Council on Energy, Environment and Water Integrated | International | Independent

Suggested citation: Kumar, Sunil, Vibhuti Chandhok and Rishabh Jain. 2025. Making India a Hub for Critical Minerals Processing. New Delhi: Council on Energy, Environment and Water.

Critical minerals are now central to India's industrial growth, energy, and national security. To develop a self-reliant supply chain of critical minerals will require strengthening India's processing ecosystem - not just as an industrial requirement but as a strategic imperative - essential for reducing import dependence and ensuring energy security.

This report offers a comprehensive assessment of India's present capacity in processing critical minerals. It focuses on 15 critical minerals - including lithium, cobalt, nickel, rare earths, and graphite - selected from the 30 identified by the Ministry of Mines in June 2023. The study maps natural occurrences of critical minerals, analyses commercial processing routes worldwide, and evaluates India's midstream (processing and refining) capabilities. In doing so, it identifies the main roadblocks, proposes practical solutions, and suggests clear strategic interventions built on three pillars: building institutional capacity, strengthening the existing mining and metallurgy ecosystem, and enhancing competitiveness.

Countries across the globe are facing the impacts of climate change, and to reduce its effects, the transition to clean energy technologies, such as batteries, solar photovoltaics, wind energy, etc., has become necessary. Critical minerals are essential for India’s energy transition and are commonly defined as ‘minerals that are necessary inputs for national economic goals and have serious risks that threaten the supply chain’s resilience’ (NBR 2022). Additionally, critical minerals are building blocks for many strategic sectors, including defence, aerospace, and electronics, thus underscoring their multidimensional economic and technological importance. India already possesses a foundational infrastructure and institutional memory for the mining and processing of bulk minerals such as iron, aluminium, lead, zinc, etc., which can be further strengthened and strategically developed to support the growing needs of critical minerals processing.

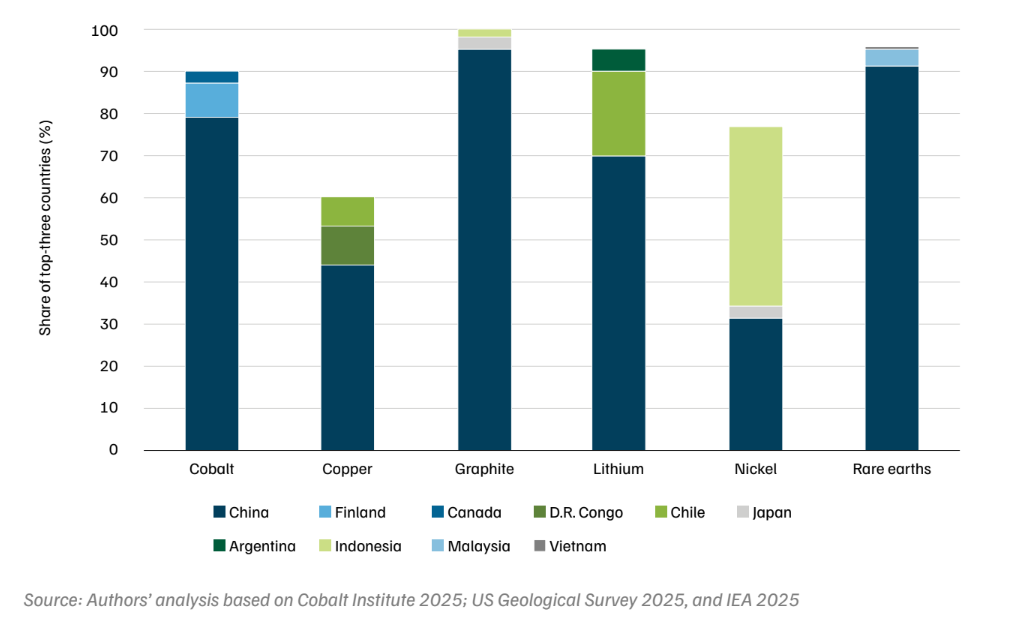

Critical minerals are found only in a handful of countries with limited availability, and the supply chain of these minerals is also highly concentrated in a few countries. China, for example, dominates in processing critical minerals like lithium, cobalt, graphite, rare earth elements and copper, as shown in Figure ES1. China is responsible for more than 90 per cent of global rare earth processing, 95 per cent of graphite processing, and 79 per cent of refined cobalt production. India is not among the top three producing countries for many of these critical minerals relevant for clean energy transition technologies and the defence sector. It remains dependent on imports for nearly all of its lithium, cobalt, and nickel requirements1 (Ministry of Mines 2023). Moreover, the global landscape is moving towards a more calculated, security-driven approach to resource management, which makes India’s existing supply chain vulnerable to significant geopolitical and economic risks, such as trade barriers, as well as recent restrictions on the supply of minerals such as rare earths (CSIS 2025).

Figure ES1. Share of the top three countries in the processing of critical minerals (2024)

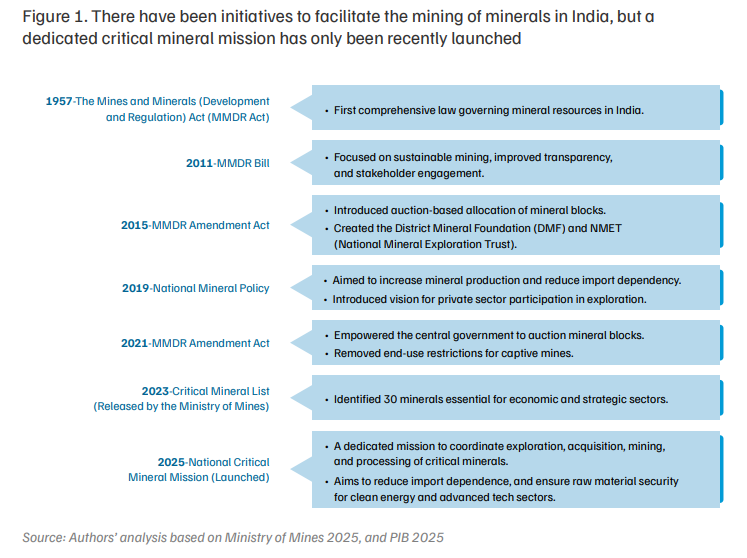

India’s ambitious trajectory to achieving Net-Zero by 2070 entails energy independence and carbon neutrality that hinge critically on large-scale deployment of clean energy technologies like solar, wind and batteries. Recognising the strategic importance of critical minerals, policy decisions governing them have gained substantial momentum since India’s G20 presidency in 2023. After successful negotiations on critical minerals during the G20 Energy Transition Working Group, the Ministry of Mines amended the Mines and Minerals (Development and Regulation) Act (MMDR) to ease the process of critical mineral block auctions, followed by the launch of the National Critical Mineral Mission in January 2025, with a budget of INR 34,300 crore (approximately USD 4 billion) over seven years from FY 2024–25 to 2030–31. One of the important action points of the recently launched National Critical Mineral Mission is the development of four processing parks where existing capabilities should be leveraged. The government has allocated a budget of INR 500 crore (approximately USD 58 million) for the same. The mission aims to secure a long-term, sustainable supply of critical minerals and strengthen India's critical minerals value chains, encompassing all stages from critical mineral exploration, mining, beneficiation and processing, and recovery from end-of-life products.

While India remains dependent on imports for several critical minerals such as lithium, nickel, cobalt, etc., this evolving policy landscape and auction of critical mineral blocks present a timely opportunity to focus on the development of domestic processing capabilities. India already has the opportunity to emerge as a key player in the processing of critical minerals given that it has a well-developed mining industry and significant technological know-how in mineral processing, owing to its expertise in base metals, including iron, aluminium, copper, and zinc, thus providing a strong base in mineral processing. The existing capabilities provide a strong foundation to expand into the processing of critical minerals, and with these advantages, India holds significant potential to become a global player in the processing of critical minerals. To achieve this, it is essential to assess the current capabilities and gaps in India’s mineral processing landscape.

This report aims to provide an in-depth analysis of India's capabilities in the processing of critical minerals, and proposes potential strategic action steps to strengthen and develop domestic capabilities. To this end, we have covered the following aspects:

We expect the report’s findings to help the government and industry stakeholders in informed decision-making to develop India’s critical minerals processing capabilities.

Naturally critical minerals rarely occur in pure form; they are found in association with other valuable or non-valuable minerals/rocks in deposits. These naturally occurring minerals require processing after mining. The processing of any mineral includes a combination of physical and chemical operations to extract a high-purity element or compound, suitable for industrial applications. The naturally occurring deposits/ore and their commercial processing route of all the 15 minerals analysed in this report are shown in Table ES1.

Table ES1. Commercial processing routes of the critical minerals based on their naturally occurring ores and deposits

| S No | Critical mineral | Ore/Deposit type | Processing route |

|---|---|---|---|

| 1 | Cobalt | Copper-cobalt sulphide and oxide deposit | Roasting → Leaching → Solvent extraction → Precipitation |

| Nickel-cobalt laterite deposits | Leaching → Precipitation → Solvent extraction → Electrowinning | ||

| Nickel-copper-cobalt sulphide deposits | Smelting → Leaching → Solvent extraction → Electrowinning | ||

| 2 | Copper | Copper sulphide deposits | Smelting → Converting → Refining |

| Copper carbonate and oxide deposits | Leaching → Solvent extraction → Electrowinning | ||

| 3 | Graphite | Natural graphite | Froth flotation → Leaching |

| Synthetic graphite | Devolatilisation → Tar distillation → Graphitisation | ||

| 4 | Lithium | Spodumene, pegmatite deposits – hard rock | Calcination → Leaching → Precipitation → Carbonation |

| Brine | Precipitation (impurity removal) → Solvent extraction → Electrolysis → Carbonation | ||

| 5 | Molybdenum | Molybdenite, copper sulphide deposits | Roasting → Aluminothermic reduction |

| 6 | Nickel | Pentlandite, nickel sulphide deposits | Smelting → Converting → Froth flotation → Refining |

| Limonite, nickel-cobalt laterite deposits | Leaching → Precipitation → Solvent extraction → Electrowinning | ||

| 7 | Niobium | Pyrochlore and columbite-tantalite deposits | Leaching → Solvent extraction → Calcination Aluminothermic reduction → Refining |

| 8 | Platinum Group Elements (PGE) | Copper sulphide deposits | Smelting → Converting → Pressure leaching → Solvent extraction |

| 9 | Rare Earth Elements (REE) | Monazite, placer deposits | Chemical treatment → Solvent extraction → Ion exchange → Metallothermic reduction → Zone melting |

| Carbonatite and ion-adsorption clays | Leaching → Solvent extraction → Hydrometallurgy | ||

| 10 | Silicon | Quartz, silica sand | Carbothermic reduction |

| 11 | Tin | Cassiterite, placer deposits | Smelting → Refining |

| 12 | Titanium | Ilmenite and rutile, placer deposits | Leaching → Hydrolysis → Purification → Calcination |

| 13 | Tungsten | Scheelite and wolframite, Skarn deposit | Leaching → Solvent extraction → Crystallisation Calcination |

| 14 | Vanadium | Vanadiferous titanomagnetite deposits | Roasting → Leaching → Solvent extraction → Calcination → Aluminothermic reduction |

| 15 | Zirconium | Zircon sand, placer deposits | Fusion with NaOH → Leaching → Solvent extraction → Calcination → Magnesiothermic reduction |

|

|

|||

| Source: Authors' analysis | |||

India has fundamental knowledge of processing bulk minerals because of its existing mining industry and decades of experience in processing some critical minerals. Copper concentrate, for example, is processed through the pyrometallurgical route of smelting and refining, yielding high-purity copper metal.

Seven out of 15 critical minerals can be processed in India at a commercial scale. The seven - copper, graphite, rare earth elements, silicon, tin, titanium and zirconium - are being processed using primary sources at a commercial scale in India, though natural resource deposits are available for all 15 critical minerals. Domestic natural resources of some critical minerals, such as tin and copper, are of low grade, making processing less economically competitive compared to those available for import.

Though basic processing capabilities exist, there is limited access to critical minerals of the required purity for use in clean technologies. India has limited processing capabilities for clean technology minerals such as graphite, titanium, rare earth elements and tin. The purity of these minerals required for clean technologies is not easily achievable. This represents an opportunity to develop more sophisticated extraction and refining technologies in India to produce pure elements or compounds suitable for targeted applications. This requires robust linkages between industries involved in the processing of critical minerals and component manufacturers in strategic sectors like clean energy, defence, and electronics. Government policies such as the Production-Linked Incentive (PLI) scheme aim to bridge this gap by incentivising local production, but cross-ministerial coordination is essential for these policies to be effective.

India is collaborating with other countries to reduce dependency on China. The government is actively collaborating with international partners such as Argentina, Australia, Japan, South Korea, and USA to enhance India’s capabilities and reduce dependency on China. Khanij Bidesh India Limited (KABIL), for example, acquired five lithium blocks in Argentina through an Exploration and Development Agreement with CAMYEN, a stateowned company in January 2024. China currently dominates the sector not just because of its processing capability but also because of its well-integrated downstream industries that consume highly pure critical minerals.

What are the current roadblocks in establishing a domestic mineral processing sector?

India has immense potential to build a robust critical minerals processing industry, considering the growing market for clean energy products such as solar PV, wind turbines, energy storage, and hydrogen electrolysers. However, to unlock its full capacity, it must address key gaps in technology, operations, and market dimensions.

These interlinked challenges must be addressed to develop a critical minerals processing ecosystem in India that supports clean energy transition, strengthens supply chains, and may position the country as an important force in this sector.

