on. Further, we aim to provide guidance for the development of an efficient and well-coordinated offset mechanism framework within the CCTS.

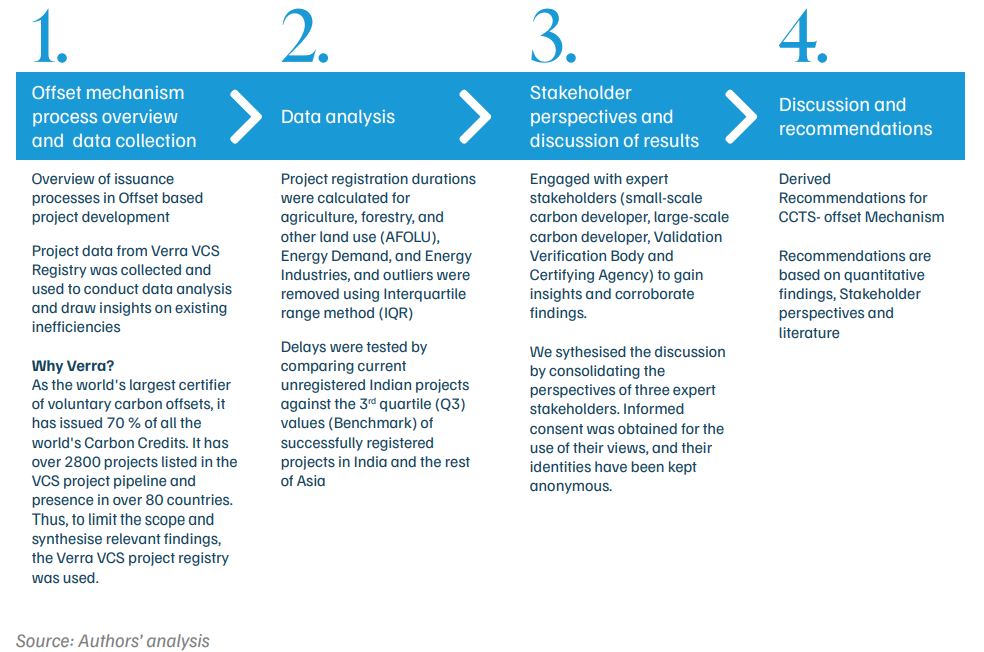

We followed a four-step process to understand and draw insights on the early stages of the credit issuance cycle of Verra VCS projects as listed on the publicly available VCS Registry (as of January 2024). The approach is illustrated in Figure 2.

Verra’s Verified Carbon Standard (VCS) is one of the world’s most widely used voluntary frameworks for certifying GHG emission reduction projects. Initially launched in 2005 as the Voluntary Carbon Standard by Climate Wedge and Cheyne Capital, it was designed to ensure rigour and transparency in carbon offset projects that operate outside of Compliance/regulated markets (Verra,).

Figure 2. Approach of the study for understanding bottlenecks in voluntary carbon market processes

The VCS covers a broad range of project types, and each project must adhere to approved methodologies that guide the calculation and monitoring of emission reductions. Independent third-party verifiers, called validation and verification bodies (VVBs), assess these projects. After successful validation, registration, verification, and tracking, carbon credits called verified carbon units (VCUs), representing tCO2-eq, are issued. These credits must be real, verifiable, and additional; double counting should be avoided. In this section, we give a procedural overview of VCS’s credit issuance cycle (Verra,).

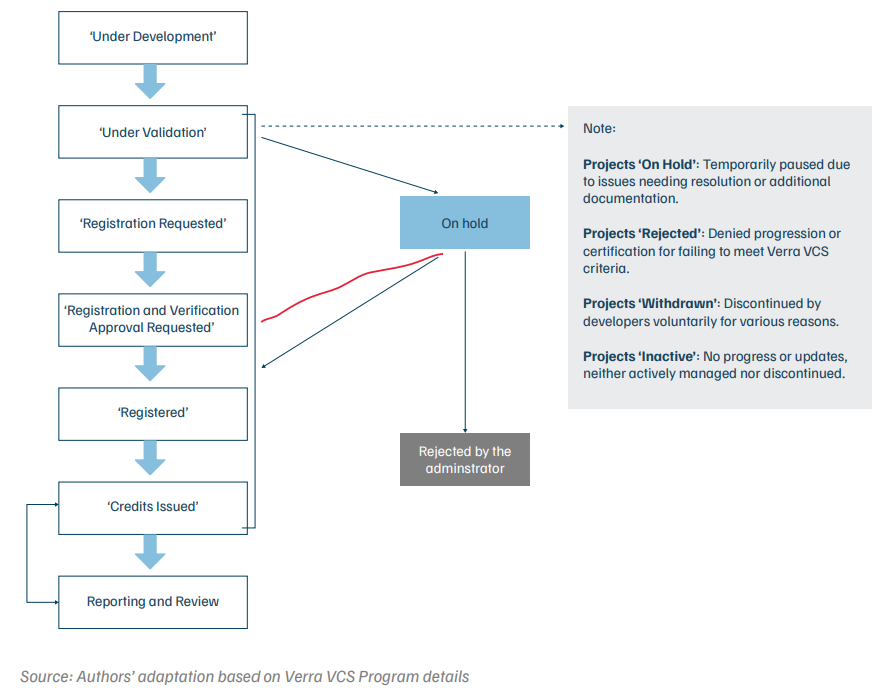

Most certifying agencies have similar processes for developing carbon offset projects. Figure 3 illustrates the procedural flow of project development, validation, verification, and issuance of credits.

Figure 3. Procedural flow of credit issuance cycle

Note: This study focuses primarily on the registration phase. The scope of our analysis is limited to this stage because it provides the most consistent data, allowing us to identify delays in the early stages of project timelines. While critical, the subsequent monitoring, reporting, and verification stages are subjected to more variability and are outside the scope of this analysis.

The VCS categorises project types into 16 sectors. Projects, activities, or methodologies can be developed under these sectoral categories. Projects can include various components – from other sectors and ongoing projects – to scale mitigation efforts. We compiled the potential for GHG mitigation in India from multiple reports. Table 1 gives an overview of 16 sectors.

