Council on Energy, Environment and Water Integrated | International | Independent

Suggested Citation: Biswas, Spandan and Aarathi Srinivasan. 2026. Advancing Solar Cell Manufacturing in India: Bridging Gaps in Cell Technology and Lowering Manufacturing Costs. New Delhi: Council on Energy, Environment and Water.

India’s solar module manufacturing capacity has expanded rapidly. However, domestic solar cell manufacturing capacities continue to lag behind, creating import dependence and supply chain vulnerabilities. To scale up, domestic manufacturers have to contend with high manufacturing costs while adapting to a rapidly changing technology landscape. Currently, higher costs for capital and consumables drive up Indian solar cell production costs in comparison to global counterparts, while structural challenges like import dependence, skill gaps, and lagging R&D lead to difficulties in developing indigenous capability.

This study proposes targeted actions for policymakers, solar cell manufacturers, equipment suppliers, and academia to make Indian solar cell manufacturing competitive on both cost and technology.

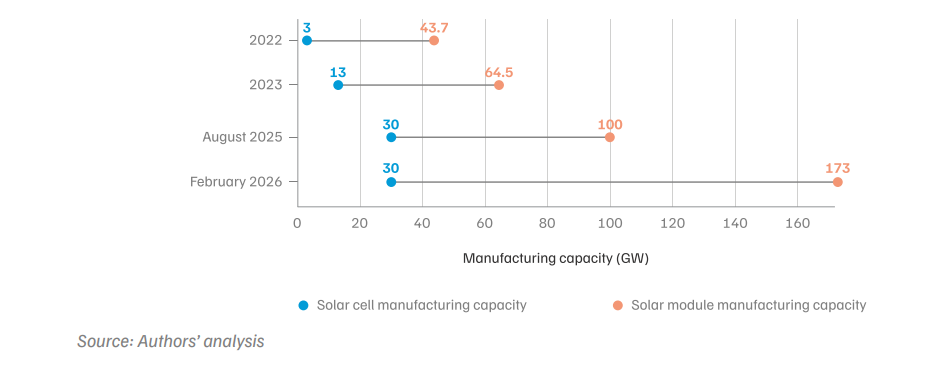

India has rapidly expanded its solar energy deployment over the past decade, emerging as one of the world’s largest and fastest-growing markets. However, this growth in deployment has not matched the growth of domestic manufacturing across the supply chain. Such a mismatch risks creating supply chain vulnerabilities in downstream segments, such as module manufacturing and deployment, due to continued import dependence (Premier Energies 2024; Vikram Solar 2024; Waaree Energies 2024a). As of March 2026, solar module manufacturing is the most established supply chain segment in the Indian solar PV industry, with a manufacturing capacity of 173 GW (MNRE 2026b). In comparison, nameplate solar cell manufacturing capacity is only ~30 GW, forming only 20 per cent of the module manufacturing capacity (authors’ analysis from Waaree Energies 2025; MNRE 2025a; Sinovoltaics 2025; ETEnergyWorld 2024; MNRE 2026a). For the remaining 80 per cent, module manufacturing would have to depend on imported cells primarily from China. Figure ES1 demonstrates the gap in growth between module and cell manufacturing.

Figure ES1. Module manufacturing capacity has outpaced cell manufacturing capacity by more than five times, creating high demand for new cell production

Scaling up solar cell manufacturing is thus necessary to solve this issue and improve supply chain resilience. Such scaling up is also critical for increasing domestic value addition through solar manufacturing, as nearly 60 per cent (InfoLink Consulting 2025c) of the solar module cost is attributable to the solar cells.

However, domestic solar cell manufacturers face a global landscape marked by declining prices and rapidly evolving technology—the global cell technology landscape has shifted, with PERC (passivated emitter rear contact) being replaced by TOPCon (tunnel oxide passivated contact) as the commercially dominant technology within two years (2023 to 2025). In 2 Image: CEEW contrast to this evolution, domestic solar cell manufacturing remains PERC-based, and faces higher manufacturing costs compared to Chinese counterparts. As a result, domestic solar cell manufacturing faces risks of technology lock-in and lack of cost competitiveness.

