Council on Energy, Environment and Water Integrated | International | Independent

Context: With the release of ALMM List-II for solar cells, India has taken a significant step toward deepening domestic manufacturing by aligning module deployment with locally manufactured cells.

CEEW Analysis: The list enables greater demand certainty and encourages vertical integration; however, domestic cell capacity still falls short of listed module capacity and is constrained by systemic challenges of high capital expenditure, reliance on imported machinery, and more.

Recommendation: Scaling cell manufacturing through PLI-backed capacity expansion, developing domestic supply chains and workforce skills, and supporting R&D for high-efficiency technologies will be essential to realise the full benefits of List-II.

The push for domestic vertical integration for solar manufacturing, where manufacturers produce both cells and modules, has entered a new phase. In July 2025, the Ministry of New and Renewable Energy (MNRE) released the first version of the Approved List of Model and Manufacturers (ALMM) List-II, covering solar cell models and manufacturers.

Until now, only ALMM List-I, initially introduced in 2021, was in effect, and it only applied to domestic manufacturers of solar photovoltaic (PV) modules. ALMM List-I was temporarily paused due to insufficient domestic module manufacturing capacity, but was reinstated in 2024. Since then, solar PV module imports declined from USD 4,353 million in FY2024 to USD 2,151 million in FY2025, while module manufacturing scaled up by 12 times, from 8.2 GW to 100 GW, from March 2021 to August 2025. As of October 2025, the ALMM List-I enlisted module manufacturing capacity has further increased to 119.8 GW.

Starting June 2026, module manufacturers listed in List-I will be required to buy cells only from List-II manufacturers for modules installed in India. Both ALMM lists aim to anchor demand for domestic solar production, ensure quality control and reliability, and discourage cheaper imports. The ALMM List-II addresses several policy gaps in domestic solar cell manufacturing and is poised to significantly impact domestic module production and deployment. However, other persistent challenges continue to plague the Indian solar cell industry.

The list comprises seven companies, cumulatively making up 17.88 GW of solar cell manufacturing capacity. This accounts for 60 per cent of India’s total estimated cell manufacturing capacity of 29.66 GW. This estimate has been derived by taking a sum of the manufacturing capacities across different firms mentioned in Sinovoltaics, and compared and verified with the manufacturing capacities of companies such as Jupiter, Renew, Tata power, Waaree, First Solar, Emmvee as well as the latest revision of ALMM List-I .

Three cell technologies are currently listed:

As of September 2025, six out of seven manufacturers enlisted in ALMM List-II also operate module production lines, with a combined module manufacturing capacity of 28.4 GW (Figure 1). Among these, Emmvee, Mundra, Premier Energies and Tata Power produce both PERC and TOPCon modules. However, the cell manufacturing capacities of these firms are limited—Premier Engine has PERC and Emmvee has TOPcon—with only Mundra producing both. Jupiter is the only manufacturer under the ALMM List-II that produces only solar cells and no modules; however, it has announced plans of solar module production by the end of 2025.

The list also indicates that cell manufacturing capacity is regionally clustered (Figure 2), with Gujarat and Tamil Nadu together making up nearly three-fourths of the listed cell manufacturing capacity.

These peculiarities of the domestic solar market have most likely determined the following key provisions of ALMM List-II:

List-II provides comprehensive support to domestic social cell production by going beyond policies such as import duties and the Domestic Content Requirement (DCR) mandate. The latter promotes the use of domestically manufactured cells and modules only for specific projects such as Central Public Sector Undertaking (CPSU) Scheme Phase-II for setting up state or central-supported grid-connected solar PV projects, the PM Surya Ghar Yojana for rooftop solar, and the PM-KUSUM programme for off-grid solar PV installations like solar pumps. In contrast, List-II will unlock broader domestic demand from utility-scale solar projects and solar components of hybrid systems, which are not covered under DCR-mandated schemes.