Table 1. Sectoral scopes and mitigation potentials

| S. No | Sector | Description and initiatives | Mitigation potential in India |

|---|---|---|---|

| 1 | Energy industries | Emissions are reduced through renewable energy use and/or fossil fuel efficiency. Examples include renewable energy projects such as solar, wind, and hydro, and efficiency upgrades in fossil fuel plants. | High |

| 2 | Energy distribution | Energy enhancement to enable lower transmission losses using smart grids and improved infrastructure. | Low |

| 3 | Energy demand | Reduction of emissions from industries and appliances via the implementation of energy-efficient tech and industrial energy management systems. | Medium |

| 4 | Manufacturing industries | Reduction of emissions in the manufacturing sector through process optimisations and efficiency upgrades. | High |

| 5 | Chemical industry | Reduction of emissions through cleaner production methods, energy recovery, and decreased use of carbon-intensive materials in chemical processes. | Low |

| 6 | Mining/mineral production | Energy improvement and emission reductions in extraction and processing through automation, process optimisation, etc. | Medium |

| 7 | Metal production | Reduction of emissions through advanced smelting, waste heat recovery, and integration of renewable energy in metal production processes. | Low |

| 8 | Construction | Reduction of emissions by using recycled/eco-friendly materials, energy-efficient designs, and modular construction methods. | Low |

| 9 | Transport | Emission reductions through improved fuel efficiency, vehicle electrification, and improved mass transit. | High |

| 10 | Fugitive emissions (fuels) | Capture of emissions during fossil fuel extraction and distribution through methane recovery and improved pipeline sealing. | Low |

| 11 | Fugitive emissions (industrial gases) | Minimisation of leakage of high-global-warming gases by replacing high global warming potential (GWP) substances and enhancing containment and recovery systems. | Low |

| 12 | Solvent use | Reduction of emissions by substituting high-emission solvents with eco-friendly alternatives and improving solvent recycling in industrial processes. | Low |

| 13 | Waste handling and disposal | Reduction of GHGs such as methane through recovery and capture, recycling, composting, waste-to-energy projects, and biogas facilities. | High |

| 14 | Agriculture, forestry, and other land use (AFOLU) | Reduction and removal of emissions via sustainable agriculture, forest management, afforestation/reforestation, and peatland restoration. | High |

| 15 | Livestock and manure management | Reduction of methane emissions from livestock by improving manure management, implementing biogas recovery, and dietary interventions to reduce enteric fermentation. | Moderate |

| 16 | Carbon capture utilisation and storage (CCS) | Capture of CO₂ from industrial processes securely storing or utilising it; for example, in concrete or via geological sequestration. | High |

VVBS conduct validation and verification to vet projects listed under Verra VCS. They are independent third-party auditors accredited by Verra who evaluate whether a project complies with all relevant VCS guidelines. During the validation phase, VVBs assess whether a project meets certain criteria to be eligible for registration under the VCS programme. During the verification phase, they evaluate whether a project has accurately quantified and achieved the outcomes outlined in its documentation. VVBs must meet specific criteria outlined in the guidelines of the particular programme. This includes accreditation by a VCS-recognised body, authorisation by Verra, and payment of an annual fee to Verra. VVBs may lose their accreditation due to non-compliance or failure to perform responsibilities.

Credit issuance cycle

The credit issuance cycle consists of multiple phases. Until January 2024, the Verra VCS Registry only provided phase-wise data for the stages illustrated in Figure 4.

Figure 4. Phases of the credit issuance cycle according to VCS data availability in its registry

While this study primarily analyses data from the Verra VCS Registry, the landscape of carbon offset standards is diverse. An overview of other prominent standards, such as the Gold Standard and the CDM, offers valuable insights into methodology, procedural frameworks, and the integration of sustainable development objectives. Table 2 presents a brief overview of other popular standards.

Table 2. Comparative overview between major Carbon Market Standards

| Aspect | Clean Development Mechanism | Gold Standard | American Carbon Registry |

|---|---|---|---|

| Governance and Accounting |

|

|

|

| Scope and eligibility |

|

|

|

| Environmental integrity |

|

|

|

| Monitoring, reporting, and verification (MRV) |

|

|

|

Table 3. Availability of methodologies under standards

| Sectors | Number of methodologies (CDM) | Number of methodologies (Gold Standard) | Number of methodologies (VCS) |

|---|---|---|---|

| AFOLU | 12 | 14 | 19 |

| Energy demand | 31 | 27 | 10 |

| Energy industries | 59 | 25 | 19 |

| Waste handling and disposal | 22 | 21 | 21 |

| Transport | 22 | 20 | 8 |

| CCS | 0 | 3 | 1 |

| Fugitive emissions | 19 | 1 | 6 |

| Construction | 2 | 1 | 5 |

| Manufacturing industries | 28 | 7 | 7 |

| Chemical industries | 23 | 6 | 3 |

| Energy distribution | 9 | 3 | 3 |

| Mining and metal industries | 9 | 2 | |

| Total | 236 | 128 | 104 |

We designed the methodological framework for this study to evaluate procedural timelines, sectoral participation patterns, and delays in project registration within the ICM. We used data from the Verra VCS Registry, which was subsequently cleaned and processed. We analysed the data using descriptive statistical techniques to estimate registration timelines, delays and deviations from the timelines, and project distribution and diversity. This section provides a concise overview, with detailed steps and results elaborated under Annexure 1.

Key methodological steps

1. Data collection and cleaning

2. Data set organisation

The master dataset was segmented into thematic sheets for ease of analysis. These included:

3. Statistical analysis

4. Sectoral diversity assessment

5. Derivation of results and graphs and engagement with sector experts

Our analysis is limited by the granularity of data in the Verra VCS Registry, as it lacks detailed phase-wise information through the credit issuance cycle. We have developed sector-specific generalised timeframes using Q3 values to provide liberal estimates for each sector. The delay testing was performed by comparing the timelines of each unregistered project with the sectorspecific timeline set under the ROA benchmark. ROA was compared because it has a sectoral distribution similar to that of India. It should be noted that other countries, such as Turkey, have a similar sectoral distribution; however, we limited the scope to Asia for analysis purposes. Furthermore, the analyses consider only the three major sectors – AFOLU, energy industries, and energy demand – for delay comparison because the highest number of projects in India’s VCS portfolio belong to these sectors.

Building on the methodology described in Section 2, we analysed projects in the Verra registry to quantify registration delays and sectoral participation patterns.

Our objectives were twofold: first, to benchmark how quickly projects move from listing to formal registration in India relative to the ROA, and second, to map which sectors Indian developers actively engage in and the reasons that influence participation. We structured the presentation of findings into two parts:

Two key factors influence the observed time difference between project listing and registration. First, there is a time lag between listing a project and the VVB initiating the audit process. This delay can result from scheduling constraints and the need for preparatory documentation, internal review procedures, and internal stakeholder consultations with the certification body. Second, once the audit begins, the VVB must complete a comprehensive review of the project’s data through multiple rounds of validation, stakeholder consultations, and checking compliance with the project description. This validation process can also lead to delays in the registration phase. The available data do not allow for differentiation between these two factors; thus, we selected a more liberal Q3 value for benchmarking timelines.