Hence, vertical integration into solar cell manufacturing must be accompanied by the development of technological capabilities and the reduction of manufacturing costs to build long-term competitiveness. The objective of this report is to identify the key priority areas and strategic interventions that should be targeted by policymakers and domestic solar manufacturers to achieve this twin goal.

This study adopts a techno-economic lens to arrive at the key findings, drawing from secondary literature and stakeholder consultations. Further, the interventions have been mapped by considering domestic policies, actions taken by other nations, and their relevance to the identified gaps.

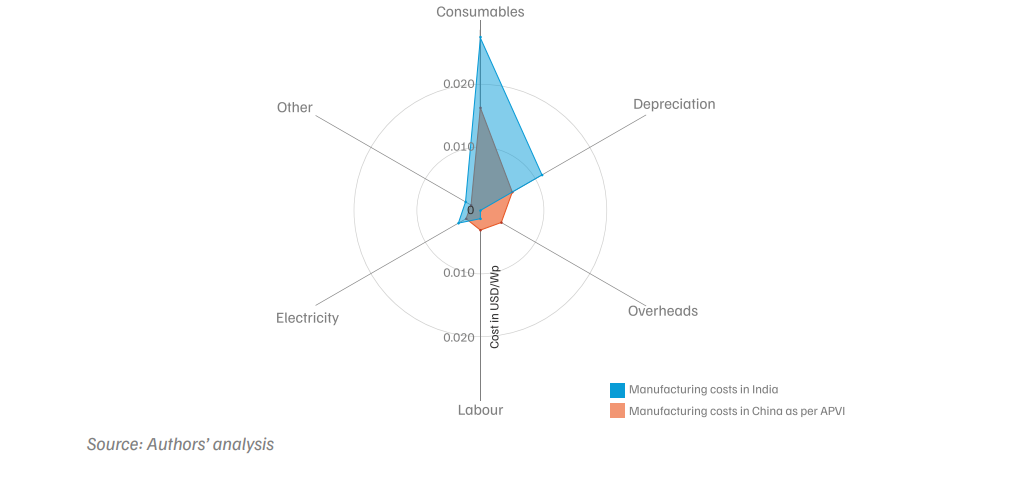

Figure ES2. Higher costs in consumables and depreciation make cell manufacturing ~40% more expensive in India than China

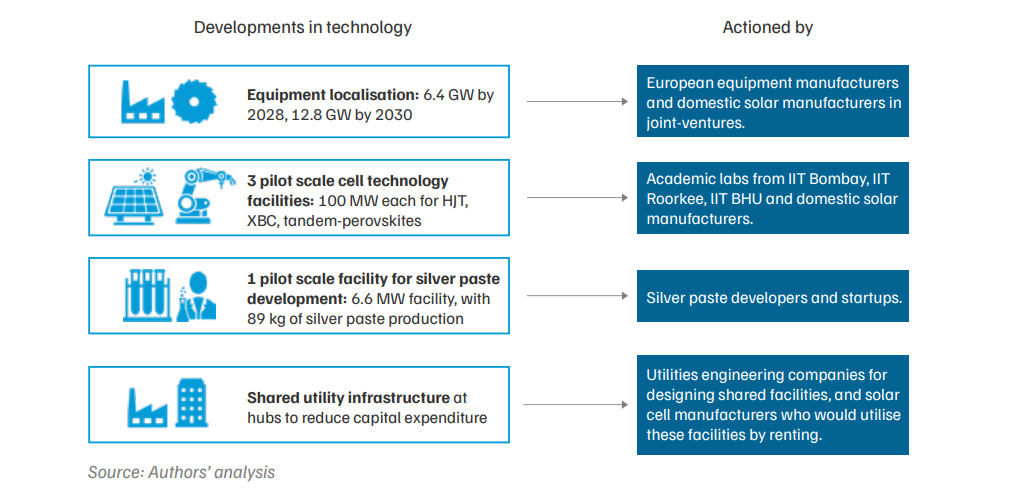

1. MNRE could develop shared infrastructure for machinery localisation, cell technology development, and upfront capital-cost reduction: A national framework should be created to bridge the gap between laboratory research, pilot-scale validation, and commercial deployment. The key priorities are as follows.