Even projected data promises greater demand. In FY25, India installed 23.83 GW of solar PV capacity, all of which was ALMM List-I compliant. To meet its renewable energy targets of around 292 GW by FY2030, annual solar PV installations between FY2025–26 and FY2029–30 would need to be about 37 GW per year, creating a steady demand for List-II solar cells. A recent study by the Council on Energy, Environment and Water (CEEW) finds that a high-generation mix of 600 GW of clean energy by 2030 would require 377 GW of solar installations, translating to an annual capacity addition of 43.47 GW. This would be slightly higher than India’s estimated 42 GW of solar cell manufacturing capacity by 2026, ensuring a sizable market, while preventing overcapacity and encouraging manufacturers to scale up.

Finally, demand for solar cells will be redirected towards List-II participants by discouraging cheaper imports. As of October 2025, Chinese solar cells are priced at USD 0.042 per Wp (INR 3.57 per Wp). After adding a 20 per cent Basic Customs Duty (BCD) and a 7.5 per cent Agricultural Infrastructure and Development Cess (AIDC), the final cost rises to USD 0.053 per Wp (INR 4.50 per Wp). In comparison, domestic solar cells are priced around USD 0.077 per Wp (INR 6.54 per Wp), making them 45 per cent more expensive and less competitive than imported solar cells, even after implementation of the import duties.

With the implementation of ALMM List-II, List-I manufacturers must source cells only from List-II, effectively eliminating competition from cheaper imported cells in the domestic market. Further, the 30 per cent Anti-Dumping Duty (ADD) imposed by the Directorate General of Trade and Remedies (DGTR) raises the landed price of imported cells to USD 0.07 per Wp (INR 5.85 per Wp), bringing it closer to the domestic solar cell price.

The relatively higher cost of domestic cells will trigger a domino effect, increasing domestic module installation and tariff costs. The rise in solar cell costs will lead to a rise in domestic module cost, by USD 0.024 per Wp. An increase of USD 0.01 per Wp in module costs leads to an increase of domestic solar tariffs by INR 0.06 per unit. As a result, domestic tariffs may increase by INR 0.14 per unit.