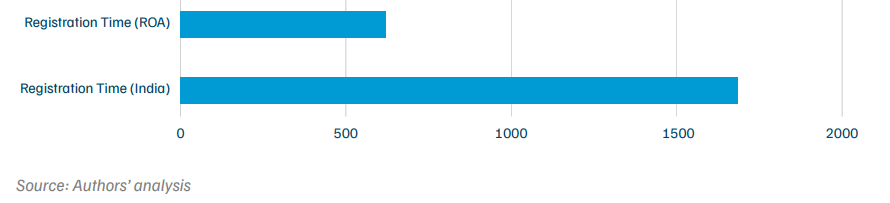

The number of registered AFOLU projects in India is notably low, with only 10 successfully registered compared to over 108 in the issuance cycle. Moreover, only 8 per cent of AFOLU projects in India are registered, compared to more than 20 per cent in the ROA. Among the registered projects, 75 per cent of India’s projects took more than 1,689 days to be registered, while in the ROA, 75 per cent of the projects required only 623 days. These three observations indicate that prolonged registration timelines are prevalent in India, demonstrating that AFOLU projects in India generally take much longer to register than those in other parts of Asia. Figure 5 shows India’s significantly longer registration timelines for AFOLU projects than the ROA.

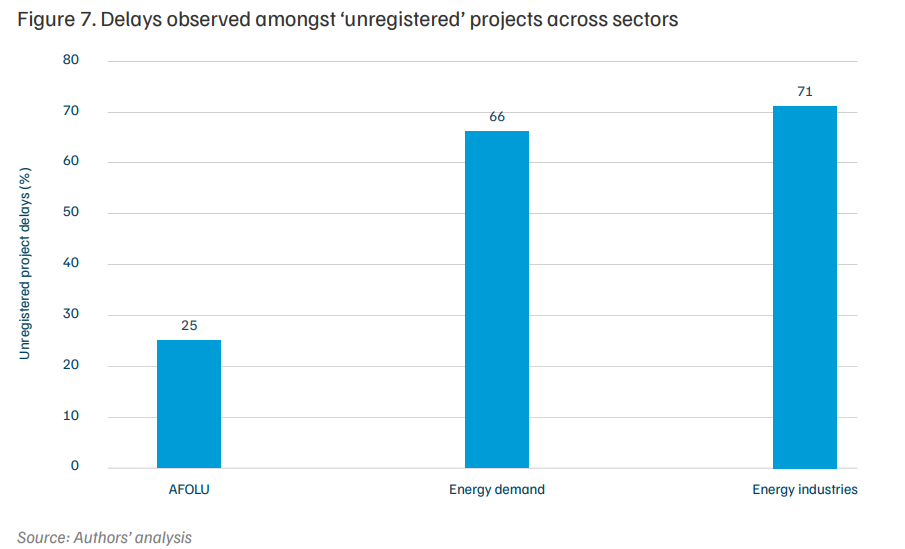

When unregistered projects are evaluated and delays are compared to the ROA benchmark of 623 days, it is revealed that approximately 25 per cent of unregistered Indian AFOLU sector projects are experiencing delays in registration timelines. Although Indian AFOLU projects face fewer delays than other sectors in India (such as the energy sector), their overall timelines remain significantly longer than those in the ROA.

Another critical statistic on AFOLU projects further clarifies the current trends and challenges in the AFOLU sector. This is related to sectoral vulnerabilities that exacerbate timeline delays. Sectoral vulnerability implies the number of projects on hold or rejected for various reasons. Among all projects in the registry – registered and unregistered, across 84 countries – the AFOLU sector has the highest proportion of projects put ‘on hold’ or ‘rejected by the administrator’. Specifically, 93 per cent of all global on-hold projects and 81 per cent of all global rejected projects belong to this category.

Figure 5. AFOLU projects in India take significantly longer to be registered when compared to the ROA

Energy sector–related projects have been broadly classified into two categories: energy industries and energy demand (Refer table 1 for sector related description). We found that the energy industries sector in India has been the most active in this area over the past decade, with over 75 successfully registered projects. More than 75 per cent of these registered projects in India take at least 360 days to register successfully.

While this indicates that, historically, registration timelines in India have been shorter than those in the ROA for the energy industries sector, the current trend in India tells a different story. Extended delays are evident among the 60 unregistered projects in India currently listed in the VCS Registry. Analysing these projects against the benchmark (427 days) reveals that 71 per cent of unregistered energy industries projects have already exceeded this threshold. This indicates that, in India, the highest delays among unregistered projects are observed in the energy industries sector.

In the energy demand sector, the Q3 benchmark for project registration in India is 536 days, based on data from 31 registered projects. This is closely aligned with the Q3 benchmark of 534 days for projects in the ROA, derived from 30 registered projects. The similarity in these values, combined with the substantial number of projects in this sector in India, indicates that energy demand projects in India have historically demonstrated a degree of procedural efficiency.

However, current trends reveal substantial delays among the 102 unregistered projects in India in this sector. When these projects are evaluated against the ROA benchmark of 534 days, approximately 66 per cent are found to have exceeded this threshold, signalling significant delays. Although this percentage is lower than the 71 per cent observed in the energy industry sector, it still represents a considerable portion of projects that experience extended timelines.

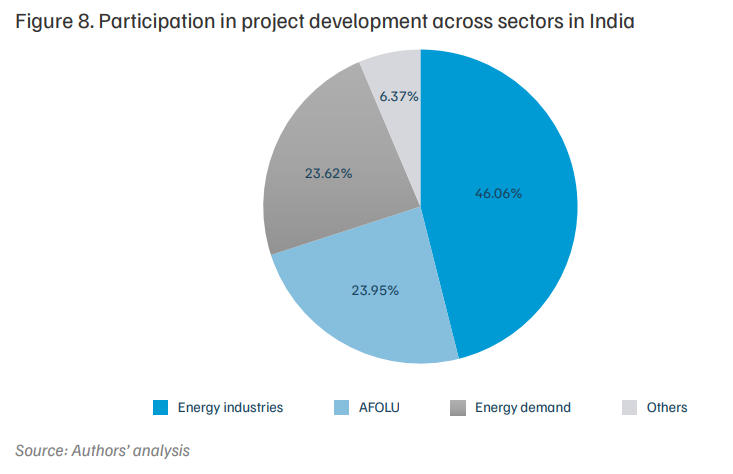

To assess sectoral representation in India’s voluntary carbon market, we analysed all projects listed in the Verra VCS Registry, including registered and unregistered projects. Through this approach, we aimed to evaluate the participation of Indian project developers across sectors. All 598 projects (including registered and non-registered projects) in the Indian data set (post-data validation) were used to assess participation across 16 sectors.