Forward-looking government initiatives have cultivated significant momentum and optimism in India’s critical mineral landscape. Our analysis indicates the need for additional measures to fully capture the existing opportunity to bring both jobs and growth in this sector. We have identified three strategic areas of priority for industry leaders and policymakers, represented in Table ES2.

Based on these strategic priorities, we provide eight recommendations designed to address the existing gaps highlighted in the report and enhance the scale, efficiency and competitiveness of India’s mineral processing industry.

Table ES2. Strategic priorities will enable the advancement of India’s mineral processing industry

| Building capacity | Strengthening existing ecosystem | Enhancing competitiveness |

|---|---|---|

|

|

|

| Source: Authors' analysis | ||

India stands at a crucial juncture in its journey to competitively develop a critical minerals processing industry. While several challenges exist, a well-coordinated strategy encompassing international collaboration, domestic capability building, and a forwardlooking whole-of-government approach with appropriate policy measures can unlock India’s full potential in this space. By addressing the structural and strategic challenges, India can reduce its dependence on imports, secure a sustainable supply chain of critical minerals, and enhance its industrial competitiveness.

Critical minerals are the bedrock of the technologies that shape our modern world, serving as indispensable resources for economic stability and national security in an increasingly digital and climate-focused era. These minerals are vital across crucial sectors such as renewable energy, defence, telecommunications and mobility—areas poised to drive the next wave of national growth. Each mineral holds a unique role in facilitating energy transition and supporting strategic industries. For instance, lithium, nickel, and cobalt are the backbone of lithium-ion batteries that power everything from smartphones to electric vehicles. Rare earth elements like neodymium, praseodymium, dysprosium, samarium and terbium enable high-strength magnets that are crucial for wind turbines. Silicon is fundamental to solar cell production and semiconductor manufacturing, which feeds into the telecommunications and electronics sectors. In defence, minerals such as titanium, tungsten, vanadium and rare earth elements are critical for cutting-edge weaponry and advanced aerospace systems.

To effect India’s commitments to cut emissions intensity by 45 per cent below 2005 levels by 2030 and achieve 50 per cent of its electric power from non-fossil fuel sources (PIB 2023a), clean energy technologies will be increasingly important. Critical minerals are the raw materials required for these technologies. Thus, India’s ambitions to become a self-reliant, technologically advanced nation require a secure, sustainable, and resilient supply of critical minerals. They are key to driving economic growth and leading India towards an era of innovation and energy independence.

Critical minerals are the foundation of the modern economy, yet their supply chain is highly concentrated (CEEW, IEA, UC-DAVIS and WRI 2023). China, for instance, led in the mine production of key critical minerals in 2024, including natural graphite (79 per cent), rare earth elements (69 per cent), tungsten (83 per cent) and vanadium (70 per cent). In the same year, Indonesia led in nickel mine production, accounting for a 59 per cent share, while Australia accounted for a 37 per cent share of global lithium mine production (US Geological Survey 2025).

The processing and refining of critical minerals globally are even more concentrated, amplifying global dependence on one country—China. In 2024, the nation accounted for 79 per cent of refined cobalt and 44 per cent of refined copper. China also accounted for the processing of 91 per cent of global rare earth elements, and 70 per cent of refined lithium production in the same year (Cobalt Institute 2025; US Geological Survey 2025; IEA 2025).

Nations around the world are prioritising the domestic supply security of these minerals to reduce reliance on imports, taking strong policy actions, as mentioned in Table 1 below. These strategies reflect a growing trend toward resource protectionism, where nations aim to secure critical minerals and capture more value by integrating deeper into global supply chains. We have analysed approximately 180 policies across 20 countries and found that 23 of them focus on initiating action for the processing of critical minerals. Among these, the United States, Australia, Indonesia, and Canada are leading with targeted support for domestic processing.

Table 1. Countries across the globe are focusing on building capabilities in critical minerals processing

| Country | Policy (Year) | Specifics on critical minerals processing |

|---|---|---|

| USA | Inflation Reduction Act (2022) | The IRA supports critical minerals processing projects through expanded loan guarantees and appropriations, removing innovation requirements to ease financing, and accelerate domestic refining and recycling activities. |

| Australia | Future Made in Australia Plan (2024) | The plan includes a USD 7 billion production tax incentive to promote the processing and refining of critical minerals, alongside USD 1.2 billion in strategic project funding and feasibility studies for shared processing infrastructure. |

| Russia | Update on Mineral Strategy (2050) | Russia's updated mineral strategy (to 2050) emphasises improving the processing of scarce mineral resources to meet industrial needs, and reduce import dependence. It focuses on enhancing geological exploration and refining capabilities aligned with updated strategic raw materials. |

| Country | Policy (Year) | Specifics on critical minerals processing |

|---|---|---|

| UK | Critical Mineral Strategy (2022) | This strategy focuses on boosting domestic refining and manufacturing capabilities to maximise value along the critical minerals supply chain. The emphasis is on cutting-edge research and innovation in refining, with goals to enhance sustainable and transparent mineral processing. |

| Japan | Critical Mineral Subsidy Programme (2023) | The programme provides grants covering up to 50 per cent of costs for smelting and refining projects of key critical minerals, including lithium-ion battery materials, rare earths, and semiconductor-related minerals. It also supports technology development and recycling efforts within mineral processing. |

| Canada | Critical Minerals Research, Development and Demonstration (2021) | The initiative allocates USD 192.1 million in federal funding to support the advancement of innovative processing technologies within the critical minerals sector. |

Source: Authors’ analysis based on US Department of Energy 2022; Gov. of UK 2023; Gov. of Canada 2021, and IEA 2025

In its mission to strengthen critical minerals supply chains, India has already taken significant steps. In 2023, 30 critical minerals were identified by the Ministry of Mines, followed by the Mines and Minerals (Development and Regulation) Act (MMDR) amendment, which selected 24 critical and strategic minerals, and empowered the central government to auction blocks of these minerals (Ministry of Mines 2023a). Recently, in the Union Budget of 2025, a dedicated amount of INR 16,300 crore was allocated to the National Critical Mineral Mission, one of whose eight components is critical minerals processing. This shows India’s commitment to strengthening domestic mineral processing and refining, thereby consolidating domestic mineral supply chains. Thus, it is evident that critical minerals would be at the centre stage of India’s policy landscape.

Currently, India relies heavily on imports to meet its critical mineral needs, making it vulnerable to market fluctuations and supply disruptions. The lack of domestic production has led to import dependence on minerals such as lithium, cobalt, nickel and vanadium entirely, which results in significant economic and strategic risks (Ministry of Mines 2023b). With the launch of the National Critical Mineral Mission and the first tranche of offshore mineral blocks, many more critical minerals block auctions will follow. Additionally, organisations such as Khanij Bidesh India Limited (KABIL), Coal India Limited and Oil India Limited are looking for critical mineral resources overseas. After detailed exploration, some of these blocks will go online for mine production and metal extraction in the upcoming years, fundamentally creating an opportunity to focus on developing critical minerals processing and refining capabilities.

India’s efforts to build domestic processing capabilities would not only strengthen its resilience, but also position the nation as a competitive alternative in the global supply chain, potentially making it a leader in the critical minerals landscape. The economic impact of these domestic critical minerals processing capabilities extends beyond immediate applications. Domestic processing of critical minerals would support India’s high-growth sectors, contribute to job creation, facilitate India’s transition to a decarbonised economy, and maximise domestic production and manufacturing capabilities in sustainable technologies and other strategic sectors. Thus, there is a pressing need to accelerate efforts towards domestic processing capabilities.

With decades of experience producing refined steel, aluminium, copper, zinc, and rare earth elements, India has the fundamental knowledge of mineral and metallurgical processing technologies. This advantage, along with lower labour costs, makes it one of the ideal locations for investments in critical minerals processing. However, significant efforts are required to build a resilient and secure critical minerals supply chain. By mapping India’s existing supply chain and processing capabilities through this study, we seek to lay out a clear path to develop a sustainable processing industry in India. Through our analysis, we have tried to bring up strategic actions to strengthen domestic production and minimise reliance on imports.

As we move toward a clean energy future, it is essential to analyse where we stand, identify the gaps, and find opportunities in India’s current mineral processing capabilities. This report focuses on 15 critical minerals—cobalt, copper, graphite, lithium, molybdenum, nickel, niobium, the platinum group of elements, rare earth elements, silicon, tin, titanium, tungsten, vanadium, and zirconium—which are essential for clean energy technologies, defence, aerospace, and other strategic sectors. While some of these critical mineral blocks have been auctioned for further exploration and mining, others are important for India’s clean energy transition and industrial growth.

The next section begins with an overview of methods for processing critical minerals, highlighting the techniques that are commonly used to process raw ore and produce pure elements or compounds. Next, we look into mineral deposits, their processing routes and the supply chain of the selected critical minerals. Following this, the report evaluates India’s position in the critical minerals processing landscape, mapping existing capabilities and identifying key bottlenecks and opportunities for growth. Finally, the report concludes with actionable recommendations for strengthening processing capabilities to reduce import dependence, and create a resilient domestic supply chain of critical minerals.

To maintain a focused approach and keep our research crisp, we have analysed the primary processing techniques of naturally occurring raw materials of these critical minerals, with some focus on the recovery of critical minerals as by-products, or from secondary sources. However, the report also highlights deep rooted challenges and policy constraints that need to be addressed, and proposes strategic interventions to potentially position India as a global leader in the processing of critical minerals.

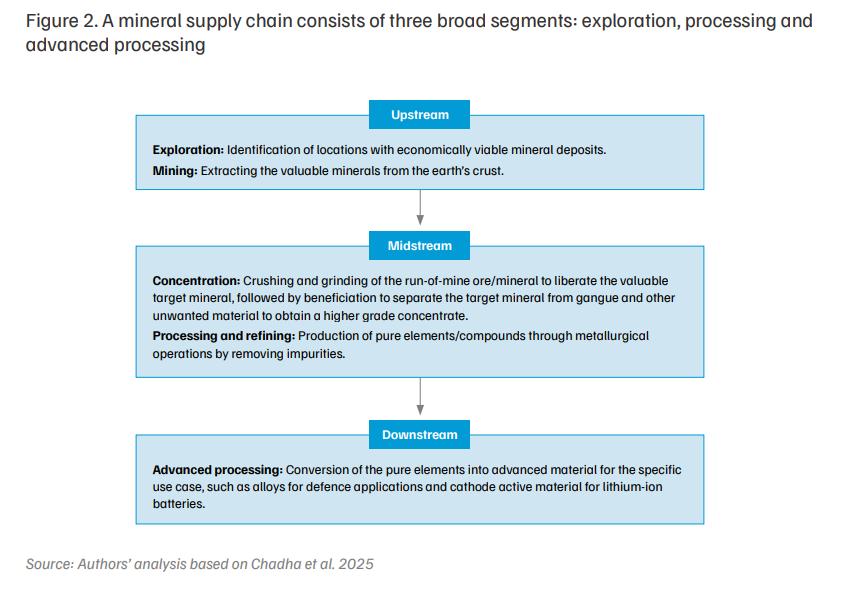

Critical minerals processing is the essential stage that converts raw (run-of-mine) ore/mineral into usable material by removing impurities and recovering valuable minerals. This step is positioned midstream of the overall mineral supply chain (Figure 2), connecting the upstream mineral exploration-mining operation with downstream advanced metallurgical processes that convert the purified critical minerals into advanced material for specific industries, such as electric vehicles, energy storage and defence.

Most critical minerals are not evenly distributed in the earth’s crust in their pure form. Instead, they occur naturally as a part of mineral deposits, often associated with other valuable or non-valuable minerals. For instance, copper is found with other critical minerals such as nickel, cobalt, platinum group elements (PGEs) and molybdenum in sulphide deposits. Similarly, monazite, a rare earth mineral, is found in placer deposits with titanium and zirconium minerals, which are also critical.

The concentration of different minerals in their respective deposits also varies across geographies. For example, lithium concentration differs between brine deposits in Chile (0.14 per cent average) and spodumene in Australia (1–3 per cent), while the newly discovered lithium deposit in Jammu and Kashmir has an average concentration of 583 parts per million (ppm) (VINACHEM 2022; Geoscience Australia 2023; Ministry of Mines 2023c). Similarly, the concentration of graphite varies from 5 to 80 per cent, depending on the deposit type (Indian Bureau of Mines 2024a).

Other than the valuable minerals, the rest of the raw ore includes unwanted impurities, mostly rocks and silica particles, commonly known as gangue, which are removed by processing these minerals. The varying concentrations of the target mineral because of – complex texture or association of various phases, and fine dissemination of target mineral – in the mineral deposits affect the processing complexity and cost of production. Typically, the deposit with a lower concentration of the target mineral requires a multi-step, complex processing approach to achieve the desired purity of the final product, resulting in an increase in the production cost.

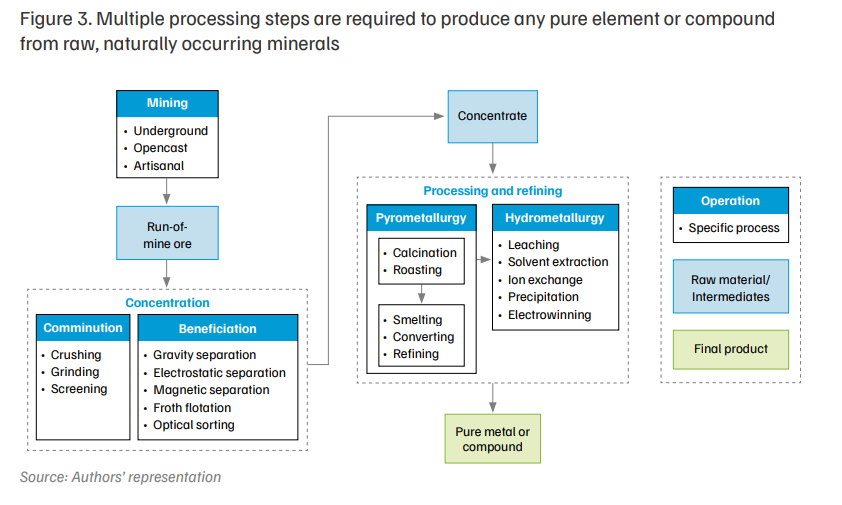

This section explores common methods used to process these naturally occurring minerals, focusing on the key methods, such as comminution, beneficiation and processing of concentrates to obtain valuable products. Broadly, comminution and beneficiation fall under mineral processing, and the subsequent processing of concentrate is technically known as extractive metallurgy. The processes involved in extractive metallurgy are further classified as hydrometallurgy and pyrometallurgy, with some minerals requiring a combination of both. A general processing route of critical minerals is represented in Figure 3, and the common steps are defined below.

