Council on Energy, Environment and Water Integrated | International | Independent

Recent auctions for green ammonia set record-low tariffs, signalling for the first time that green hydrogen derivatives can compete with fossil fuels in commercial markets. Long dismissed as too expensive, these fuels are now edging toward economic viability.

Green ammonia, a green hydrogen derivative, is a vital feedstock for fertiliser production in India. India is the second-largest consumer of fertiliser in the world, and ammonia forms the building block of these urea and non-urea fertilisers. However, around 86 per cent of the total ammonia consumed in India is reliant on imports of ammonia, natural gas, or ammonia embedded in fertiliser end-products. Under the ambitious National Green Hydrogen Mission (NGHM), the Solar Energy Corporation of India (SECI) conducted a landmark reverse auction in August and September that cleared thirteen green ammonia projects at record-low prices ranging between INR 49.80 per kilogram and INR 64.7 per kilogram, securing supplies to seven non-urea fertiliser producers in nine states under ten-year contracts. At approximately USD 594-774 per tonne after including GST, the green ammonia price range in India is much more favourable against the EUR 1,000 per tonne (~USD 1,160 per tonne) awarded in the most recent European green ammonia auction for a project in Egypt. This is good news.

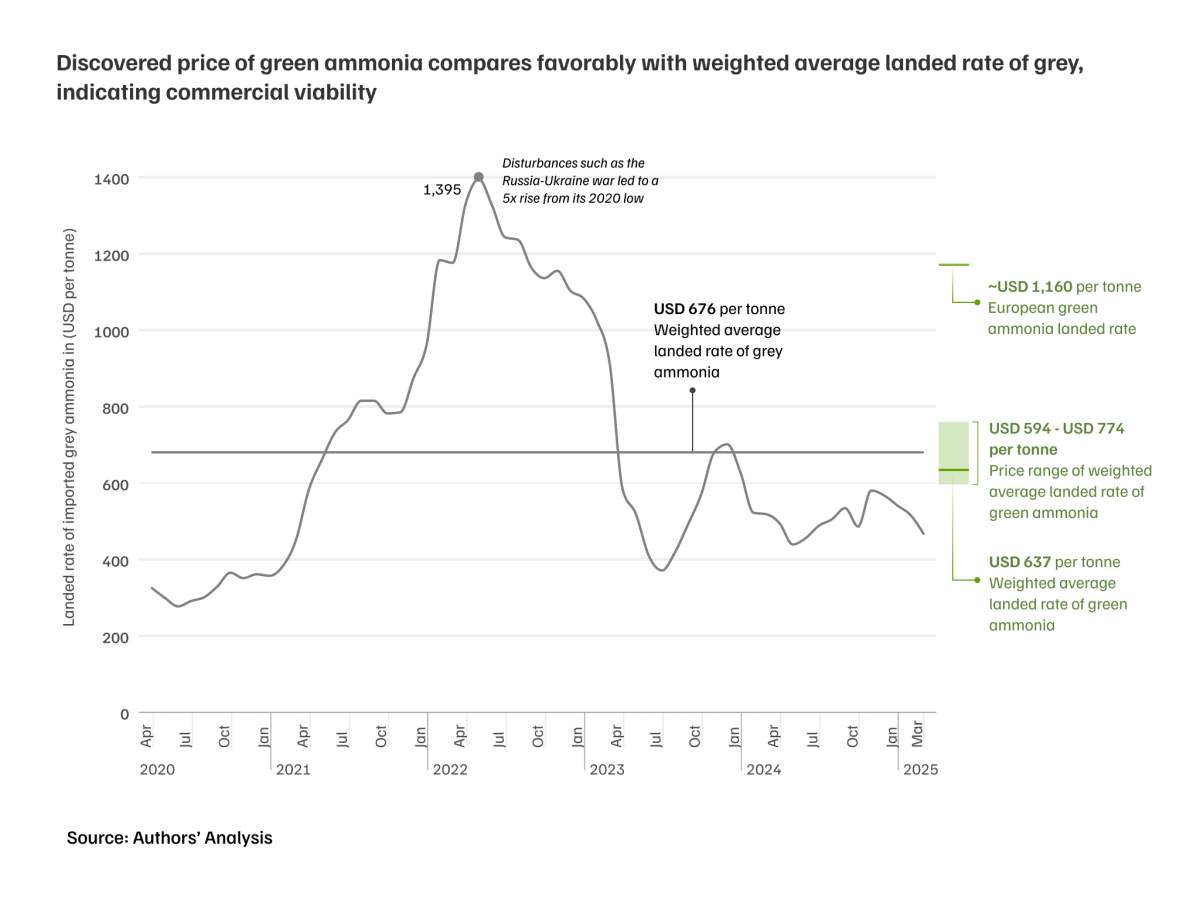

It means that green ammonia is approaching commercial viability compared to imported grey ammonia, which accounts for more than 70 per cent of the ammonia used in India’s non-urea fertiliser production. The weighted average green ammonia price of USD 637 per tonne (range of USD 566 - 737 per tonne) is lower than the five-year weighted average import price of grey ammonia at USD 676 per tonne, as shown in Figure 1. The historical landed cost of imported ammonia is obtained after considering a basic customs duty (BCD) of 5 per cent, a social welfare surcharge of 10 per cent on the BCD and a GST of 18 per cent.

Figure 1: Discovered price of green ammonia compares favorably with weighted average landed rate of grey, indicating commercial viability