As reflected in the VCS Registry, India’s project portfolio shows significant disparities in sectoral representation. Most projects are concentrated in the energy demand, energy industries, and AFOLU sectors. Specifically, energy industries account for 46 per cent, energy demand for 23 per cent, and AFOLU for 24 per cent of the total portfolio. In contrast, there is zero participation in several sectors, including construction, mining and mineral production, metal production, fugitive emissions, solvent use, and carbon capture and storage (CCS). Furthermore, participation is limited in sectors such as energy distribution (0.17 per cent), manufacturing industries (1.17 per cent), and the chemical industry (0.5 per cent). Notably, sectors considered to have moderate to high mitigation potential—including transport, waste disposal, mineral/ mining production, CCS, livestock management, agriculture within AFOLU, and durable carbon dioxide removal—remain underutilised.

It is critical to ensure wide sectoral representation to harness India’s emission mitigation potential and attract funding to facilitate industry transitions. Our assessment, however, shows that a lot needs to be done to ensure adequate representation of projects across sectors. Figure 8 shows sectoral participation in India, indicating that the energy industries have the highest participation, followed by AFOLU and energy demand.

In this section, we highlight the key challenges across sectors based on our discussion with three expert stakeholders – a large-scale carbon project developer, a small-scale carbon project developer, and a certification body.

Systematic issues in AFOLU projects are leading to extended registration timelines in India. According to stakeholders, in many cases, projects being implemented on ground face barriers that , often deters investors, developers (especially new entrants) and local communities , leading to disinterest and distrust need among stakeholders. Projects remain in limbo without any guarantee of successful credit generation, and the brunt is faced by local communities and investors who have invested time, land, and money in project deployment. In this section, we discuss the various issues hindering projects in this sector.

Regulatory and legal hurdles

In India, the complexity of legal and regulatory frameworks causes significant delays to forest carbon projects in the AFOLU sector. Experts reported that forest carbon projects have stringent standards for precise control as well as clear demarcation of large land parcels. This ensures that the project is economically viable and effectively managed throughout the duration of the project. However, ambiguity in land titles and overlapping jurisdictions between various government levels – from local panchayats up to state forest departments – add delays in the initial phases of project development. The involvement of multiple legal frameworks, such as the Forest Conservation Act and the Land Acquisition Act, often places these regulations at odds with local land usage. Land use is traditionally governed by customary practices and statutory regulations, compounded by bureaucratic processes overseen by central bodies and various state-level authorities.

A study (Aggarwal 2020) highlights the challenges encountered when implementing afforestation projects in Himachal Pradesh, particularly due to land tenure matters. These projects face multiple challenges in clarifying land titles due to the involvement of local village councils as well as the state’s forest department. Resistance from local communities’ delays progress further, as the project intervention caused conflict with traditional land-use practices. In this case, a lack of adequate consultation led to land rights and resource access disputes. A policy paper from the Indian Institute of Management, Bangalore, studies land disputes and delays in decisionmaking related to property rights over agricultural lands in Maharashtra. It revealed that most of the disputes were over land ownership, such as non-clarity of title, doubtful transactions, administrative loopholes, and legal multiplicities (Mane 2013).

Other Asian countries—such as China, Bangladesh, Indonesia, and Thailand—have faced similar land-use and management issues. Many countries have developed, or are currently developing, policies to support greater efficiency in land use, land management, and rights-related issues. Many Indian states are also adopting state-level policies to decrease these hurdles. However, it is essential to note that land titles and legal frameworks around tenure are shaped by decades of political and social negotiation. Implementing forest carbon projects requires alignment with these established frameworks while simultaneously scaling and accelerating development across large parcels of land, which involves numerous stakeholders.

India’s AFOLU sector faces significant challenges due to declining foreign investor interest. This decline, as explained by experts, can be attributed to a combination of factors, including reduced demand for carbon credits generated by such projects in India, relatively low prices in the carbon market, and the perceived low permanence of Indian AFOLU projects as a result of the media backlash in the past two years. For example, a CSE study published an exposé on various malpractices, questioning the overall effectiveness of ongoing offset projects (Dev and Krishnamurthy 2023). The Guardian reported that the market value of carbon offset credits has fallen by 61 per cent, indicating significant volatility in global carbon markets. This was further attributed to a combination of factors, including oversupply, shifting policy priorities, and investor scepticism about the integrity and long-term viability of many offset projects (Greenfield 2024).

Experts have further pointed out that certification bodies may deliberately delay project registration to balance the supply and demand in the market. Delays may be used to manipulate market dynamics to maintain price stability, but disadvantage project developers who rely on timely credit sales for project viability. This practice can deter foreign investors seeking more predictable and reliable returns on investment, leading to a cautious or even negative investment outlook towards Indian AFOLU projects.

This vulnerability stems from several inherent challenges associated with managing land-based projects and involves complex interactions between environmental, social, and regulatory factors. The Indian AFOLU sector deals with multiple disaggregated local-level stakeholders such as small landholders, indigenous communities, local government bodies, and non-governmental organisations, each with distinct interests and levels of engagement. These long-term projects span large land parcels with many local-level stakeholders. This invites multiple uncertainties at different stages of project development and implementation. AFOLU projects might frequently intersect with spaces owned by local communities that depend on these lands for their livelihoods through agriculture, livestock grazing, and the collection of forest products (Aggarwal 2020). Experts pointed out that these overlapping interests can lead to conflicts over land rights and resource access, as social acceptance is considered a critical factor for project viability, especially over a long period. Projects that fail to engage local communities or secure their consent and cooperation adequately are more likely to face challenges during the verification process, leading to possible suspensions or rejections.

Vulnerability to natural hazards

AFOLU projects, particularly afforestation/reforestation and soil carbon sequestration projects, are more exposed to natural hazards, with significant risks stemming from prolonged naturebased carbon removals. The successful issuance of credits in these projects depends on the stability of ecosystems, which makes them highly susceptible to adverse climatic events such as floods, droughts, and cyclones. The biggest challenges for AFOLU projects are the appropriate handling of natural risks, such as fire, pests, hurricanes, and climate change; internal management risks, such as those surrounding project management and financial viability; and external risks related to community engagement and land tenure (Verra).

Coupled with this, India’s vulnerability to climate hazards is a menacing factor in the minds of many investors. A CEEW study showed that 27 of 35 Indian states and union territories are highly vulnerable to extreme hydro-meteorological disasters such as floods, droughts, and cyclones (Mohanty and Wadhawan, 2021). Thus, there is a general belief among developers, investors, and buyers that the risks associated with this sector are increasing due to the worsening effects of climate variability. Experts noted that this major factor causes AFOLU sector projects to be suspended and rejected more often than those in other sectors. It also deters investors who are increasingly cautious about committing to long-term projects, as they are susceptible to significant non-permanence and implementation hurdles.