This step is employed after the mining of raw ore/mineral. It improves the grade or quality of the ore by removing nonvaluable gangue and minerals such as quartz, feldspar, micaceous minerals, rock, etc., from valuable target minerals by utilising the difference in their physical properties.

Comminution involves reducing the size of run-of-mine ore/minerals to liberate valuable minerals. Its processes include:

Beneficiation separates valuable minerals from impurities (gangue), yielding a concentrate with a higher concentration (grade) of the desired valuable material. Some of the common beneficiation techniques include:

The concentrate obtained after mineral processing serves as feed for extractive metallurgy, wherein the valuable minerals/elements are extracted economically through metallurgical operations. The common metallurgical processes are discussed below in brief:

Pyrometallurgy involves converting the ore or concentrate at high temperatures, to segregate and recover the desired metal in a usable metal or compound form in one phase, while rejecting impurities, known as slag. In most instances, both phases are molten state because of high temperature operations. Some of the most common pyrometallurgical techniques involve:

Hydrometallurgy involves converting the ore or concentrate particles by dissolving the ore in a suitable aqueous medium at room temperature, or applying heat in some operations, to separate the waste and generate pure solution of the target mineral. Finally, the desired metal or its compound is precipitated from the solution through chemical or electrolytic means. Some of the common hydrometallurgical operations include:

Understanding the current status of global supply chains of critical minerals is important, especially from the perspective of geological distribution, availability of reserves, and technological expertise involved in processing. In this section, we highlight mineral-wise deposits of the select critical minerals, examining the nature of their deposits (such as primary or secondary sources), and their association with other minerals. This section also dives deep into industrial processing technologies, including mineral beneficiation to extractive metallurgy, and provides insights into global supply chains.

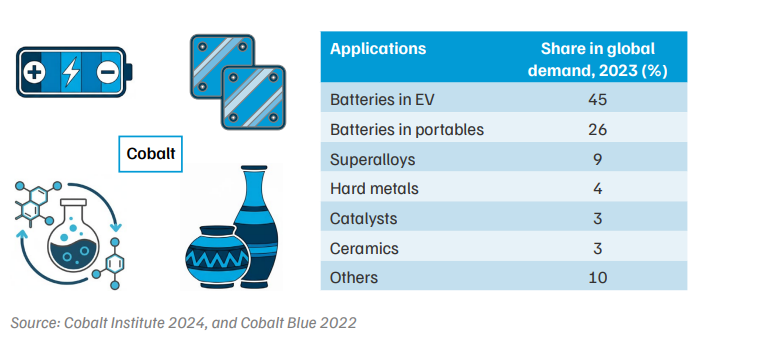

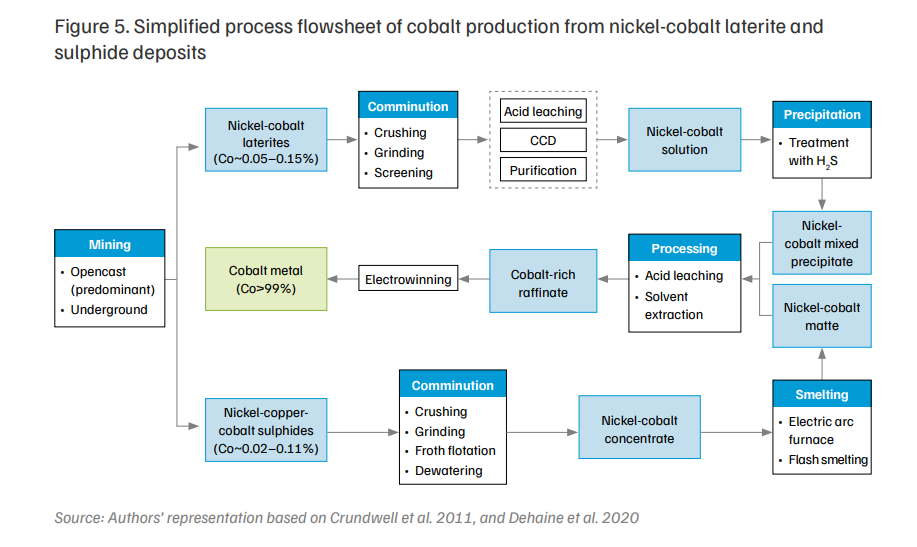

Cobalt, a silver-grey metal with a high melting point and ferromagnetic properties, is commonly used in superalloys and batteries because of its high energy density and stability.

Cobalt is never found in a pure form. Naturally, it is associated with elements like copper, nickel, iron, zinc, and platinum group of elements (PGEs). The major deposits which are exploited for commercial cobalt extraction are listed in Table 2.

Table 2. Different deposits of cobalt and their locations

| Cobalt deposits | Countries | Cobalt grade (%) |

|---|---|---|

| Sedimentary copper-cobalt sulphide and oxide deposits | D. R. Congo and Zambia | 0.2–1 |

| Nickel-cobalt laterite deposits | Australia, Indonesia, and the Philippines | 0.05–0.15 |

| Magmatic nickel-copper-cobalt deposits | Australia, Russia, Finland, USA, and Canada | 0.02–0.11 |

Source: Authors’ analysis based on Dehaine et al. 2020

Due to its lower concentration (0.02–1 per cent) in mineral deposits, most cobalt is produced as a by-product of copper and nickel. According to the Cobalt Institute (2022), 60 per cent of cobalt is mined during copper mining, and 38 per cent comes from nickel mining. Cobalt recovery from its deposits requires a complex, multi-step processing route, customised according to the type of deposit being processed, and the desired product purity.

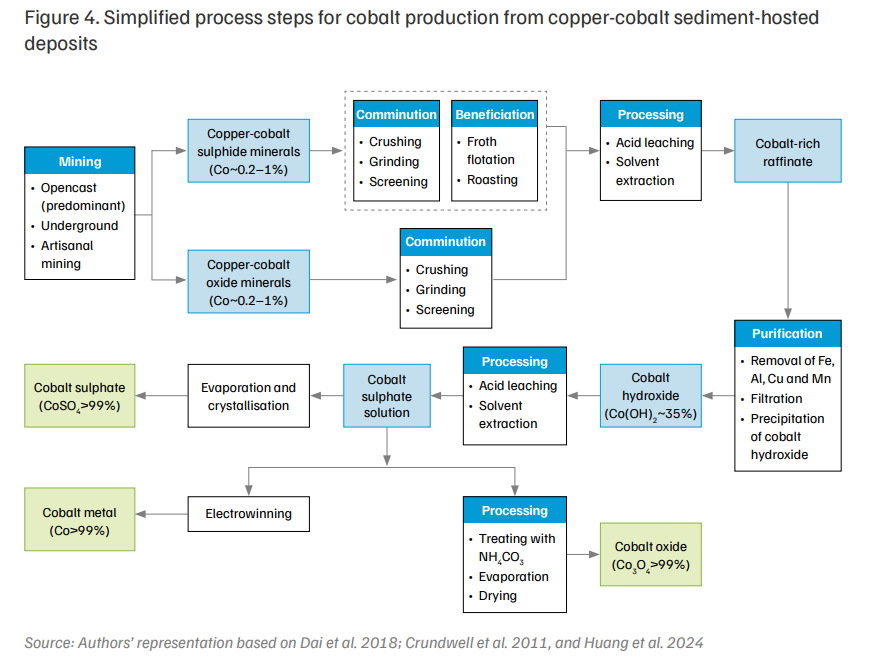

For copper-cobalt sediment-hosted deposits, typically, the processing steps involve leaching, solvent extraction, and electrowinning to yield high-purity cobalt. First, the ore is crushed, ground and concentrated through froth flotation, then roasted to convert sulphides to oxides, which are then leached with sulphuric acid. After purification, cobalt and copper are separated through solvent extraction and cobalt is precipitated as cobalt hydroxide, which is further refined for the production of battery-grade cobalt compounds (Dai et al. 2018).

During refining, cobalt hydroxide undergoes leaching, impurity removal and crystallisation to produce battery grade cobalt sulphate or cobalt oxide, as shown in Figure 4. Electrowinning from cobalt sulphate completes the process, yielding metal of over 99 per cent purity, essential for battery materials (Crundwell et al. 2011).

Cobalt production from nickel-cobalt laterite deposits is achieved through high-pressure acid leaching (HPAL). In this hydrometallurgical process, the pre-concentrated limonite ore is leached with sulphuric acid in an autoclave under high pressure and temperature, achieving 95 per cent cobalt recovery in the leach liquor. The solution is purified, and cobalt is separated by treating it with hydrogen sulphide, forming a mixed nickel-cobalt sulphide precipitate. This precipitate is further acid leached; cobalt and nickel are separated via solvent extraction, and cobalt is electrowon to achieve over 99.95 per cent purity. Alternatively, purified cobalt may be processed into powder or briquettes, as shown in Figure 5.

In the case of cobalt production from nickel-copper-cobalt sulphide deposits, the concentrate is smelted, producing a nickel-cobalt matte, further refined by acid leaching in the presence of oxygen. Solvent extraction is used to separate nickel, leaving a cobalt-rich solution. Finally, cobalt is either electrowon to produce cobalt metal or treated to produce cobalt powder, yielding an overall cobalt recovery rate of approximately 40 per cent (Dehaine et al. 2020).

Cobalt’s supply chain is concentrated in a few countries. As per US Geological Survey estimates, the mine production of cobalt was estimated to be 290 kt in 2024, with D. R. Congo being the leading producer, contributing 76 per cent. Indonesia was the secondlargest producer, and together, these two countries accounted for over 86 per cent of the global cobalt mine production (US Geological Survey 2025). The total production of refined cobalt was nearly 224 kt in 2024, with China being the leading producer of refined cobalt, accounting for 79 per cent (Cobalt Institute 2025). However, China’s cobalt reserves account for only 1.88 per cent of the global figure, and the nation is dependent on imports of more than 90 per cent of cobalt raw materials (Huang et al. 2024)

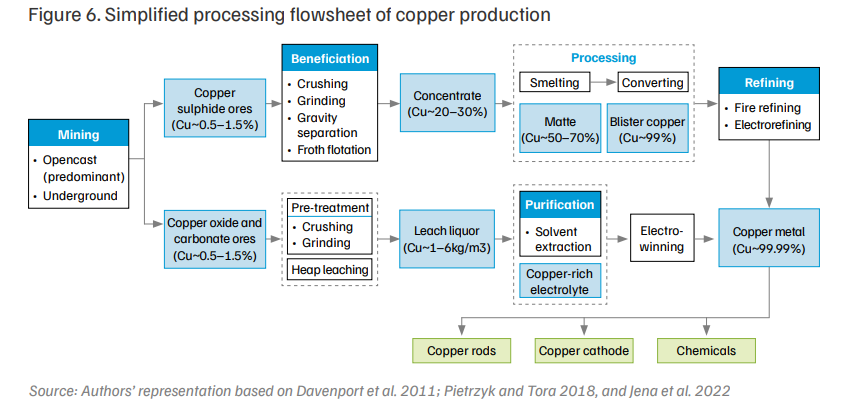

Copper is a reddish-brown metal known for its ductility, excellent electrical and thermal conductivity, and corrosion resistance. It is the third-most-used industrial material after steel and aluminium, mainly used in various construction and electrical applications.

Copper occurs naturally in the earth’s crust in various deposits, and approximately 90 per cent of the copper ores are found in sulphide form (Pietrzyk and Tora 2018). The rest are found in carbonate and oxide deposits, and rarely as pure metallic copper. Most copper is commercially produced from sulphide deposits, prominently from chalcopyrite ore. Other minerals of copper include bornite, chalcocite, azurite and malachite. In the sulphide deposits, copper remains associated with other valuable minerals, including nickel, cobalt, molybdenum and selenium, and is recovered as a by-product during copper processing (Indian Bureau of Mines 2024d).

The copper production route varies depending on the copper deposit and its concentration. Copper production from sulphide ores primarily relies on a series of pyrometallurgical processes, accounting for 80 per cent of primary copper production. Initially, the ore undergoes comminution and beneficiation to yield a copper concentrate with a copper content of 20–30 per cent (Jena et al. 2022). The concentrate is then smelted and converted in a Pierce Smith Converter to remove iron and sulphur, forming blister copper (99 per cent copper). Finally, blister copper is refined through fire and electrorefining, yielding high-purity copper suitable for electrical use (Davenport et al. 2011).

In contrast, copper production from oxide, carbonate and chalcocite ore follows a hydrometallurgical route, and accounts for the remaining 20 per cent. After crushing and beneficiation, dilute sulphuric acid is applied to ore heaps, dissolving copper into a leach liquor, a process known as heap leaching, as shown in Figure 6. This solution (leachate), containing one to six grams of copper per litre, is purified through solvent extraction. The resulting copper-rich electrolyte undergoes electrowinning, producing high-purity copper suitable for industrial applications (Davenport et al. 2011).