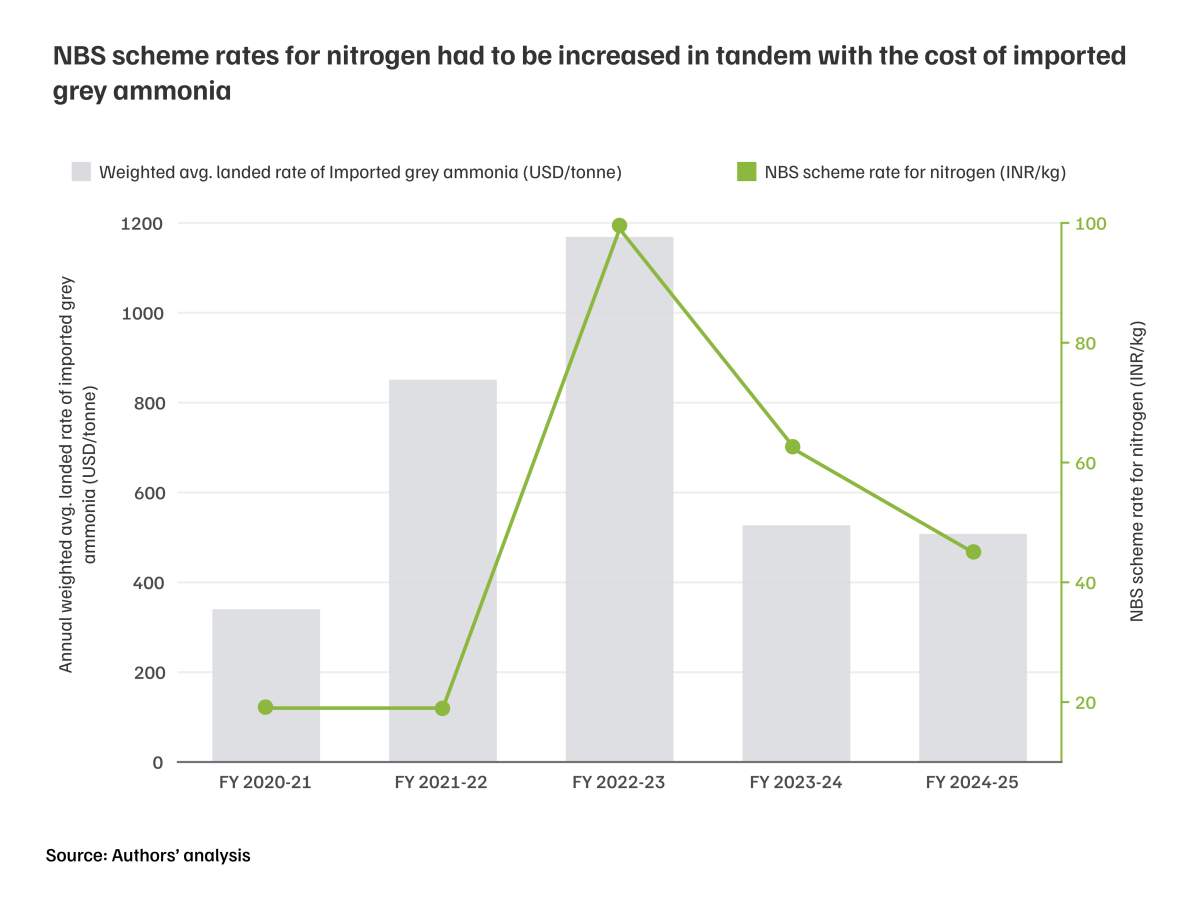

Due to recent geopolitical conflicts such as the Russia-Ukraine war, the landed rate of imported ammonia surged to a peak of USD 1,395 per tonne in 2022, a five-fold rise from its 2020 low. This volatility exposed both fertiliser producers and the government to abrupt cost shocks. In response, subsidy rates for nitrogenous non-urea fertilisers under the Nutrient-based Subsidy (NBS) scheme had to be increased sharply by India, as presented in Figure 2. This placed additional pressure on the Indian government's budgetary expenditure, highlighting the vulnerability of relying on imports for critical industrial feedstocks.

Figure 2: NBS scheme rates for nitrogen had to be increased in tandem with the cost of imported grey ammonia

Various interventions by the central and state governments in India could have been critical in mitigating risks for green ammonia projects and lowering the cost of production to achieve record-low prices.

The Ministry of New and Renewable Energy (MNRE), through the National Green Hydrogen Mission (NGHM), offered production-linked incentives for the first three years to developers, with a total support of INR 1,533 crore. Further, project developers could have availed various power- and non-power-related incentives offered by various state governments in India. The total tender volume was bifurcated among 13 non-urea fertiliser plants spread across the country to minimise the risk of offtake associated with any single procurer.

SECI conducted an e-reverse auction, ensuring competitive and transparent price discovery. One of the main reasons developers were attracted to the auction was the inclusion of a strong payment security mechanism (PSM). This mechanism reduced the risk of payment delays from fertiliser companies. It included a mandatory three-month letter of credit issued by the buyer, a voluntary payment security fund set up by the procurers, with oversight from the Government of India to ensure timely payments.