India’s renewable energy sector experienced rapid growth in the early 2010s as policy support, competitive auctions, and large-scale investments accelerated capacity additions (Dyck, Melaina et al. 2023). However, while the cost of renewable power has plummeted in recent years, few registrations of traditional renewable energy projects have been observed. This is partly due to market saturation and a shift in focus to newer technologies and innovative project formats—such as hybrid or distributed solutions—that promise grid stability and better economics. Thus, historical success was driven by supportive policies and competitive pricing and now it has been tempered by market saturation and evolving investor preferences. These factors, along with administrative challenges and changing policy frameworks, contribute to the slow pace of registering conventional renewable projects today.

Financial additionality

Large-scale, non-grid-connected renewable energy projects frequently encounter challenges in demonstrating financial additionality, particularly in nations outside the group, that is, where these projects are already economically viable and competitive with fossil-fuel alternatives. Since 2010, over 750 million voluntary carbon credits have been issued by 1,700 renewable energy projects worldwide, accounting for about 30 per cent of all carbon credits generated in the VCM,these credits however, contributed to less than 4 per cent of total revenue for large-scale wind, hydro, and solar installations (Loffler et al., 2024).

Furthermore, geographic context is essential in addressing additionality concerns, particularly in emerging economies such as India, where high renewable energy adoption makes it harder to prove that new projects provide emission reductions beyond business as usual. A 2021 study on India’s wind power sector found that many projects were financially viable without carbon credits. This resulted in only infra-marginal projects taking off, which weakened the overall impact on global emissions (Calel et al. 2024).

Market saturation

This sector is increasingly seen as highly saturated within VCMs. Large volumes of credits are generated at low costs and fetch very low prices. Recently, Verra and Gold Standard restricted the certification of new renewable energy projects only to, underserved regions, and small island developing states (SIDS) to focus carbon financing on areas facing considerable barriers in adopting renewable energy (Verra 2024). This has led to many projects being halted in the validation phase, as registries revisit and scrutinise the genuine impact of these projects beyond what would occur in a businessas-usual scenario.

Shift in focus to other types of certifications

Most standards in VCMs have stringent additionality requirements. Many large-scale market players in the energy industries sector, which do not need to be supported by carbon revenue, are shifting their focus to other energy certifications, such as international renewable energy certificates (I-RECs) or renewable energy certificates (RECs). These certificates often do not require a demonstration of additionality, making them a better alternative for already economically viable projects.

Many sectors in India have high- to medium-level potential for decarbonisation, and these sectors can leverage the VCM to seize these opportunities and scale financing. India’s greatest decarbonisation potential lies in the power; industrial, particularly steel and cement; and agriculture sectors. The power sector can reduce emissions significantly by rapidly expanding renewable energy capacity and upgrading the efficiency of fossil fuel plants. Industrial sectors, such as steel and cement, can leverage process innovations, green hydrogen adoption, and carbon capture, utilisation, and storage (CCUS) to cut emissions substantially. Meanwhile, being a high-emission sector, agriculture offers numerous opportunities through sustainable farming practices, A/R, and improved land management, all of which can increase carbon sequestration (Duhan 2022). However, around 90 per cent of offset projects in the ICM portfolio are traditional energy and A/R projects in the AFOLU sector. Multiple factors enhance the attractiveness of these sectors to investors and project developers. These factors, if made available for other high-medium potential sectors, can help build a stronger and more diversified decarbonisation portfolio in India’s VCM.

Availability of methodologies

Interviewed stakeholders note that the availability of approved methodologies within each sector influences sectoral participation. Sectors with more approved methodologies offer more options for project developers, encouraging participation in diverse sectors for mitigation activities. Increased engagement also signals investors to invest in particular industries that are cost-effective, can fetch higher prices, have moderate to high mitigation potential, and have minimal risks. Conversely, sectors with fewer approved methodologies may face barriers to entry, limiting the number of projects and participants.

To understand this better, we looked at the methodology portfolio to identify one of the directly linked factors that might influence sectoral participation: the availability of diverse methodologies under each sector or subsector. As validated by the stakeholders engaged in our study, sectors such as AFOLU, energy industries, and energy demand appear to have higher participation and more available methodologies. However, despite the availability of methodologies, the waste-handling sector and transport sector have not been utilised by developers as abundantly as the other three. Stakeholders report that these sectors face additional challenges in setting baselines and accounting for emission reductions due to the presence of complex value chains in waste-handling and transport sectors , which may influence low uptake. Table 4 compares the sectors with the highest availability of methodologies and their activity in the VCM side-by-side.

Table 4. Side-by-side comparison of (a) the availability of methodologies under each sector and (b) participation in each sector

| Sectors | (a) Availability of methodologies | (b) Participation |

|---|---|---|

| Energy industries | High | High |

| AFOLU | High | High |

| Energy demand | Medium | High |

| Waste handling and disposal | High | Low |

| Transport | Medium | Low |

| Manufacturing industries | Medium | Low |

| Fugitive emissions | Low | Low |

| Construction | Low | Low |

| Chemical industries | Low | Low |

| Energy distribution | Low | Low |

| Mining and metal industries | Low | Low |

| Carbon capture and storage | Low | Low |

Source: Authors' analysis from the sectoral representation in Figure 8 and Table 2.

Domestic policies

The current Indian Carbon Market has a significant focus on energy sector and AFOLU sector projects. This is due to it’s alignment with the country’s climate goals as outlines in it’s NDC. These targets include reducing GDP emissions intensity by 33–35 per cent by 2030 from 2005 levels, increasing non-fossil-fuel capacity to about 40 per cent of the total power capacity by 2030, and creating an additional carbon sink of 2.5–3 billion tonnes of CO2 equivalent through expanded forest and tree cover (MNRE 2024).

Complementing these measures, the implementation of proactive initiatives such as the National Green Hydrogen Mission, Pradhan Mantri Kisan Urja Suraksha evam Utthaan Mahabhiyan (PMKUSUM), PM Surya Ghar, and the Production-Linked Incentive (PLI) schemes for solar PV modules highlight the Indian government’s strategic focus on enhancing energy generation capacity while reducing dependence on fossil fuels. This corroborates with the Government of India setting up the ambitious target of achieving 500 GW from non-fossil sources by 2030 (MNRE 2024). In addition, wind energy programmes are being encouraged through capital subsidies, and the National Clean Energy Fund—funded by a coal tax—provides financial support for clean technology projects.

India’s supportive policies for greening initiatives – such as the National Afforestation Programme (NAP), Green India Mission (GIM), compensatory afforestation under the Compensatory Afforestation Fund Management and Planning Authority (CAMPA), the National Agroforestry Policy, and the Green Credit Programme – have given impetus to afforestation, reforestation, and sustainable agriculture activities. These measures collectively promote several projects in these sectors by signalling their growth.