Copper reserves are distributed globally. However, the majority of reserves are in South America and the Australian continent. According to the US Geological Survey, out of the 980 million tonnes of global copper reserves, Chile possesses the largest, accounting for 19 per cent, followed by Peru and Australia, with each nation possessing 10 per cent of copper reserves. Chile also leads the mine production of copper, accounting for 23 per cent in 2024 out of 23 million tonnes. D. R. of Congo and Peru come next, contributing 14 per cent and 11 per cent, respectively. China dominates refined copper production, accounting for 44 per cent of the global 27 million tonnes in 2024, followed by D. R. Congo and Chile, contributing 9 per cent and 7 per cent respectively (US Geological Survey 2025).

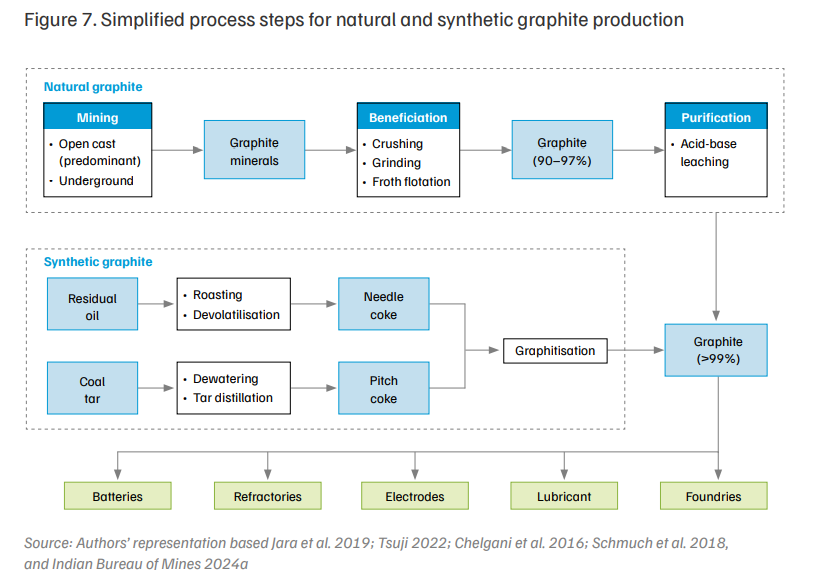

Graphite, a stable form of carbon with a greyish-black appearance, is soft to the touch and highly conductive to heat and electricity. Because of its chemical inertness, it is used in batteries, lubricants and metallurgical operations. In Lithium-ion batteries, graphite is used in anodes, enhancing its thermal stability and efficiency, and it can constitute up to 17–20 per cent of a battery’s weight. There are two types of graphite: synthetic and natural.

Natural graphite is commonly associated with metamorphic rocks, and is often found with other minerals such as quartz, calcite, and micas. Graphite is naturally produced as flaky and amorphous graphite, and artificially, as synthetic graphite. Flaky and synthetic graphite is considered suitable for battery applications, and synthetic graphite holds 80 per cent of the market share for battery anode material (IEA 2024b). The mined natural graphite contains carbon in the range of 5–80 per cent, depending on the type of deposit, and the lower-grade run-of-mine ore is processed to improve graphite grade and remove impurities. Synthetic graphite is produced from residual oils and coal tar, accounting for 66 per cent of the total graphite supply in 2021 (Natural Resources Canada 2024b).

Upon mining, natural graphite processing begins with the crushing and grinding of run-ofmine ore to prepare fine particles for froth flotation. In this process, kerosene is used as a collector, methyl isobutyl carbinol (MIBC) as a frother, and sodium silicate as a depressant, producing a concentrate with up to 97 per cent graphite (Tsuji 2022). For higher purity, processes such as reverse flotation, electrostatic separation, air classification, acid or base leaching may be employed at high temperatures (about 500°C). This involves treating the concentrate with sodium hydroxide, which forms water-soluble silicates removed by leaching to yield a graphite grade above 99 per cent (Jara et al. 2019; Chelgani et al. 2016).

Synthetic graphite production involves transforming petroleum residual oil and coal tar into high-purity graphite through multiple heating stages. Residual oil from crude oil refineries undergoes coking to yield green petroleum coke, which is further heated in a rotary kiln to produce calcined petroleum coke with up to 99.5 per cent carbon. However, through this process, only a small fraction—needle coke—achieves the purity and structure needed for battery applications. Alternatively, coal tar from the coke-making process is distilled and then heated at high temperatures to form pitch coke. Both needle and pitch coke undergo graphitisation, heating to 2600–3300°C, to obtain graphite with over 99 per cent purity.

China dominates the global graphite supply chain. In 2024, China was responsible for 79 per cent of graphite production out of 1.6 million tonnes, and the top-three countries - China, Madagascar and Mozambique - accounted for nearly 90 per cent of global graphite production. While the graphite reserves are somewhat more diversified, China still leads with 28 per cent of graphite reserves, followed by Brazil with 26 per cent out of a total of 290 billion tonnes. The top-five countries hold 77 per cent of global graphite reserves (US Geological Survey 2024t). For refined spherical graphite, suitable for battery anodes and produced through spherodisation of purified natural graphite, China dominates with 99 per cent of the market share, highlighting the concentration of battery grade graphite supply (IEA 2024).

Graphite is used to manufacture monocrystalline silicon solar cells for solar photovoltaic (PV) modules. Monocrystalline silicon solar cells are produced from silicon ingots grown through the Czochralski process, where seed silicon is drawn slowly upwards from a bath of melted polysilicon by a Czochralski puller from a crucible. During this process, crucibles are heated by ‘hotzone’ to temperatures of 1,500°C (Mersen 2024). Hotzone materials are made of various kinds of graphite (ESIA 2024), such as isostatic graphite, graphite felt, hard felt, graphite, soft felt, etc. Isostatic graphite, produced by isostatic moulding, is predominantly used in hotzones due to its physical and chemical properties, such as high chemical stability, thermal conductivity, and mechanical strength (Liu et al. 2024)

Solar PV is the largest application area for isostatic graphite. With the predicted increase in global solar manufacturing capacity to around 1,300 GW by 2028 (Joshi 2024), the demand for isostatic graphite is expected to increase. While Adani Solar has announced plans for a 2 GW manufacturing capacity of monocrystalline silicon ingot (Yuen 2024), domestic demand for isostatic graphite does not exist as Czochralski pullers and their crucible manufacturing are concentrated in China (ESIA 2024).

Isostatic graphite is a crucial consumable in producing crystalline silicon ingots and wafers from polysilicon. A thousand tonnes of isostatic graphite is required per one GW of a completely integrated solar PV manufacturing supply chain, from polysilicon to module (ESIA 2024). Currently, India’s solar module manufacturing capacity is 89.8 GW (Mercom Capital Group 2024, 2025). Hence, indigenising this entire module manufacturing capacity would require 89,800 tonnes of isostatic graphite supply

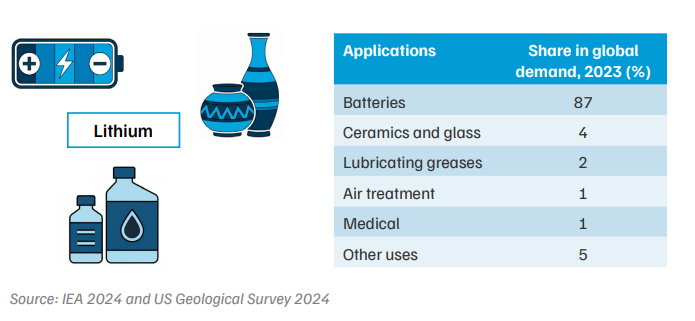

Lithium is a soft, silver-grey metal known for its reactivity, high specific heat and conductivity. Predominantly used in high-energy-density lithium-ion batteries for electric vehicles, it is also used in ceramics, glass, lubricants, air treatment, aluminium smelting and pharmaceuticals.

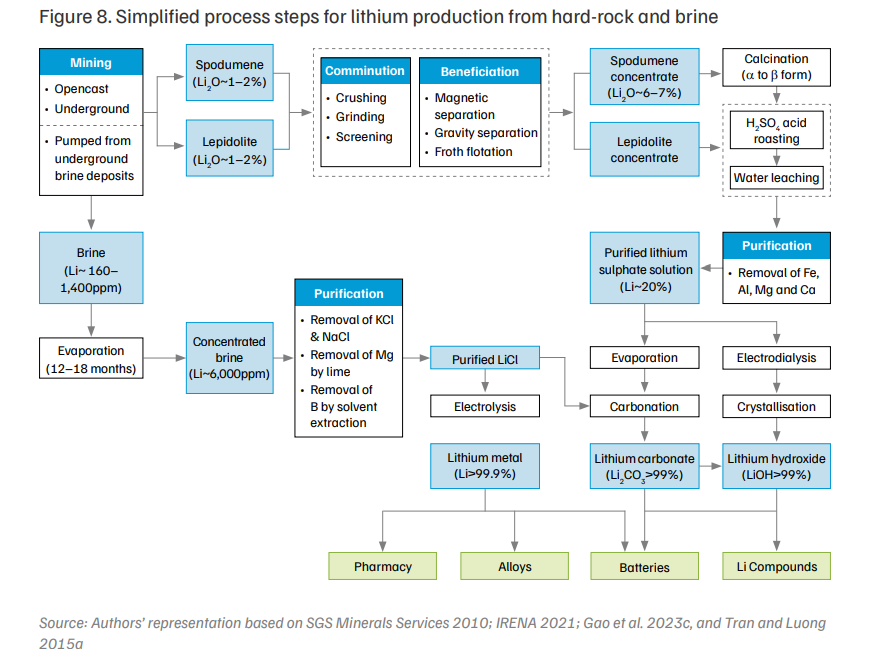

In the earth’s crust, lithium is associated with other alkali and alkaline elements, such as sodium, potassium, magnesium and aluminium. Several deposits of lithium have been identified, listed below in Table 3. However, most lithium is commercially extracted from pegmatite deposits (hard-rock deposits), which host spodumene and lepidolite minerals. Spodumene, a lithium aluminium silicate mineral, is currently the main mineral in lithium production. In 2023, hard rock contributed approximately 63 per cent of the global lithium supply (IEA 2024a). Brines are chloride salt lakes formed underground, containing 200 to 2,000 parts per million (ppm) of lithium and other elements such as potassium, sodium, boron and magnesium. Lithium clay deposits are another potential lithium source, forming 7 per cent of global lithium resources, and processes are being developed across the globe to recover lithium (Zhao, Wang and Cheng 2023a).

| Lithium deposits | Countries | Lithium grade (%) |

|---|---|---|

| Pegmatite deposits | Australia, USA, Canada, Zimbabwe, and China | 0.5–3 |

| Closed-basin brines | Australia, Indonesia, and the Philippines | 0.05–0.2 |

| Lithium clay deposits | Mexico, Siberia, USA, and India | 0.05–1.8 |

Source: Authors’ analysis based on Marcinov et al. 2023, and Zhao, Wang and Cheng 2023

Lithium production from spodumene begins with comminution, followed by beneficiation to obtain a concentrate with 6–7 per cent lithium oxide (SGS Minerals Services 2010). The concentrate undergoes high-temperature (950–1100°C) calcination (also known as decrepitation), making it amenable to sulphuric acid leaching. After calcination, the material is acid-roasted at 250–300°C and then water-leached. The leach solution is then purified by adding lime and sodium carbonate to eliminate impurities. The purified solution evaporates, followed by sodium carbonate addition, resulting in the precipitation of lithium carbonate with over 99 per cent purity (Gao et al. 2023b).

Lithium extraction from brine involves evaporating lithium-rich brines in large ponds for 12–18 months, to concentrate lithium to 6 per cent by weight. During evaporation, impurities settle down, and the concentrated brine undergoes purification through hydrometallurgical treatment, to remove magnesium and boron, as shown in Figure 8. Finally, the lithium chloride solution is either electrolysed to produce lithium metal, or treated with sodium carbonate to precipitate lithium carbonate, achieving over 99 per cent purity for industrial applications (Cabello 2021; Tran and Luong 2015a).

The global supply chain of lithium is concentrated just in a few countries, with the majority of reserves being possessed by just four countries—Chile (31 per cent), Australia (23 per cent), Argentina (13 per cent) and China (10 per cent) out of 30 million tonnes. Australia leads in hard-rock mining, accounting for 37 per cent of the 0.24 million tonnes of global lithium supply in 2024. The next two countries are Chile, which dominates in brine production, holding 20 per cent of the global lithium supply, and China, which produces both hard-rock and brine. These three countries hold 74 per cent of global lithium mine production (US Geological Survey 2025). China leads the refining of raw lithium materials, accounting for 59 per cent of the total in 2022 (LTRC 2022). It processes the lithium minerals and brines mined locally, and the imported hard-rock concentrate from Australia and Africa. According to the International Energy Agency (IEA), China is expected to dominate lithium refining and hold 60 per cent of refining capacity by 2030 (IEA 2024a).

Lthium-ion batteries (LIBs) are used for electric vehicles (EVs), consumer electronics and grid-scale energy storage. The market of LIBs has been growing exponentially and is expected to continue to do so. Various chemistries are available for LIBs, each with a different application: Lithium Cobalt Oxide (LCO), Lithium Manganese Oxide (LMO), Lithium Nickel Manganese Cobalt Oxide (L-NMC), Lithium Iron Phosphate (LFP), etc. Currently, India does not manufacture cathode materials, but Altmin and Himadri Chemicals have announced plans to start manufacturing cathode materials at giga-scale by 2030 (EVreporter.com 2023, 2024).