We find that there is a structural shift in grey ammonia prices in international markets. The stable cost of imported grey ammonia ranged between USD 336 per tonne to USD 427 per tonne between FY 2017-18 to FY 2020-21, whereas after the pandemic, the prices seem to have settled at USD 527 (in FY 2023-24) - USD 508 (in FY 2024-25) per tonne. This is roughly 50 per cent higher than the price of USD 340 per tonne observed in FY 2020-21. Given that the cost of green ammonia in 13 tenders ranges from USD 566–737 per tonne, it can be concluded that the auction-discovered prices for green ammonia are now within striking distance of recent grey ammonia landed costs.

The cost of imported grey ammonia is subject to international price shocks. The costs of imported grey ammonia, or the imported LNG used for its production in India, are tied to the US dollar, which has appreciated at a CAGR of 3.3 per cent against the Indian rupee over the past decade, according to our estimations. If the trend continues, it implies that Indian fertiliser plants will pay a higher price for imported grey ammonia in rupees even though the cost in dollars remains the same. On the other hand, green ammonia procurement from domestic suppliers will be structured through rupee-denominated contracts, inherently shielding the Indian fertiliser industry from currency fluctuations that affect grey ammonia. If this trend continues, long-term fixed-price rupee-denominated green ammonia contracts will enable fertiliser companies to achieve lower costs in the future and reduce subsidy burden for the government.

Finally, a developing country like India needs stability in energy prices. Unlike the price of imported grey ammonia, which is subject to vagaries of the international markets due to geopolitical events and other factors, domestically produced green ammonia offers India a secure supply at stable prices. This gives the Government more flexibility for allocating budget to other developmental needs.