Technological advancements in clean energy and energy efficiency

In India, renewable energy technologies such as solar and wind have now matured. Their scaling has resulted in cost reductions and efficiency improvements, making them viable for large-scale deployment. Innovations and developments such as integrating solar photovoltaic materials and efficient wind turbine designs – such as bifacial solar panels and larger rotor diameters – have massively improved energy capture and operational efficiency (Rodrigues et al. 2023). Infrastructure development, particularly in grid integration and advanced energy storage solutions such as lithium-ion batteries, supports integrating intermittent renewable sources into the energy system. Furthermore, India’s manufacturing capabilities have become more enhanced, which has reduced costs and strengthened local supply chains, aided by government policies such as incentives for local production and feedin tariffs. This has lowered the entry barrier and operational risks, making renewable energy technologies attractive and viable options for investors. However, some of these aspects have also led to difficulties in demonstrating the financial additionality of the projects.

Foreign and Indian investments in clean energy

India’s renewable energy sector has experienced substantial growth, with foreign direct investment (FDI) reaching USD 2.5 billion in FY 2023—marking a 56 per cent year-on-year increase. Total FDI in the sector surpassed USD 12.47 billion by December 2022(Ranjan, 2023). Key investors from countries such as Singapore, Mauritius, and Japan have fuelled this growth (Cyrill, 2024). The country’s renewable energy landscape, driven by affordable capital and regulatory incentives, has attracted global strategic investors targeting netzero goals (Duhan, 2022). As a result, the influx of FDI has accelerated India’s clean energy transition, contributing to substantial scaling of the renewable energy market and increased interest in developing clean energy projects in the India’s VCM portfolio.

Our study recommends establishing a robust monitoring and reporting framework that submits systematic and regular assessment reports to the National Steering Committee for Indian Carbon Market (NSCICM) on various aspects related to the functioning of the CCTS offset mechanism. This framework will not only keep the governance body well-informed regarding the functioning of the mechanism, but it will also enable the timely redressal of systemic and process-related challenges and irregularities. We recommend the following key aspects to be considered for inclusion within the monitoring and reporting assessment report to be submitted quarterly to the NSCICM.

Establish and review the performance of a single-window clearance system for AFOLU projects

Our assessment highlights that projects in the AFOLU sector face the most delays due to the myriad challenges associated with this sector. Other countries in the ROA that face similar issues have modernised their land administration systems to address challenges such as overlapping jurisdictions, ambiguous land titles, and bureaucratic delays. For example, Vietnam’s National Land Information System issues authenticated digital e-certificates for land registration, reducing processing times and enhancing transparency (ASL Law Firm 2018). Similarly, Thailand’s efficient land administration – managed by the Department of Lands under the Ministry of Interior – completes most titling and registration procedures in less than a day at minimal cost. It is supported by legislative frameworks such as the 1954 Land Code and subsequent reforms (Open Development Thailand 2016). Bangladesh and Indonesia promote digitisation by establishing e-service centres and adopting digital governance frameworks to preserve records and streamline service delivery. However, data consistency and inter-agency coordination issues remain (Akter, 2022).

Thus, we recommend a single-window clearance system for AFOLU projects on the CCTS offset mechanism website, which can help address key challenges such as land disputes, regulatory hurdles, and land title identification. Drawing from models such as the National Single Window System (NSWS), and utilising the growing database under the Digital India Land Records Modernization Programme (DILRMP), this system would streamline approvals for land titles, environmental clearances, and regulatory compliances through the use of a centralised digital platform. Key features would include automated land title verification, time-bound application processing, and coordination among central departments such as the Ministry of Environment, Forest and Climate Change (MoEFCC) and state revenue bodies. This would enable regulatory issues and environmental or social disputes related to a particular land parcel to be detected early on in the planning stage, presenting developers with options to carefully rectify, reassess, and select land parcels.

The NSCICM should be quarterly apprised of the progress in establishing such a single-window clearance system for AFOLU projects, as well as its performance once it is operational.

Monitor the status and progress of project portfolio diversification

Our assessment reveals the disproportionate participation of the energy demand and energy industries sectors in the mechanism. While these two sectors hold significant potential, India has the scope to diversify the carbon offset market to other high-potential and emerging sectors as well. For example, the transport sector, which is responsible for nearly 14 per cent of India’s emissions, can attract significant climate financing by adopting electrification and fuel-efficient logistics, tapping into global funds to reduce transport emissions (Climate Action Tracker 2024). The waste management sector, which accounts for 3–4 per cent of national emissions (Cheteau, Dang, and MacDonald 2023), holds significant potential for waste-to-energy projects and landfill gas capture, which can draw carbon revenues and enhance environmental, social, and governance (ESG) investment.

In agriculture (within the AFOLU sector), sustainable practices can sequester 85.5 Mt CO2 annually (Sapkota et al., 2019) while enhancing rural incomes and engaging a large section of the economy. India’s CCS potential is sizeable and has the potential to mitigate up to 50 million tonnes of CO2 annually from large sources near oil and gas fields, with an additional 100 million tonnes near coal fields (Beck et al., 2013). To encourage participation in diverse sectors, the CCTS mechanism may consider:

A quarterly report on the pool and diversity of projects registered over time should be submitted for assessment to NSCICM.

Monitor the real-time status and progress of project applications through a project tracking system

Based on our analysis, it is essential to incorporate real-time tracking for each stage of the registration cycle, such as project submission, validation, verification, stakeholder consultations, and certification issuance. These thresholds should align with historical timelines and best practices from frameworks such as the CDM, Verra VCS, and Gold Standard. A centralised database should include phase-wise timelines, detect delays, and notify stakeholders via automated alerts. In case of delays, a grace period may be provided, followed by the submission of a mandatory issue report by the particular ACVA outlining the reasons, mitigation measures, and revised timelines. This approach would ensure early identification and resolution of issues in the project development and credit issuance cycle.

This database can also be a repository for project-related data accessible to authorised users. Such data would be useful for research, transparency, adaptive management practices, and content creation for capacity-building programmes. It can be integrated with an automated quarterly report submitted to the NSCICM that summarises the status of project applications, any delays, and the actions being taken to address these delays.

Institute annual performance review of accredited carbon validation and verification bodies (ACVAs/VVBs)

An annual performance review system for accredited carbon validation and verification bodies (ACVAs) should be established to enhance accountability and maintain high operational standards. As independent third parties, these organisations are essential for upholding the market’s integrity and ensuring the successful issuance of carbon credits. Since they are deeply involved in validating and verifying projects, their role is crucial. A performance review system should assign performance-based grades to all certified ACVAs, enabling project developers to make informed decisions based on cost-effectiveness and performance metrics.

The following key points may be included within the performance review system:

The NSCICM should be briefed about the key results and actions should be taken based on the suggested annual performance review of ACVAs.