Recently, LMFP battery chemistries have been considered to replace LFP due to their higher energy density than LFP and lower price than NMC (EY 2024). According to projections based on the current scenario, the Indian market is expected to be led by NMC-622, NMC-811 and LFP chemistries, with the share of LFP slowly increasing due to the deployment of grid-scale BESS (CEEW 2023). To cater to the growing battery demand, the requirement for lithium in India will increase, and alternative chemistries, such as sodium-ion batteries (SIBs), have a long way to go before making any significant impact on the lithium demand for batteries.

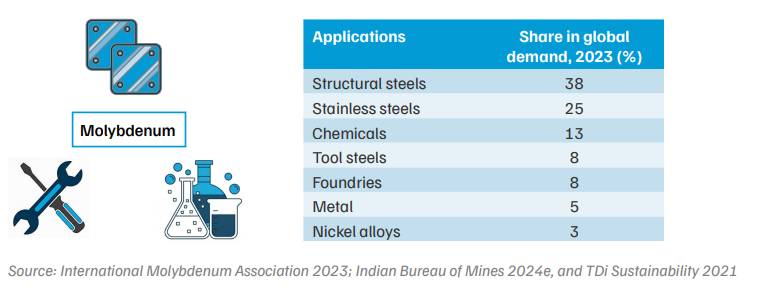

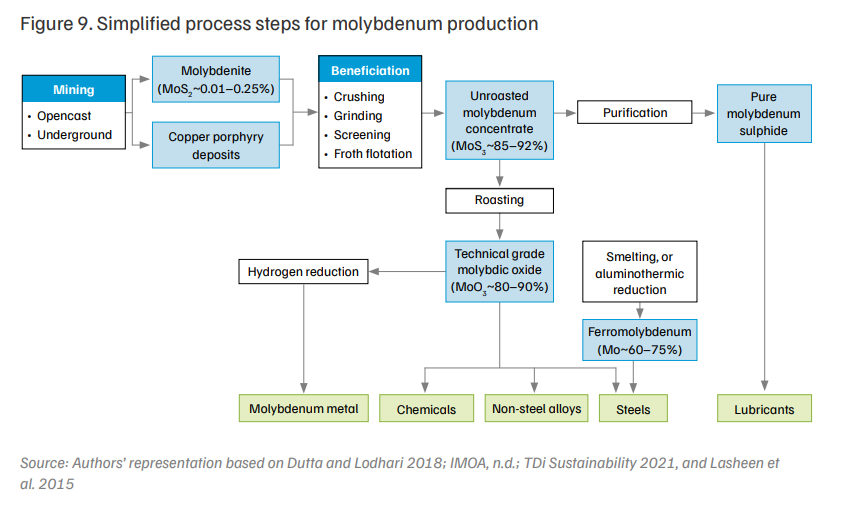

Molybdenum is a silver-white transition metal with the ability to enhance strength, toughness and hightemperature stability. It is mostly used as an alloying agent in stainless steel and titanium alloys.

Molybdenite (MoS2 ) is the primary ore exploited at an industrial scale for molybdenum extraction. However, two-thirds of global production comes as a by-product from porphyry copper sulphide deposits, with the remaining produced through primary molybdenite ore mining, predominantly in China. The concentration of molybdenum in its deposits, considered viable for extraction, ranges from 0.01 to 0.25 per cent (TDi Sustainability 2021; Indian Bureau of Mines 2024e).

Typically, molybdenum production from primary ore involves comminution and beneficiation via froth flotation, followed by roasting. In copper-molybdenum ores, copper is separated from molybdenum by leaching with ferric chloride. The resulting concentrate, unroasted molybdenum concentrate (UMC), typically has a molybdenite content of around 85–92 per cent and is roasted at 500–650°C in rotary or multiple-hearth kilns, to obtain technical-grade molybdic oxide (TGMO) (Lasheen et al. 2015). This marketable product is further processed based on the application requirements in steelmaking, non-steel alloys, and chemicals (TDi Sustainability 2021), as shown in Figure 9. Molybdenum is also recycled; recycled molybdenum constitutes nearly 30 per cent of the global supply of the metal (US Geological Survey 2024d). Molybdenum gets recycled during old and new steel scrap recycling; there are no separate processes for recycling it.

Like other critical minerals, the supply chain of molybdenum is also concentrated in a few nations. In 2023, the global mine production of molybdenum was estimated to be 260 thousand tonnes, and 85 per cent of molybdenum mining was concentrated in the top-four countries—China, Peru, Chile and USA—which possess 85 per cent of global production. Total global estimated reserves are be 15 million tonnes (US Geological Survey 2025). China holds a dominant position in the molybdenum supply chain, as it accounted for 81 per cent of global ferromolybdenum production in 2021, 42 per cent of molybdenum mine production in 2024, and possesses 39 per cent of global reserves (European Commission 2023b; US Geological Survey 2025).

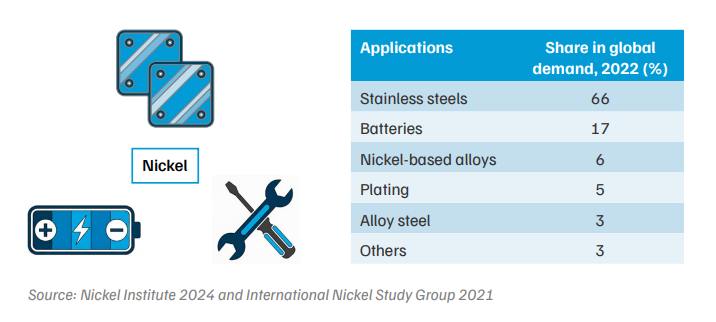

Nickel is a silver-white metal with a high melting point, excellent strength, corrosion resistance and oxidation stability at elevated temperatures. Known for its ability to form alloys, nickel is mostly used in stainless steel and NMC batteries.

Nickel is the fifth-most-abundant element in the earth’s crust by weight, with an average concentration of 68–80 ppm. It is naturally associated with iron, copper, cobalt, magnesium, and aluminium. Commercially, it is extracted from laterite deposits and sulphide deposits. According to the International Nickel Study Group (INSG), 40 per cent of nickel resources are in sulphide deposits, and 60 per cent are in laterite deposits (Zevgolis and Daskalakis 2022; International Nickel Study Group 2021; Henckens and Worrell 2020a).

Table 4. Different deposits of nickel and their locations

| Nickel deposits | Countries | Nickel grade (%) |

|---|---|---|

| Nickel laterite deposits | Indonesia, New Caledonia, the Philippines, and Australia | 1–1.6 |

| Nickel sulphide deposits | Russia, Canada, China, and Australia | 0.2–2 |

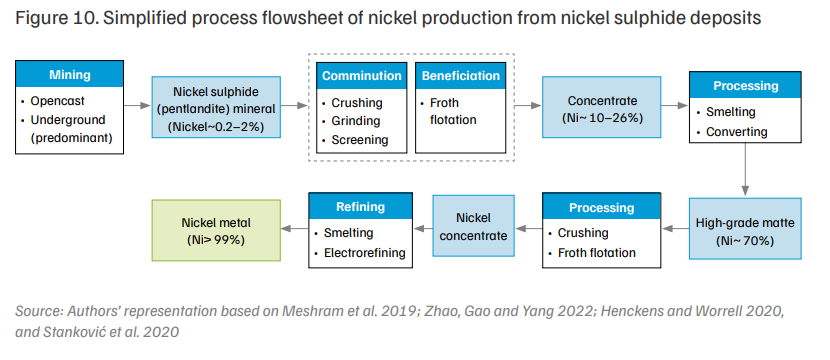

In sulphide deposits, the nickel grade is 0.2–2 per cent, with pentlandite being the principal commercially exploited mineral. After mining, the sulphide ore is crushed, ground, and sent to the beneficiation facility to improve the nickel grade in the concentrate by subjecting the ore particles to magnetic separation, gravity separation, and froth flotation. Finally, nickel concentrate is produced with 10–26 per cent nickel content, and is processed via the pyrometallurgical route of smelting, converting and refining (Zhao, Gao and Yang 2022; Meshram et al. 2019), as shown in Figure 10.

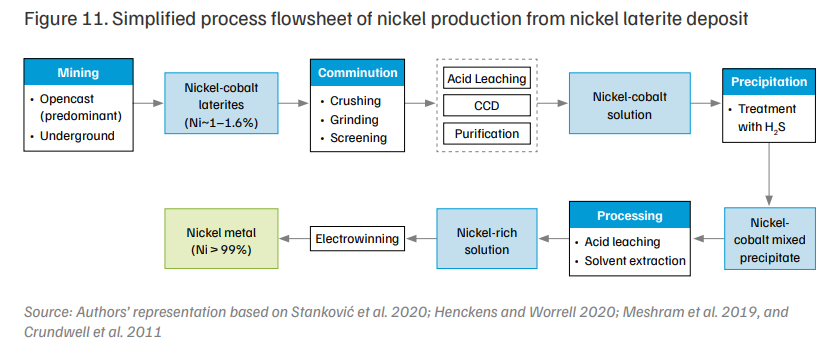

The nickel grade in the laterite deposits is 1–1.6 per cent. The principal minerals are limonite, which has high iron content and low magnesium, and garnierite, which has high magnesium and low iron content. In contrast to the sulphide ores, nickel laterite concentrates, containing nickel in the range of 3–5 per cent, are processed via the hydrometallurgical route (Figure 11), involving processes such as leaching, counter-current decantation, solvent extraction and electrowinning (Stanković et al. 2020; Henckens and Worrell 2020b; Meshram et al. 2019b).

A few countries dominate nickel reserves and production, and Asia is the leading continent in the supply chain. As per US Geological Survey, the global nickel reserves are estimated to be more than 130 million tonnes in terms of metal content in 2024. Indonesia alone holds 42 per cent of global nickel reserves. The top-three countries—the other two being Australia and Brazil—have more than 70 per cent of nickel reserves. In 2024, the global mine production of nickel was estimated to be 3.7 million tonnes, with Indonesia being the leading producer, contributing 59 per cent. The Philippines and Russia were the second- and third-largest producers, and together, these countries accounted for 74 per cent of the global nickel mine production (US Geological Survey 2025). The total production of refined nickel was more than 3.1 million tonnes, with Indonesia being the leading producer, accounting for 37 per cent. China was the second-largest producer of refined nickel, accounting for 27 per cent (British Geological Survey 2024a).

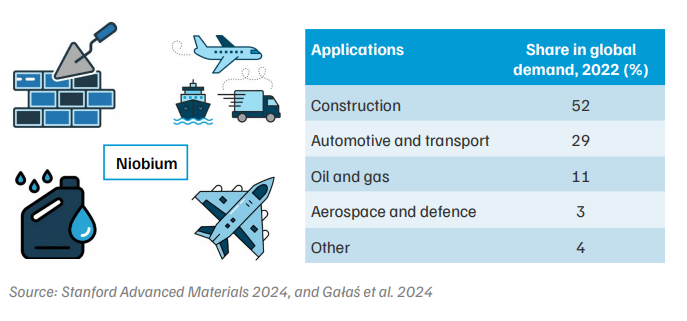

Niobium is a lustrous grey metal known for its high melting point, low density and superconducting properties. Primarily used in High-Strength Low-Alloy (HSLA) steels for construction and automotive use, niobium enhances its strength and corrosion resistance.

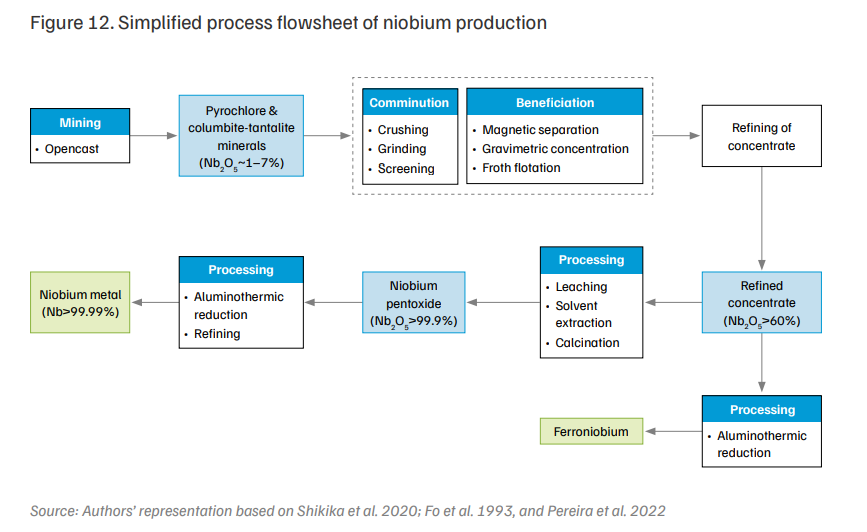

Although niobium is found in many minerals, only two niobium-containing minerals are economically viable to extract: columbite-tantalite, which can contain up to 76 per cent niobium pentoxide (Nb2 O5 ) and pyrochlore, with up to 71 per cent Nb2 O5 . One of the largest pyrochlore deposits is in Araxá, Brazil, which is the world’s main source of niobium globally, and is operated by the Companhia Brasileira de Metalurgia e Mineração (CBMM) (Pereira et al. 2022). Since niobium is found close to the surface, it is mined through open-pit mining methods, using heavy machinery like bulldozers and dump trucks.