These dynamics underscore the urgent need to develop a domestic green ammonia supply, underpinned by long-term offtake agreements and dedicated infrastructure, to mitigate price volatility and supply-chain risks and promote self-sufficiency in India’s fertiliser sector.

To capitalise on the auction-discovered prices and safeguard India’s fertiliser sector against import-related volatility, a coordinated set of policy and industry measures is required. We outline four specific levers in the following recommendations.

First, the Ministry of Chemicals and Fertilisers (MoCF) and the MNRE should jointly pursue a complete substitution of imported grey ammonia in non-urea fertiliser production. Achieving this goal could unlock domestic demand for around 2.3 million tonnes per annum of green ammonia, necessitating an expansion of the current 724 kilo tonnes per annum (ktpa) procurement tender. Further, domestically produced ammonia for non-urea fertiliser production, estimated to range between 700 and 800 ktpa, could also be replaced over time. This expansion could be pursued in a phased manner through conditional mandates for additional green ammonia procurement, triggered by relative price movements between green and grey ammonia. The MoCF could reform the NBS framework to institutionalise such a mandate in coordination with the MNRE. Regardless, with long-term green ammonia contracts in place, the MoCF can stabilise its expenditure under the NBS scheme, since these contracts naturally hedge against commodity-price volatility.

Second, the state governments of Gujarat, Tamil Nadu, Kerala, Goa and Karnataka, which host significant non-urea fertiliser production capacity and which do not have a green hydrogen or green ammonia policy yet, should introduce targeted incentives to spur domestic consumption of green ammonia. In parallel, all states may consider directing state-owned fertiliser companies to pioneer green ammonia uptake while benefiting from provisions in central and state government policies.

Third, global offtakers of green ammonia and other green hydrogen derivatives in Europe and East Asia must prioritise co-development opportunities to synergistically leverage India's cost advantages in green hydrogen derivatives. Importing countries must work with India on harmonising standards and regulations that suit Indian project requirements and create financing structures that lower the cost of capital in India, which could further lower production costs. Such efforts will enable importing nations to procure cost-competitive green ammonia from a trustworthy and stable trading partner in India, leading to mutually beneficial partnerships.

Fourth, recognising that urea represents over 80 per cent of India’s ammonia consumption, the sector must also prepare for green ammonia blending in urea production. An independent techno-economic study should first identify optimal blending ratios and assess impacts on plant operations, overall energy efficiency, and external carbon dioxide requirements. Simultaneously, a pilot project at one or two major urea facilities ought to trial the determined blend over a prolonged production cycle, periodically reporting on predetermined project metrics. These parallel initiatives will build the technical confidence and operational readiness needed to scale green ammonia in India’s dominant fertiliser segment once its economic viability further improves.

Finally, the emerging viability of green ammonia indicates that green hydrogen and green methanol—used in the chemicals, shipping and refining sectors—could also approach cost competitiveness in the near term. Procurement tenders for these sectors, modelled on the approach adopted for fertilisers, could also be explored under the NGHM.

Decarbonising India’s fertiliser sector hinges on translating competitive auction prices into a resilient domestic supply of green ammonia at scale. The record‐low tariffs uncovered under the Strategic Interventions for Green Hydrogen Transition (SIGHT) Scheme demonstrate that green hydrogen derivatives are near commercial viability today, not in some distant future. By implementing a coordinated national and state-level incentive framework, forging international partnerships and preparing the urea segment for blending trials, policymakers and the industry can lock in these gains. Immediate action will safeguard India’s food security, stabilise subsidy burdens and establish the country as a global leader in the production of green hydrogen and derivatives.

The authors are grateful to Dr Sachchida Nand, former Additional Director General, Fertiliser Association of India, and Hemant Mallya, Fellow, CEEW, who reviewed the blog, and Ribhav Pal, Consultant, CEEW, for his input.

Karan Kothadiya is a Programme Lead and Deepak Yadav is Senior Programme Lead at Council on Energy, Environment and Water (CEEW). Send your comments to karan.kothadiya@ceew.in.

Add new comment