Share status and progress updates of capacity-building activities undertaken by project developers with stakeholders

Our consultation with experts revealed that many offset-based projects, especially in the AFOLU sector, become delayed when the stakeholders within the project ecosystem are not well informed. Therefore, to ensure the efficient functioning of the mechanism, there is a need to deliver timely and regular capacity-building activities. The developers should undertake such activities at the project’s onset as well as at the time of listing. They should then record and report on these activities for each project. Information related to capacity-building activities should be reported quarterly to the NSCICM.

Share status and progress updates related to ‘highadditionality’ energy projects

Our assessment shows that many projects in the energy sector are on hold for a long time, as demonstrating additionality is challenging, given that renewable energy costs have fallen significantly in the last few years. To address this, new standards within the CCTS offset mechanism should prioritise high-additionality projects that can demonstrate financial and environmental benefits, such as energy storage systems (ESS), CCUS, and durable carbon removal–based projects. Developers should conduct robust barrier analyses to establish financial additionality, ensuring carbon financing is directed toward projects that would not be viable without such support.

Gradually, reliance on traditional renewable energy projects within the ICM should be reduced as they become increasingly cost competitive and do not need additional carbon revenue to be supported. Other projects that may be considered high additionality now might also become cost competitive in the future with the scaling of such industries. The NSCICM should be briefed quarterly about the progress of such high-additionality energy projects.

Integrate standardised baselines to streamline project development within the CCTS offset mechanism

The CCTS offset mechanism should consider integrating standardised baselines (SBs) to streamline the carbon credit issuance process and overcome barriers to project development. A use case has been demonstrated in the development of the rice mill sector in Cambodia under CDM, for which SBs were successfully applied to address challenges such as small project sizes, long project cycles, and high transaction costs (UNDP 2013). Similarly, in India, projects by small-scale developers, or projects with limited data availability—especially in the energy sectors—could benefit from employing SBs, as they provide an agreed-upon baseline emissions factor, thereby simplifying the baseline identification and additionality demonstration process. Adopting SBs would further reduce the complexity of monitoring as well as calculation requirements for individual projects, thus significantly reducing transaction costs and delays within the credit issuance cycle and streamlining project development and implementation processes.

Based on the historical experiences of private-sector VCMs, our assessment reveals some of the challenges and opportunities relevant to the offset mechanism under the CCTS . Based on our analysis on three major sectors, we highlight that the AFOLU sector in India currently encounters multiple challenges – including complex regulatory frameworks related to land ownership, land use conflicts, and susceptibility to natural hazards – which result in prolonged project timelines and high vulnerability for projects. Similarly, the energy industries sector grapples with issues of financial additionality, large credit volumes, and market saturation, leading to significant delays. The energy demand sector, while less affected, still faces notable bottlenecks in the early project stages. Moreover, we learned that India’s overall carbon market portfolio is heavily concentrated in a few sectors, with limited representation in high-potential areas such as transport, waste management, agriculture, and CCS, leaving significant mitigation opportunities untapped.

Tracking the advent of these issues and managing them in the early stages can help regulate an otherwise unregulated market and strengthen the market framework for the CCTS mechanism. This will act as a differentiating factor for the CCTS offset mechanism standard and drive demand for offsets certified under it. The most compelling insight emerges not from raw data but from an understanding of how complex this market is and the need for adaptive frameworks and regulatory nudges. These tools can be used to navigate various externalities and consequently utilise market opportunities and deliver on the promise of scaling emissions mitigation and climate financing.

To address these challenges, we recommend implementing an institutionalised monitoring and reporting structure to regularly brief the NSCICM and benefit from its guidance on the various challenges that the ICM faces. Specifically, we recommend that the NSCICM be quarterly briefed about the establishment and performance of a single-window clearance system for AFOLU sector projects, the status and progress of project portfolio diversification, the real-time status and progress of project applications through a project tracking system, the performance of ACVAs/VVBs through an annual performance review system, capacity-building activities undertaken by project developers with stakeholders, and the status and progress of high-additionality energy projects.

We believe that if the key recommendations of our study are implemented, India’s CCTS can differentiate itself from existing private-market standards and become a robust, transparent mechanism by embracing flexibility, promoting sectoral diversity, and maintaining stringent integrity standards. India stands at a critical juncture for climate action, where its rich experience in VCMs should be able to propel its journey.

Aggarwal, Ashish. 2020. “Improving Forest Governance or Messing It up? Analyzing Impact of Forest Carbon Projects on Existing Governance Mechanisms with Evidence from India.” Forest Policy and Economics 111 (February): 102080. doi:10.1016/j.forpol.2019.102080.

Ahonen, Hanna-Mari, Juliana Kessler, Axel Michaelowa, Aglaja Espelage, and Stephan Hoch. 2022. “Governance of Fragmented Compliance and Voluntary Carbon Markets Under the Paris Agreement | Article | Politics and Governance,” March.

Akter, Marufa. 2022. “Digitalization in the Land Service Delivery: Comparison between Bangladesh and Indonesia.” Southeast Asia: A Multidisciplinary Journal 22 (1): 79–91. doi:10.1108/ SEAMJ-01-2022-B1006.

“Area of Focus - Agriculture, Forestry, and Other Land Use (AFOLU).” n.d. Verra. https://verra.org/programs/verifiedcarbon-standard/area-of-focus-agricul....

ASL Law. 2018. “Introduction of Electronic Land Registration in Vietnam: Key Changes Under Decree 101.”

Beck, Richard A., Yolanda M. Price, S. Julio Friedmann, Lynn Wilder, and Lee Neher. 2013. “Mapping Highly Cost-Effective Carbon Capture and Storage Opportunities in India.” Journal of Environmental Protection 04 (10): 1088–98. doi:10.4236/ jep.2013.410125.

BEE. 2024. “Carbon Market.”

Betz, Regina, Axel Michaelowa, Paula Castro, Raphaela Kotsch, Michael Mehling, Katharina Michaelowa, and Andrea Baranzini. 2022. The Carbon Market Challenge: Preventing Abuse Through Effective Governance. 1st ed. Cambridge University Press. doi:10.1017/9781009216500.

Broekhoff, Derik, Michael Gillenwater, Tani Colbert-Sangree, and Patrick Cage. 2025. “A Guide to Using Carbon Credits.”

Burtraw, Dallas, Karen L. Palmer, Clayton Munnings, Paige Weber, and Matt Woerman. 2013. “Linking by Degrees: Incremental Alignment of Cap-and-Trade Markets.” SSRN Electronic Journal. doi:10.2139/ssrn.2249955.

Calel, Raphael, Jonathan Colmer, Antoine Dechezleprêtre, and Matthieu Glachant. 2024. “Do Carbon Offsets Offset Carbon?” American Economic Journal: Applied Economics. Accessed November 22. doi:10.1257/app.20230052.

“Carbon Offset Guide.” 2024. Carbon Offset Guide. Accessed December 10. https://offsetguide.org/.