For high-strength low-alloy (HSLA) steel production, pyrochlore is processed into ferroniobium, while niobium hydroxide is produced from columbite-tantalite minerals. Ferroniobium production starts with comminution, followed by beneficiation, involving magnetic separation, gravimetric concentration and froth flotation, yielding a niobium oxide concentrate with approximately 55–60 per cent niobium. The concentrate undergoes refining in an electric arc furnace using coal or coke as reducing agents to remove impurities such as phosphorus and sulphur. The final aluminothermic reduction step requires aluminium powder, iron scrap, and refined concentrate to produce ferroniobium, which contains about 65 per cent niobium, and is formed into ingots for industrial applications (Shikika et al. 2020a; Fo et al. 1993).

For applications which require niobium pentoxide, the concentrate is subjected to an acidleaching process, initially with sulphuric acid, followed by hydrofluoric acid to dissolve residual particles, as shown in Figure 12. Solvent extraction isolates niobium ions from leach liquor, and hydrated niobium pentoxide is precipitated with ammonia. After filtration and calcination, the resulting niobium pentoxide reaches a 99.9 per cent purity, which is essential for electronics and other specialised industries. Niobium metal is produced through further refining, involving aluminothermic reduction of niobium pentoxide to yield molten niobium, which is cooled and cast into ingots. For nuclear and aerospace applications, additional purification via electron beam melting removes impurities to achieve over 99.99 per cent purity (Pereira et al. 2022).

According to the US Geological Survey, Brazil dominates the niobium supply chain, holding 94 per cent of the estimated global 17 million tonnes of niobium reserves. This nation also leads the mine production of niobium, contributing 90 per cent in 2024, and 88 per cent of refined niobium in 2021. Canada is the second-largest global player in the niobium supply chain, with 9.4 per cent of global reserves, accounting for 6 per cent of mine production in 2024, and 10 per cent of refined production in 2021 (US Geological Survey 2024g; European Commission 2023c).

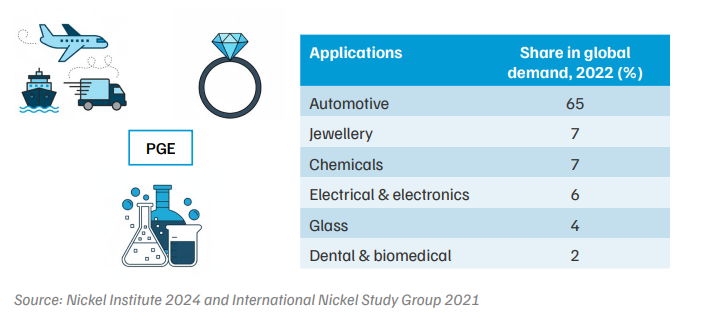

The platinum group elements (PGEs)—platinum (Pt), palladium (Pd), rhodium (Rh), iridium (Ir), osmium (Os) and ruthenium (Ru)—are high-melting, silver-white metals known for heat resistance and catalytic properties

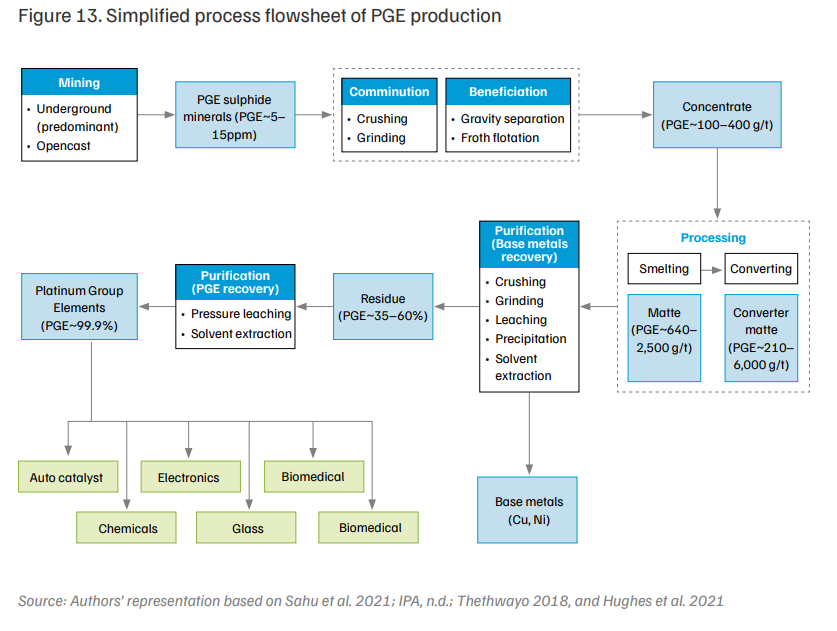

Platinum group elements (PGEs) are rarely found in their pure elemental form, and are often associated with sulphides and arsenides in chalcopyrite, iron pyrites and pentlandite deposits. These elements are extracted commercially from chalcopyrite deposits, wherein PGE concentrations range from 5 to 15 ppm. These minerals are deep-seated, and generally mined through underground mining (Thethwayo 2018; US Geological Survey 2017).

The PGEs begin with comminution at the mine site, where crushing and grinding operations liberate PGE and copper particles. Following this, beneficiation involves gravity separation and froth flotation, yielding a concentrate with 60–90 per cent PGE recovery (Hughes et al. 2021). This concentrate then undergoes smelting, producing molten matte, containing iron, sulphur and base metals, which are removed in a converting process. Next, the base metals, such as copper and nickel, are removed through hydrometallurgical methods, leaving a PGErich residue, as shown in Figure 13. Finally, PGEs are recovered by subjecting the residue to pressure acid leaching, solvent extraction, and melting to reach 99.9 per cent purity, ready for industrial use (Nose and Okabe 2014; Thethwayo 2018).

The primary production of PGEs from their deposits is a lengthy process with high production costs, which results in these being expensive elements. This process has several challenges, such as huge electricity requirements for the comminution and smelting operations. The smelting operation requires high temperatures (~1,500–1,650°C), which causes premature refractory lining failure due to excessive heat and inadequate cooling mechanisms, leading to disruption in operation and loss of production. Removing unwanted elements during the purification of converter matte and producing highly pure PGEs is also a complex process, and needs technical expertise (Thethwayo 2018).

The production of PGEs is highly concentrated in South Africa at the Bushveld complex, which contains two veins of PGEs, known as Merensky and Upper Group 2 (UG2) reefs—the largest global deposits of PGEs. South Africa alone holds 78 per cent of global PGE reserves (out of 81,000 tonnes), and contributed to 71 per cent of platinum production (out of 170 tonnes) in 2024. Russia was the leading palladium producer in 2024, accounting for 39 per cent out of 190 tonnes, and holds 20 per cent of global PGE reserves. Russia and South Africa accounted for 77 per cent of palladium production in 2024 (US Geological Survey 2025).

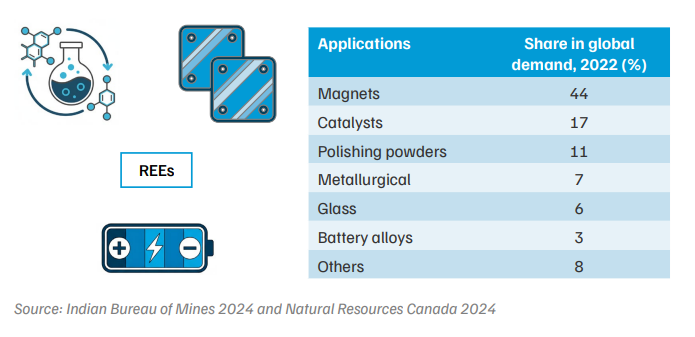

Rare earth elements (REEs) are a collection of 17 silver-white metals, including 15 lanthanides (elements from lanthanum to lutetium), plus yttrium and scandium. Based on atomic weight, natural abundance and similarities in their chemical properties, they are divided into light REEs (LREEs) and heavy REEs (HREEs). Known for their unique properties, REEs are essential in high-tech and defence applications.

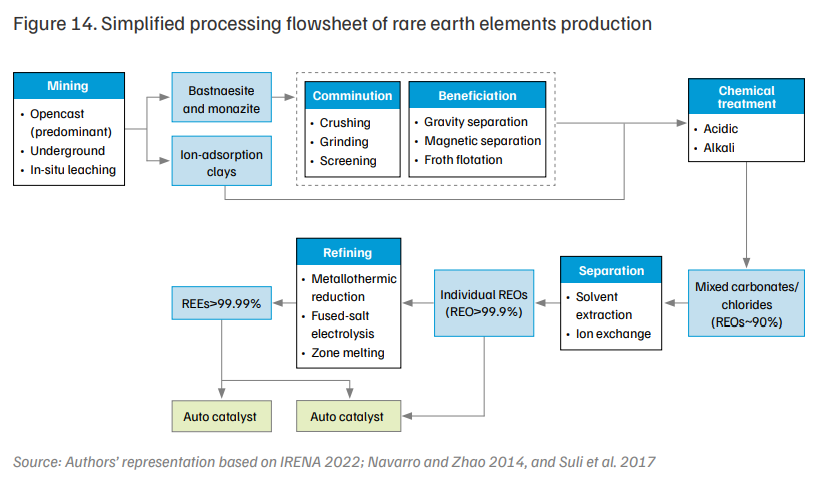

Rare earth elements are uncommon in nature in their pure form, and a limited number of deposits globally are being exploited to extract them. Bastnaesite, monazite, mixed ore containing bastnaesite, xenotime and monazite minerals and ion-adsorption clays are the mineral deposits from which REEs are extracted commercially.

Rare earth element production processes vary significantly, depending on the mineral type and its associated impurities. This diversity requires different processing routes with tailored parameters to maximise efficiency and recovery. Generally, processing of a rare earth ore involves a combination of hydrometallurgical and pyrometallurgical techniques, wherein the REE-bearing concentrate obtained after the comminution and beneficiation step undergoes acid or alkaline treatment, yielding a solution of mixed carbonates or chlorides. Extraction of the HREEs from the ion-adsorption clays includes leaching with sodium chloride solution in acidic media, or a solution of ammonium sulphate.

This solution is subjected to multiple solvent extraction or ion exchange processes to separate the individual rare earth oxides (REOs) with a purity of more than 99 per cent. Once separated, the REOs are further reduced and refined to achieve REE purity levels exceeding 99.99 per cent, often through metallothermic reduction, fused-salt electrolysis, or zone melting (Suli et al. 2017; Navarro and Zhao 2014), as represented in Figure 14.

The global supply chain of REEs is concentrated in a few countries. Out of an estimated 90 million tonnes, the top five countries hold 90 per cent of global reserves, with China alone accounting for 49 per cent. China is a dominant player in REE production, contributing 69 per cent of the global figure in 2024. China, USA, and Myanmar were together responsible for 89 per cent of the 0.39 million tonnes of global rare earth mine production in the same year (US Geological Survey 2025). Regarding refined REE production, China alone accounted for 88 per cent in 2021, while Malaysia and India accounted for 7 per cent and 2 per cent, respectively (European Commission 2023d).

Critical minerals in wind turbines mainly involve REEs in permanent magnets, which are used in wind turbine generators and gearboxes. Permanent magnets make it possible to have small, light, space-saving designs for the gearboxes of wind turbines (Gielen and Lyons 2022). Permanent magnets use neodymium (Nd) and praseodymium (Pr) to improve their magnetic strength, whereas dysprosium (Dy) and terbium (Tb) improve their susceptibility to demagnetisation, especially at high temperatures (Verma et al. 2022). A typical permanent magnet for a wind turbine comprises 28.5 per cent Nd, 4.4 per cent Dy, 1 per cent boron and 66 per cent iron. Permanent Magnet Synchronous Generators (PMSGs) are highly used in offshore turbines requiring Nd and Dy, with 216 kg/MW Nd and 17 kg/MW Dy (Verma et al. 2022). Permanent magnet drive systems dominate the offshore market, whereas induction generator drive systems, which don’t employ permanent magnets, are slightly more dominant in the onshore wind sector (IRENA 2022).

Rare earth minerals are sufficiently abundant today to meet the future demand of a wind industry that only represents a fraction of their end uses. From 2023 to 2030, the demand for Chinese wind energy Rare Earth Permanent Magnets (REPM) may fall by 14 per cent CAGR for onshore installations, and grow by only 4 per cent for offshore installations. By 2030, China is forecast to account for only 19 per cent of wind energy REPM demand, against 64 per cent in 2023. Given the average REPM grade and Pr, Nd, Dy, and Tb content assumptions, the global non-China wind energy sector will require a cumulative 30,000 tonnes of rare earth materials by 2030 (GWEC 2023).

Assessments have been conducted to evaluate whether the current metals and minerals production capacity is sufficient in India for the short-term, considering 140 GW wind energy production by 2032, and long-term potential, considering 695.5 GW wind energy production (Verma et al. 2022). The production of REEs Nd and Dy with purity required for the application of wind turbines is currently not done in India. Hence, Indian wind turbine manufacturers are dependent on imported materials.