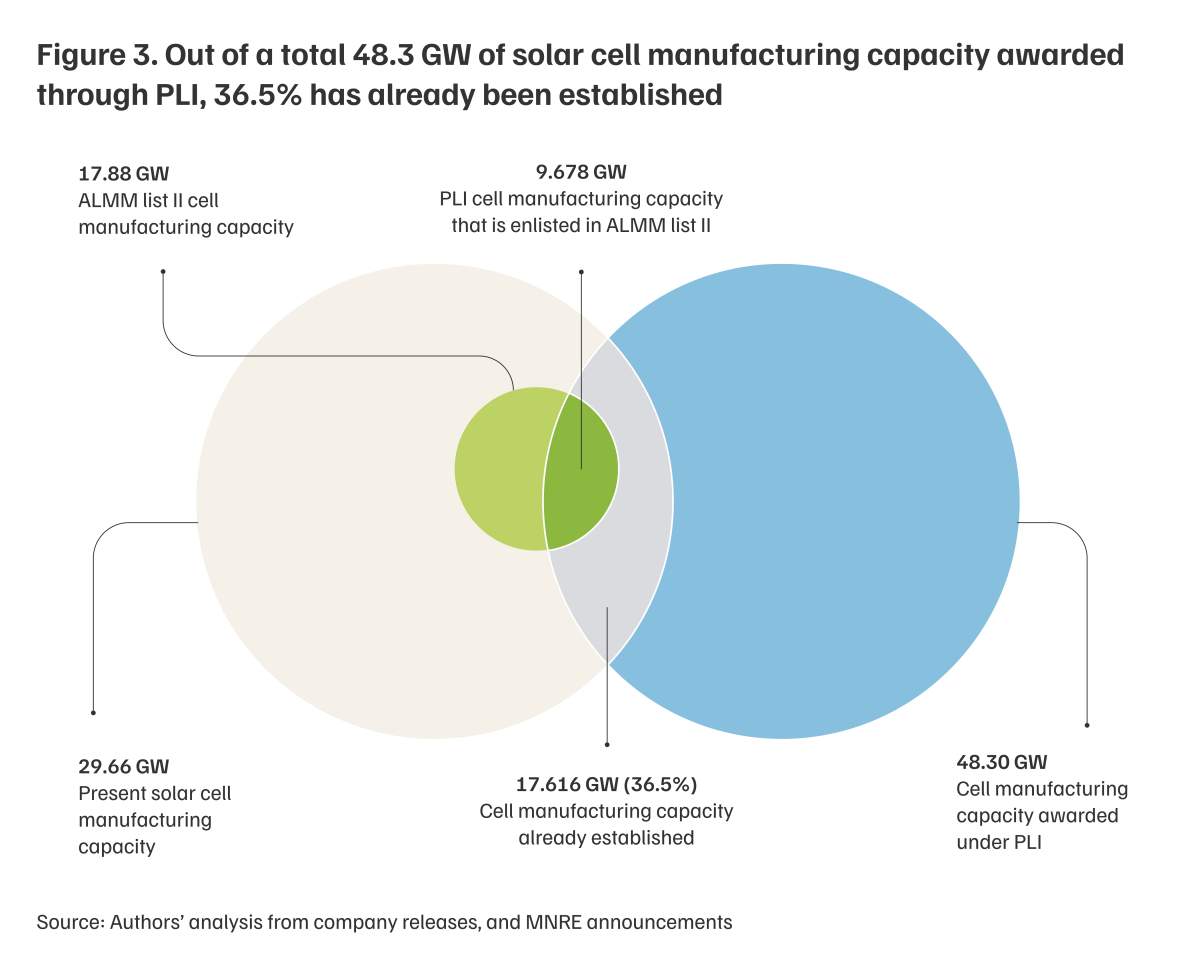

Vertical integration will be critical to improving cost competitiveness. It enables better quality control, reduced logistical overheads and economies of scale, all of which have supported the competitive advantage of Chinese manufacturers. Currently, there are only 15 vertically integrated manufacturers with a cell manufacturing capacity of 29.66 GW, out of which 7 come under the ALMM List-II with a total capacity of 17.10 GW. In contrast, the ALMM List-I has a total of 102 manufacturers with a listed capacity of 119.8 GW, implying that 87 manufacturers with 90.14 GW of cumulative module manufacturing capacity are not vertically integrated. Further, the Production Linked Incentive (PLI) scheme supports a total of 48.3 GW of solar cell manufacturing capacity expansion, 36.5 per cent of which has already been established (Figure 3).