“CDM Methodologies - Sectoral Scope Linkage.” n.d. UNFCCC CDM. https://cdm.unfccc.int/methodologies/methodologiesAccrv6/index.html.

Cheteau, John, Geetika Dang, and Margaux MacDonald. 2023. “A Framework for Climate Change Mitigation in India.” IMF Working Paper.

Cyrill. 2024. “The Scope for Foreign Investment in India’s Green Growth Challenge.” https://www.india-briefing.com/news/

“Decarbonisation and Various Opportunities in Potential Sectors...” 2024. Accessed November 22. https://www.investindia.gov.in/team-india-blogs/decarbonisation-andvario....

“Decarbonising the Indian Transport Sector: Pathways and Policies.” 2024. Accessed November 22.

Dyck, Melaina, Charlotte Streck, Streck, and Danick Trouwloon. 2023. “The Voluntary Carbon Market Explained.”

Gaurav Sishodia, Deepanshu Kaul, Keshav Daga, Namita Vikas, Smitha Hari, Suranjali Tandon, Aarti Bansal, et al. 2024. “Carbon Markets as a Tool for Climate Financing: The India Story,”

Gupta, Rajat, Shirish Sankhe, Naveen Unni, and Divy Malik. 2022. “Decarbonising India: Charting a Pathway for Sustainable Growth.” Mckinsey Sustainability.

Kärt Johanna Ojamäe. 2024. “A (Little) History of the Voluntary Carbon Market.” March. https://www.arbonics.com/knowledgehub/a-little-history-of-the-voluntary-....

Loffler, Guy Turner, Jamie Saunders, and Lucien Georgeson. 2024. “Renewable-Energy Carbon Credits Losing Steam.”

Michaelowa, Axel, Shishlov, Igor, Hoch, Stephan, Bofill, Patricio, and Espelage, Aglaja. 2019. “Overview and Comparison of Existing Carbon Crediting Schemes.”

Mohanty, Abhinash, and Shreya Wadhawan. 2021. “What Is India’s Climate Change Vulnerability Index (CVI) ? CEEW.”

“New ICVCM Methodology Decisions Announced.” 2024. Verra.Org. June 8.

Open Developlemt Thailand. 2016. “Land.” https://thailand.opendevelopmentmekong.net/topics/land/.

Patrick Greenfield. 2024. “Market Value of Carbon Offsets Drops 61%, Report Finds.” The Guardian, May.

PIB. 2023. “Activities Finalised to Be Considered for the Trading of Carbon Credits under Article 6.2 Mechanism to Facilitate the Transfer of Emerging Technologies and Mobilise International Finance in India.” Https://Pib.Gov.in/PressReleaseIframePage.Aspx?PRID=1900216. https://pib.gov.in/PressReleaseIframePage.aspx?PRID=1900216.

“Press Release:Press Information Bureau.” 2024. Accessed November 22.

Rajaram R and Mane. 2013. “Study of Causes of Land Disputes and Delays in Decisions over Property Rights in Agricultural Lands in Maharashtra.” CPP_PGPPM_P13_18. Banglore: Indian Institute of Management Bangalore. https://repository.iimb.ac.in/handle/123456789/9552.

Ranjan. 2023. “Foreign-Direct-Investment-Indias-RenewableDips-Fy-2023.”

Rodrigues, Neshwin, AK Saxena, Shubham Thakare, and Raghav Pachouri. 2023. “India’s Electricity Transition Pathways to 2050.” TERI.

Santosh Kumar and Sarla Meena. 2024. “Press Release| India’s Renewable Energy Capacity Hits 200 GW Milestone.” Saurabh Kalia.

Sapkota, Tek B., Sylvia H. Vetter, M.L. Jat, Smita Sirohi, Paresh B. Shirsath, Rajbir Singh, Hanuman S. Jat, Pete Smith, Jon Hillier, and Clare M. Stirling. 2019. “Cost-Effective Opportunities for Climate Change Mitigation in Indian Agriculture.” Science of The Total Environment 655 (March): 1342–54. doi:10.1016/j. scitotenv.2018.11.225.

Sonia Duhan. 2022. “Decarbonisation and Various Opportunities in Potential Sectors in India.”

The Economic Times. 2010. “Indian Carbon Credits to Triple by 2012,” December 5. https://economictimes.indiatimes.com/news/economy/indicators/indian-carb....

Trishant Dev and Rohini Krishnamurthy. 2023. “The Voluntary Carbon Market in India: Do People and Climate Benefit?” Centre for Science and Environment.

UNDP. 2013. “UNDP-Guidance_Note_SBs.” UNDP.

“UNFCCC Clean Development Mechanism Methodology - Gold Standard Eligibility for Large-Scale CDM Meths (AM & ACM).” 2021.

“VCS PROGRAM Methodologies.” n.d. Verra.Org. https://verra.org/program-methodology/vcs-program-standard/overview/.

“VERIFIED CARBON STANDARD.” n.d. https://verra.org/programs/verified-carbon-standard/.

Verra. n.d. Company Website. Who We Are.

“Verra VCS Registry.” n.d. https://registry.verra.org/app/search/VCS.

World Bank. 2024. High Integrity, High Impact: The World Bank Engagement Roadmap for Carbon Markets. Washington, DC: World Bank. doi:10.1596/42016.

Voluntary carbon markets (VCMs) are decentralised carbon markets where private actors like companies or individuals voluntarily buy or sell carbon credits to meet self‑set climate goals, and participation is not legally required. By contrast, compliance markets such as India's new Carbon Credit Trading Scheme (CCTS) compliance mechanism or EU-ETS operate under government regulation; covered entities must meet legally binding targets linked to the nation's goal to decarbonise industries and support its net-zero journey. Thus, VCMs channel discretionary climate finance, while compliance markets enforce mitigation through mandates by providing a cost-efficient way to decarbonise hard-to-abate industries.

There are multiple factors, but in brief, these include (i) sectoral complexity and changing sectoral realities, (ii) Validation Verification body capacity and performance, (iii) Availability of standardised baselines; (iv) the efficiency of state‑level approvals and inter‑agency coordination; and (v) developers' access to finance for upfront MRV work (vi) Certification body's institutional capacity to enforce timelines (vii) level of support from local communities. A mix of any of these factors may influence project timelines, and early-stage detection of bottlenecks can help make project timelines more efficient.

A real‑time project tracking dashboard of phase-wise project progress highlights bottlenecks early, lets developers and validators triage capacity, reassures buyers about credit integrity, and builds market confidence through transparency. Continuous tracking also helps investors and buyers understand sectoral realities and adjust their strategies to minimise the risk of systemic backlogs.

How can Carbon Markets Scale Durable Carbon Dioxide Removal in India?

Sustainable rice cultivation in India

EU Carbon Border Adjustment Mechanism

Roadmap for a Net-Zero Power Sector in Gujarat