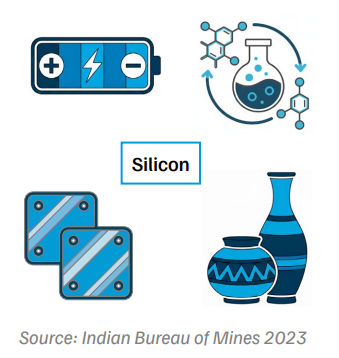

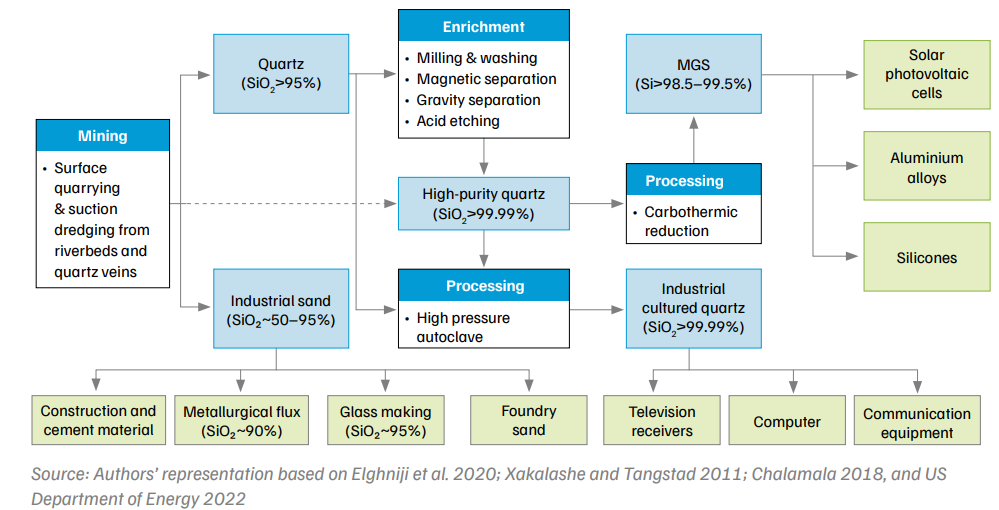

Silicon is the second-most-abundant element in earth’s crust, primarily found as silicon dioxide in quartz and silica sand. Known for its hardness and metallic lustre, silicon finds diverse applications based on purity and particle size, including in electronics, high-purity quartz-based optical fibre, and solar cells.

In nature, silicon is commonly found scattered across the Earth’s surface as silicon dioxide (SiO2 ), also known as quartz and silica sand. Quartz is a very common mineral and is often associated with a wide variety of other minerals, including feldspars, micas, amphiboles, calcite, and zeolites. Based on the grade and particle size, silicon has many applications in different sectors. For instance, industrial sand is used in construction and cementing material, foundries, glass, filtration systems, abrasives, and as flux in metallurgical operations. Industrial cultured quartz is manufactured in autoclaves at high pressure and temperature, especially for electronic applications. The process includes natural quartz (also known as lascas) and a solution of sodium hydroxide or sodium carbonate as raw material, with some additives such as deionised water and lithium salts, and used in communication equipment, computers and receivers.

High-purity quartz (HPQ) is obtained by multiple stages of physical and chemical processing of naturally occurring translucent crystalline silica and has more than 99.99 per cent SiO2 content. It is used in optic-fibre cables, crucibles, and the production of metallurgical-grade silicon, which has industrial uses, including in aluminium alloys, silicones, photovoltaic cells and ferrosilicon (US Geological Survey 2024a).

High-purity quartz is the raw material used to produce metallurgical-grade silicon (MGS). First, quartz is enriched by washing, crushing, magnetic separation and acid etching, to raise its purity to 99.99 per cent SiO₂. Then, MGS production occurs through carbothermic reduction in a submerged-arc furnace at about 2,000°C, where quartz reacts with carbon sources like coke and charcoal. This process yields molten silicon, later refined and solidified to achieve 98.5–99.5 per cent purity, as shown in Figure 15 (Ali et al. 2018; Elghniji et al. 2020; Boussaa et al. 2018).

Figure 15. Simplified process flowsheet of silicon production

Global estimates for quartz reserves and production are not available. However, quartz is widely distributed across countries such as the United States, Australia, Brazil, Canada, China, India, and Russia (US Geological Survey 2024b). In 2024, global silicon metal production was estimated at 4.6 million tonnes, with China dominating with a share of 84 per cent. Brazil and Norway followed, contributing 4 per cent and 3 per cent, respectively. As for ferrosilicon, production was estimated to be about 5.1 million tonnes, with China, Russia, and Brazil as the top producers, accounting for 69 per cent, 9 per cent, and 4 per cent of the global share, respectively (US Geological Survey 2025).

Box 4. Use of silicon in solar PV

Silicon-based solar photovoltaic (PV) technology had a market share of 97.5 per cent, while thin-film technologies had a market share of 2.5 per cent as of 2023 (Fraunhofer ISE 2024). This highlights the importance of silicon in the solar PV supply chain. Metallurgical grade silicon (MGS) is 98 per cent pure and needs to be purified to be used in solar PV; it is ground up and injected into a Fluidised Bed Reactor (FBR) to produce trichlorosilane gas, which is used as a feedstock for the Siemens process (Xakalashe and Tangstad 2011a). Siemens process takes place in a Siemens reactor, where current is passed through a U-shaped silicon seed in the presence of trichlorosilane gas, which undergoes Chemical Vapour Deposition (CVD) to form solid silicon. This results in the formation of polysilicon, which has a purity of 9N silicon (99.999999999 per cent).

Polysilicon is thus formed by breaking it down into smaller pieces, loading it up into a crucible, and melting it down to form a polysilicon bath at temperatures of 1,500°C. Monosilicon ingots are formed around a seed silicon crystal dipped into this bath and pulled slowly upwards using a Czochralski puller. This process is called the Czochralski process (ITRPV 2024). Monocrystalline silicon ingots, thus formed, are further sliced into wafers using diamond-coated wire saws, which are further processed to form solar cells, and assembled into solar modules. As it is such a cornerstone of the solar PV manufacturing process, the scaling up of the latter will lead to higher demand for silicon in the future.

Global silicon demand from solar PV was 390 kt in 2020, and is projected to be between 452 and 810 kt by 2040 (IEA 2021). Despite the abundance of raw material for silicon in the form of quartzite, due to high capital expenditure, operational expenditure, and technological knowledge required, polysilicon production does not exist in India. Solar PV module and cell manufacturers are dependent on imported wafers. While Adani Solar has announced a 2 GW ingot and wafer manufacturing capacity (Yuen 2024), it utilises imported polysilicon and has halted previously announced polysilicon manufacturing plans (Jacobo 2024).

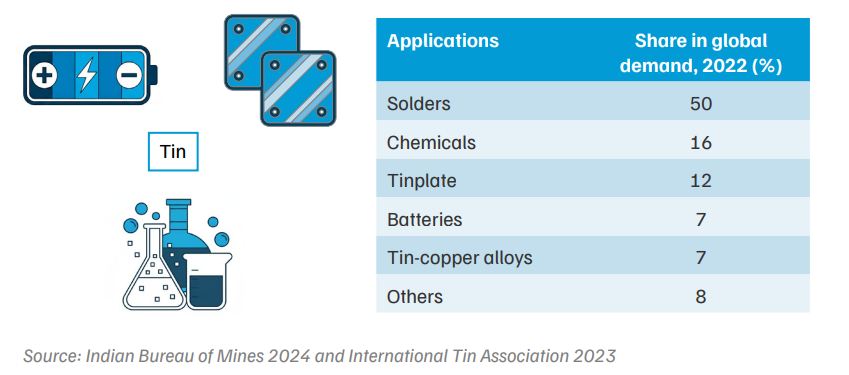

Tin (with the chemical symbol Sn from its Latin name stannum) is a soft, silver-white metal known for its chemical inertness, formability and low melting point (232°C). These properties make it suitable for various applications, including alloys, packing materials and solders.

In nature, about 80 per cent of tin reserves are available in placer deposits. Cassiterite is the primary mineral from which most tin is commercially extracted, while stannite is another mineral. Cassiterite theoretically contains 78.7 per cent of tin. Tin ore, on the other hand, typically contains 1 per cent tin due to associated impurities, such as iron, silicon, niobium, tantalum, zirconium, scandium and tungsten.

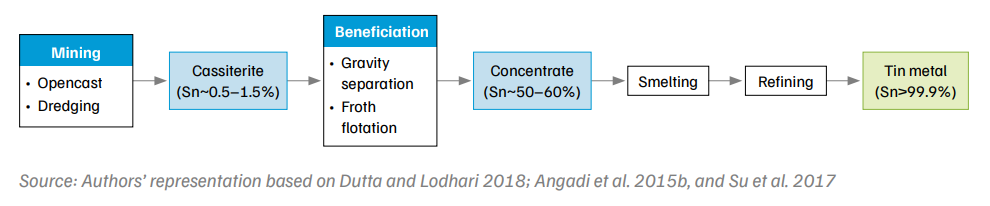

Tin production involves pyrometallurgical operations that convert raw cassiterite ore into high-purity tin, which is essential for industrial applications. First, the ore undergoes pretreatment steps like magnetic separation, roasting, and acid leaching, as cassiterite often occurs in placer deposits where comminution is unnecessary (Su et al. 2017). Following pretreatment, gravity separation and flotation produce a tin concentrate with up to 60 per cent purity and a recovery rate of around 70 per cent (Angadi et al. 2015a), as shown in Figure 16. This concentrate is smelted in furnaces with solid reductants and fluxes, achieving about 99 per cent purity. Finally, the remaining impurities are removed via crystallisation or vacuum distillation, yielding tin with over 99.95 per cent purity (Dutta and Lodhari 2018).

Figure 16. Simplified process flowsheet of tin production

Global supply chain of tin

Compared to other critical minerals, tin reserves and mine production are relatively welldistributed globally, notably in Asian countries such as China, Myanmar and Indonesia. However, in downstream processing, the supply chain becomes increasingly concentrated in China. According to the US Geological Survey, China holds 24 per cent of the world’s tin reserves, followed by Australia, which has 15 per cent out of 4.2 million tonnes. In 2024, China also led global tin mine production, contributing 23 per cent out of 0.3 million tonnes, followed by Indonesia with 17 per cent (US Geological Survey 2025). Tin smelting is even more concentrated, with China alone responsible for 52 per cent of global tin smelter production, followed by Indonesia and Peru (British Geological Survey 2024b).

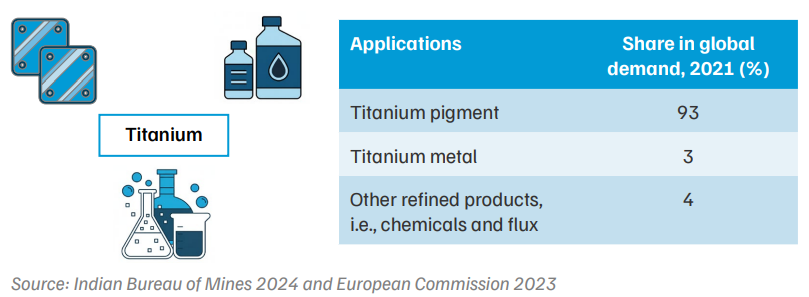

Titanium is a silver-grey, lightweight metal known for its high strength-to-weight ratio and excellent corrosion resistance, even at elevated temperatures. Over 90 per cent of globally produced titanium is used as a pigment, enhancing opacity and brightness in paints and plastics.

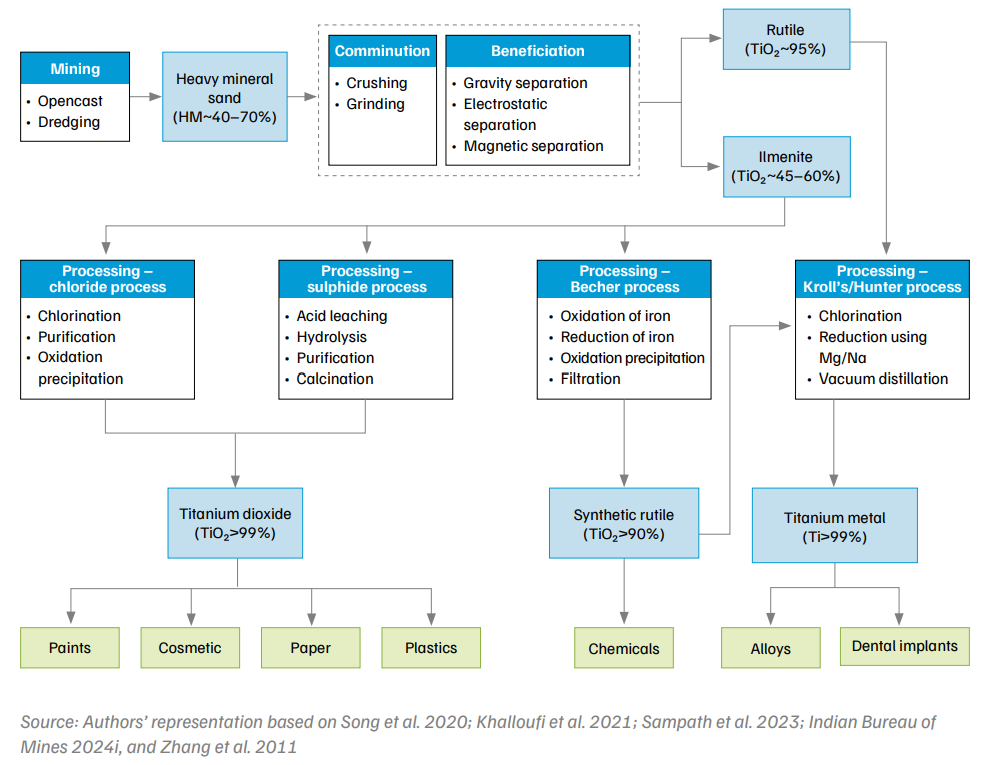

In nature, titanium is found to be associated with iron and vanadium. Ilmenite and rutile are the two primary minerals, and the majority of titanium is obtained from ilmenite, which typically contains 45–60 per cent titanium dioxide (TiO2 ). In contrast, rutile contains up to 95 per cent TiO2 (Zhang et al. 2011a). Both of these minerals are found in the placer deposit in beach sand, along with other heavy minerals such as zircon and monazite. Beach sand is mined through dredging, and beneficiated through an array of physical separation processes to obtain valuable minerals (Indian Bureau of Mines 2024i).