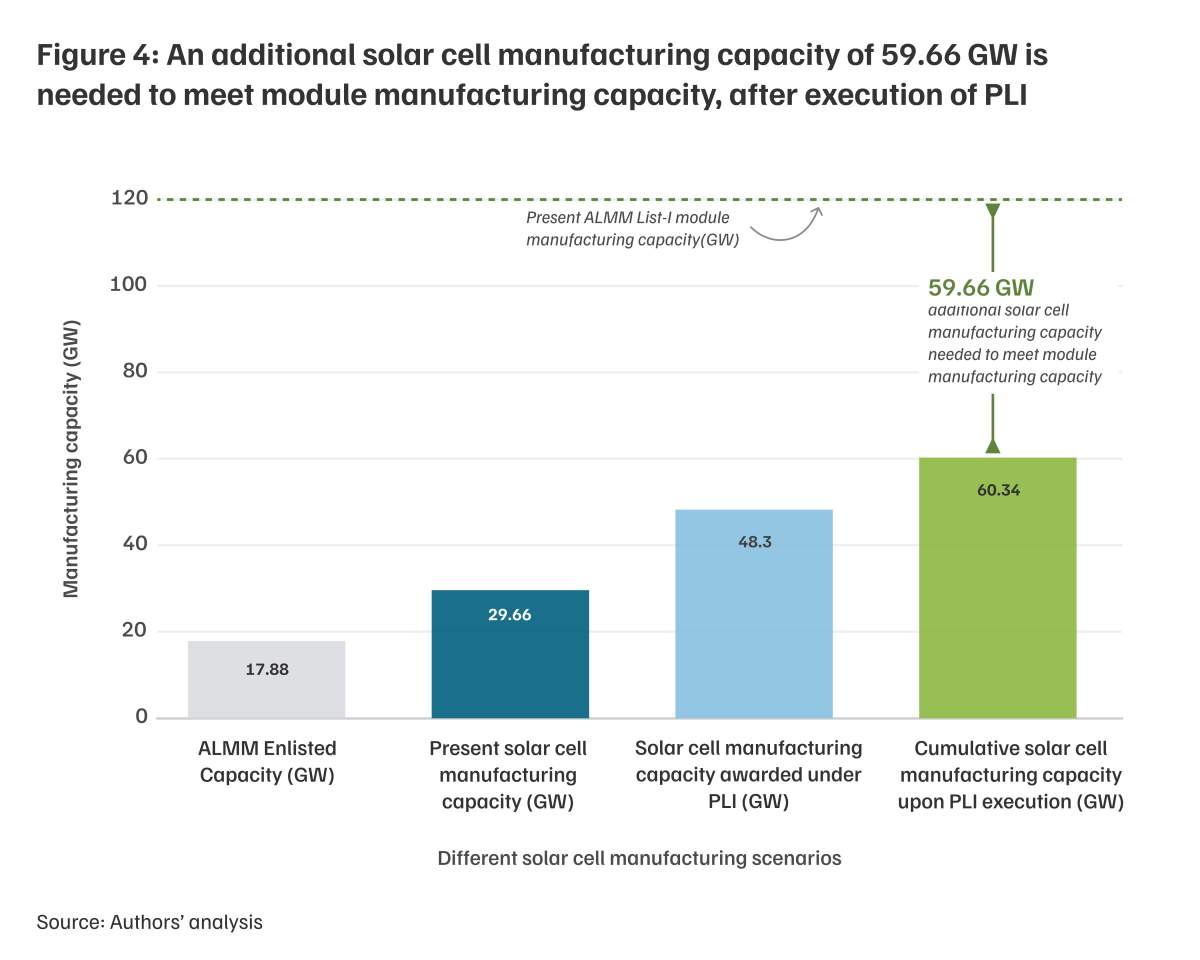

The cumulative solar cell manufacturing capacity upon the establishment of PLI-supported capacity can be estimated to be 60.34 GW (Figure 3). The enlisted capacity under ALMM List-II is thus likely to expand further, but would still fall 59.66 GW short of the 119.8 GW module manufacturing capacity (Figure 4).

Without this additional solar capacity, nearly 50 per cent of the enlisted manufacturing capacity may become ineligible for domestic deployment from June 2026, except for certain special segments where sourcing from ALMM List-I (a) will be permitted. These include government projects under net-metering, behind-the-meter, and open-access mechanisms commissioned before 1 June 2026. Over the longer term, non-vertically integrated module manufacturers will need to either secure a reliable supply from existing solar cell manufacturers or invest in building cell production capacity themselves.

Bridging the 59.66 GW cell manufacturing gap will require USD 4.18 billion (INR 35,500 crore) of investment, as the capital expenditure required to establish cell manufacturing is USD 70 million (INR 595 crore) per gigawatt. The capital expenditure is calculated by taking the average of the values mentioned in Draft Red Herring Prospectus (DRHP) documents released by Vikram Solar and Premier Energies. Due to the capital-intensive nature of solar cell production, scale-up is likely to be led by larger, established firms. This may result in an ecosystem where a limited number of vertically integrated manufacturers dominate cell production, supplying both captive module lines and non-vertically integrated module manufacturers.

While the ALMM List-II supports domestic solar cell manufacturing by restricting imports and creating assured domestic demand, it does not address the broader structural ecosystem challenges. The sector continues to face high capital expenditure and an overreliance on imported machinery and key consumables such as silver paste. This reliance limits the scope for domestic R&D and technology commercialisation, since much of the specialised know-how of manufacturing processes rests with Chinese equipment manufacturers. Moreover, cell manufacturers face a shortage of skilled process engineers and technicians, limiting their ability to optimise production lines for high-efficiency solar cells and achieve higher throughputs .

If provided with timely capacity expansion and targeted policy interventions to overcome these constraints, ALMM List-II can serve as a catalyst for scaling up vertical integration, advancing technology leadership, and stimulating demand in upstream segments such as ingot-wafer and polysilicon production.

Spandan Biswas is a Research Analyst, and Ajinkya Kale is a Programme Associate at the Council on Energy, Environment and Water (CEEW). Send your comments to spandan.biswas@ceew.in.

Add new comment