2. MNRE could offer one-time capital subsidy to PLI winners to bridge capital expenditure gaps: Based upon our calculation, a one-time capital subsidy of 15 per cent would assist in bridging the capital expenditure gaps between Chinese manufacturers and domestic PLI winners. Execution of the PLI-allocated manufacturing capacity would double the solar cell manufacturing capacity, from nearly 30 GW to 60 GW.

Figure ES3. Framework for developing machinery, technology, materials, and reducing upfront manufacturing costs

3. MNRE could develop skilling programmes and training centres to upskill process engineers and build domestic technological capacity: Scaling solar cell manufacturing will require a substantial increase in skilled process engineers and technicians. Dedicated training centres should be established in key manufacturing states, supported by industry partnerships and specialised curricula targeting process optimisation, equipment handling, and advanced cell technologies. The MNRE, in collaboration with the All India Council for Technical Education (AICTE), can take charge of curriculum and courses development, while the Ministry of Education (MoE) and Ministry of Skill Development and Entrepreneurship (MSDE) can then serve as stakeholders responsible for implementing the courses through establishing the dedicated training centres.

4. Ministry of Commerce and Industry (MoCI) could push for strategic asset acquisition and technology transfer in trade policy: MoCI can negotiate easing of regulations for acquisition of distressed foreign manufacturing assets and intellectual property through trade and investment negotiations. This will push private players to acquire distressed companies. Such acquisitions can accelerate technology upgrading, reduce capital costs, and enable faster entry into advanced cell technologies without duplicating global R&D investments.

By shifting policy focus from module-led expansion towards technology-driven, vertically integrated solar cell manufacturing, India can stabilise its domestic manufacturing base, reduce strategic vulnerabilities, and position itself as a competitive player in a diversifying global solar value chain. Timely and coordinated action across policy, industry, and academia will be critical to ensuring that today’s manufacturing scale translates into durable industrial leadership over the next decade.

Expanding domestic cell manufacturing would ensure supply chain resilience and higher domestic value addition – solar cells contribute nearly 60 per cent of the total module cost. By scaling up, reducing manufacturing costs, and accelerating technology adoption, India's solar cell manufacturing can support both domestic energy transition and build a globally competitive solar ecosystem.

Import duties on silver paste drive up consumable costs. Lack of economies of scale and limited access to subsidised infrastructure drive up capital expenditure. These two factors together lead to higher manufacturing costs.

Domestic manufacturers are dependent on imported equipment. This results in manufacturers remaining dependent on the know-how required to carry out installation and process optimisation. This results in slower commissioning of facilities for newer advanced cell technologies such as TOPCon. The lack of know-how also results in limited ability to upskill process engineers and technicians, who are critical for scaling up cell manufacturing capacities. In addition, weak public and private solar R&D leads to constraints in the timely adoption of next-generation technologies.

Establishing shared manufacturing infrastructure to reduce utility costs, localise equipment, and shared pilot-scale R&D facilities would be essential to become cost and technology-competitive. Further, targeted capital subsidies, developing dedicated skilling programmes, and strategic technology transfers would complement these measures.

Establishing a Sodium-ion Battery Ecosystem in India

Making India a Hub for Critical Minerals Processing

State of the Sector: Critical Energy Transition Minerals for India

Strengthening India's Clean Energy Supply Chains