Ilmenite is obtained after the beach sand is beneficiated and processed further based on the application and grade requirement. The hydrometallurgical route is employed to obtain TiO2 from rutile and ilmenite. There are two methods of titanium dioxide production—the chloride process and the sulphate process—as shown in Figure 17. Globally, 60 per cent of TiO2 is produced via the chloride route, and the sulphate route is mostly used in China (Sampath et al. 2023). Natural and synthetic rutile and titanium slag are processed via a thermo-chemical route, known as Kroll’s process or Hunter process, to obtain titanium metal.

Figure 17. Simplified process flowsheet of titanium production

According to the US Geological Survey, out of 510 million tonnes of global ilmenite reserves, Australia holds 35 per cent, followed by China, accounting for 22 per cent of ilmenite reserves, and 37 per cent of mine production in 2024. In midstream processing, the supply chain becomes more concentrated in China, with an installed pigment production capacity of 56 per cent, and titanium sponge production capacity of 63 per cent. In 2024, this nation accounted for 69 per cent of global titanium sponge production, followed by Japan and Russia, with shares of 17 and 6 per cent, respectively. Australia leads the rutile mine production, accounting for 44 per cent in 2024, and has the highest reserves (76 per cent) of natural rutile (US Geological Survey 2024o, 2024m).

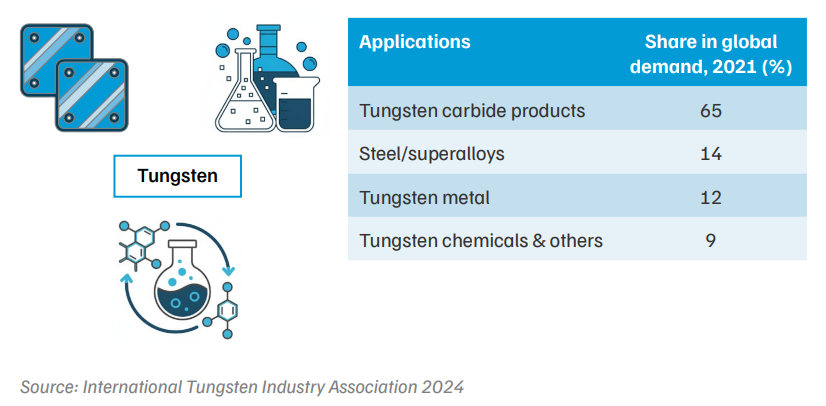

Tungsten (with chemical symbol W for its old name, wolfram) is a greyish-white metal known for its electrical and thermal conductivity and low thermal expansion. Its primary applications include tungsten carbide for cutting tools, ferrotungsten for high-speed steels and superalloys, and tungsten compounds for dyes and inks.

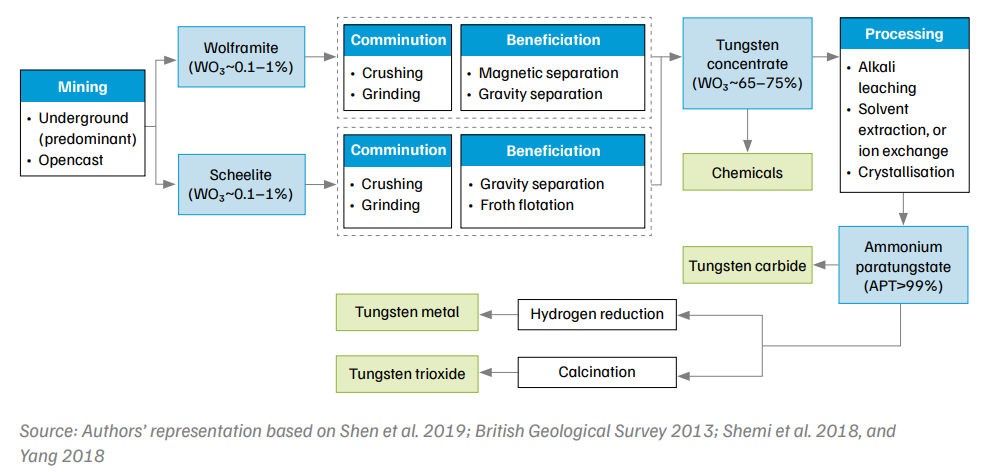

Scheelite and wolframite are the two minerals, found in skarn and porphyry deposits (Surya et al. 2023), typically containing tungsten oxide (WO3 ) in the range of 0.1–1 per cent, and primarily mined through underground mining methods for the commercial production of tungsten.

The current commercial process of tungsten ore processing begins with comminution, followed by pre-concentration, with X-ray and gravitational sorting for scheelite, and optical or hand sorting for wolframite. The beneficiated scheelite concentrate, achieved via gravity separation or froth flotation, reaches up to 65 per cent WO₃. In comparison, wolframite undergoes gravity and magnetic separation to yield a concentrate with over 30 per cent WO₃ (Das et al. 2023; Yang 2018). Further processing and refining involve digestion/leaching of tungsten concentrate, purification of the obtained solution, and then crystallisation to obtain ammonium para tungstate (APT), which is the marketable product and raw material to produce tungsten carbide, compound, and metal (Shemi et al. 2018).

Figure 18. Simplified process flowsheet of tungsten production

China dominates the supply chain of tungsten. As per the US Geological Survey, global tungsten mine production was estimated at 81,000 tonnes in 2024, with China accounting for 83 per cent, followed by Vietnam and Russia with less than 4 per cent and 2 per cent contribution, respectively. Globally, tungsten reserves are estimated at 4.6 million tonnes, with 52 per cent of these reserves located in China. Other countries with substantial reserves include Australia (12 per cent) and Russia (9 per cent) (US Geological Survey 2024p).

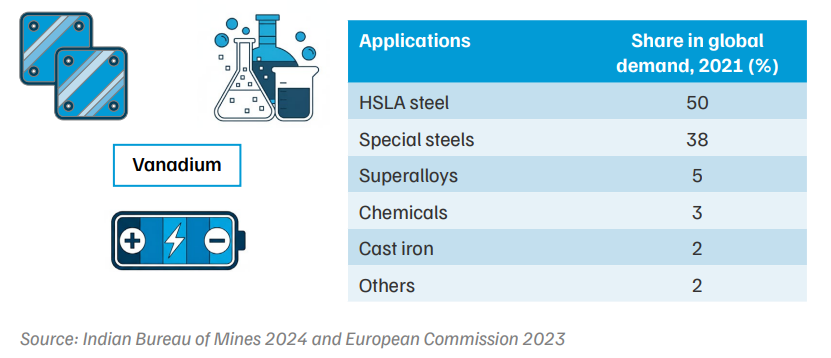

Vanadium is a hard, silver-grey transition metal known for its malleability and ductility. Primarily used in the steel industry as ferrovanadium, it enhances the strength and wearresistance of steel, comprising over 90 per cent of its applications.

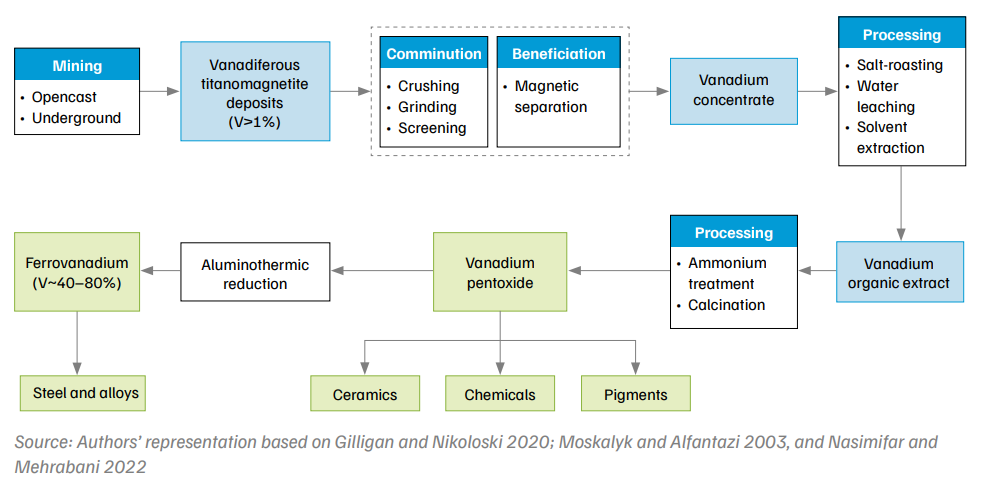

Vanadium is found naturally in several minerals, such as patronite, vanadinite, carnotite, and roscoelite (Indian Bureau of Mines 2024g). Vanadiferous titanomagnetite deposits are exploited for most commercial vanadium production globally, and vanadium is produced both as a primary resource and a by-product. Most vanadium is obtained as a co-product or byproduct of iron and steel production, wherein vanadium is recovered from the slag generated during the smelting of magnetic iron ore. The remaining vanadium is obtained from secondary sources such as red mud from aluminium processing, and spent catalysts in petrochemical processes.

Vanadiferous titanomagnetite, with more than one per cent vanadium pentoxide (V2 O5 ) content by weight, is commonly used as a primary source of vanadium. During processing, the concentrate obtained after beneficiation is salt-roasted at 800–1,000°C, commonly with sodium carbonate, making vanadium soluble for leaching (Gilligan and Nikoloski 2020). After leaching solvent extraction, vanadium from impurities is isolated. Finally, the vanadium precipitates as ammonium polyvanadate, which is calcined to produce V₂O₅. This V₂O₅ is further reduced to ferrovanadium, as shown in Figure 19 (Nasimifar and Mehrabani 2022).

Ferrovanadium is one of the marketable products. Depending on the use case, it contains 40–80 per cent vanadium, and is obtained from iron and steel slag through the pyrometallurgical route of reduction and refining. Additionally, ferrovanadium is produced by the aluminothermic reduction of vanadium pentoxide (Moskalyk and Alfantazi 2003).

Figure 19. Simplified process steps for vanadium production

According to the US Geological Survey, the global reserves of vanadium are estimated to be 18 million tonnes, mostly distributed across Australia, Russia, and China, with their respective shares of 47 per cent, 28 per cent and 23 per cent, respectively. China dominates vanadium production, contributing 70 per cent out of 100,000 tonnes of global mine production in 2024, followed by Russia and South Africa (US Geological Survey 2024q). China also leads global refined vanadium production, having contributed 59 per cent in 2019, followed by the European Union and South Africa at 9 per cent each.

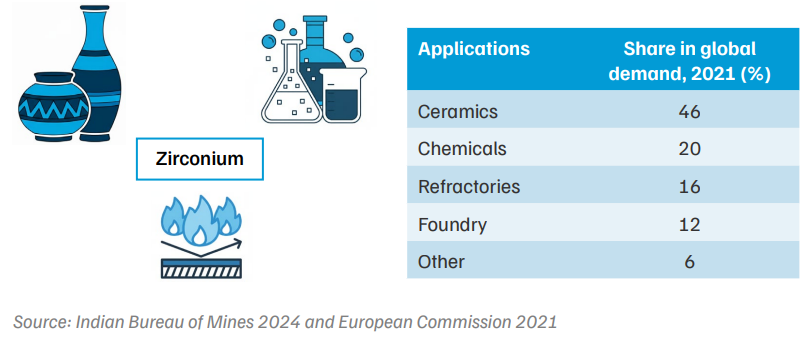

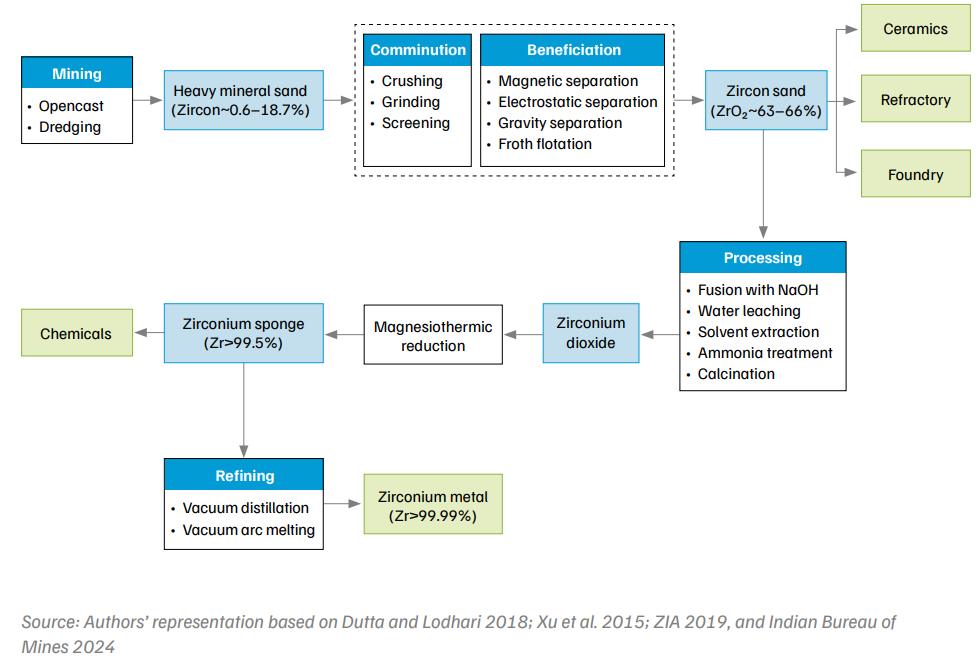

Zirconium is a silver-grey element known for its hardness, tensile strength and heat resistance. Because of these properties, it is used in pumps, valves, and piping in the chemical industry.

Zirconium is found in various deposits, but is primarily extracted from two minerals: zircon and baddeleyite. Most zirconium—around 97 per cent—comes from zircon found in heavy minerals, which also contains other minerals like ilmenite, rutile, leucoxene, monazite and garnet in different amounts.