Council on Energy, Environment and Water Integrated | International | Independent

Context: India’s widening gap between peak and average power demand is increasing system costs, while long-term power purchase agreements offer limited flexibility in managing short-duration peaks.

CEEW analysis: India’s first Contract-for-Difference pilot introduces a mechanism that can de-risk market-linked renewable energy and storage, improve wholesale market liquidity, and support clean peak power procurement.

Recommendation: To scale market transactions using instruments like Contracts-for-Difference, India must strengthen pricing benchmarks, increase buyer participation, develop long-term hedging tools, and pursue broader electricity market reforms.

India's peak power demand touched a record 256 GW on 25 April 2026, with projections of 270 GW this summer. But the challenge is the widening gap between this growing peak and average demand. Capacity built to meet short periods of extreme demand sits underutilised for most of the year, raising system costs and, ultimately, consumer tariffs.

In the last two decades, India has quadrupled its installed power generation capacity to fuel a rapidly growing economy. This expansion was enabled largely through long-term power purchase agreements (PPAs), which provided assured payments and reduced investments for coal-based plants. In renewables, competitive auctions with 25-year PPAs led to sharp tariff declines and rapid capacity additions. However, while this model was effective for scaling supply, it is less suited to today’s dynamic demand patterns. Long-term PPAs lock in capacity for decades regardless of when electricity is actually needed. They are designed to meet expected baseload demand, not respond flexibly to short-term peaks or increasing uncertainty in consumption patterns.

This is where the Ministry of New and Renewable Energy’s (MNRE) recent push towards Contracts-for-Difference (CfDs) becomes significant. Unlike traditional PPAs, CfDs can complement existing baseload arrangements by channelling flexible, demand-responsive clean power into wholesale markets. This allows India to competitively procure electricity when it is most needed while providing an alternative procurement route alongside long-term contracts.

A Contract-for-Difference (CfD) is a financial instrument designed to manage the risk of revenue uncertainty for generators selling electricity exclusively on market platforms (called merchant plants), where electricity prices fluctuate based on real-time demand and supply.

In advanced power markets, CfDs provide revenue stability by guaranteeing a fixed benchmark, known as the strike price (SP), which is typically determined through competitive bidding and reflects the generator’s cost to supply. The contract then settles the difference between this strike price and the prevailing market or reference price.

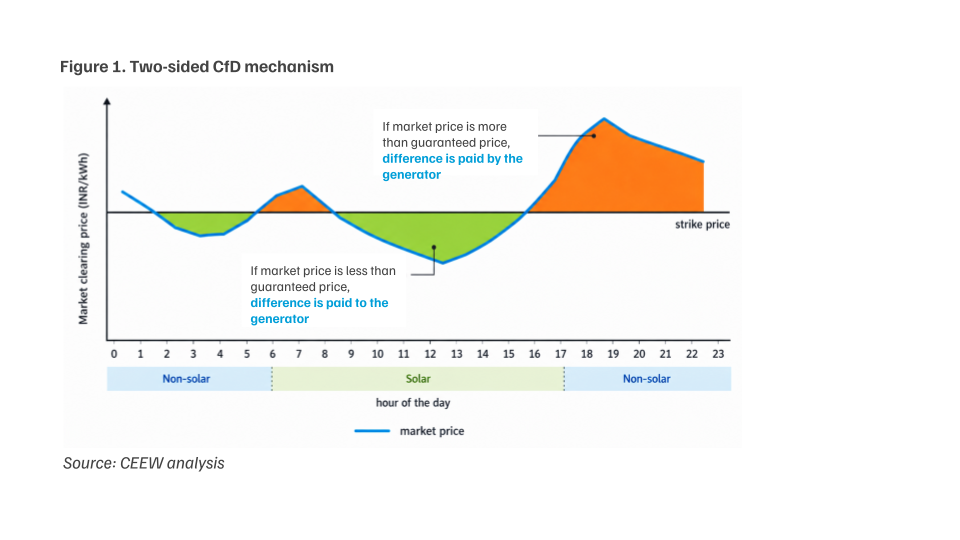

In a two-way CfD (Figure 1):

- If the reference price < SP, the generator receives a payment to cover the shortfall.

- If the reference price > SP, the generator pays back the excess revenue.

This structure protects generators from low-price periods while preventing windfall gains during high-price periods. In countries such as the United Kingdom and Germany, where CfDs are prevalent, these payments are usually managed through government-backed financial settlement pools managed by counterparties.

India’s wholesale electricity markets remain thin. Despite nearly 17 years of formal operation, power exchanges—platforms where electricity is bought and sold for short-term horizons—account for only about seven per cent of total electricity generation, functioning largely as a last-resort option for buyers. The primary cause is the dominance of legacy long-term PPAs, which lock most distribution companies into fixed procurement arrangements. This creates a self-reinforcing cycle: low trading volumes lead to volatile prices, which discourage buyers such as discoms from participation. Weak demand, in turn, deters suppliers from entering the market, further constraining market depth (Figure 2).

Renewable energy and storage are well-placed to break this cycle for two key reasons:

But merchant renewable energy plants face risks operating in illiquid markets. These risks are difficult to quantify and, in many cases, still poorly understood. Without instruments to discover and manage these risks, investment in market-based capacity remains constrained and wholesale market liquidity remains weak. This is the structural gap that India’s CfD is designed to fill: by stabilising revenues sufficiently to attract investment while preserving enough market exposure to drive competitive behaviour.

In March 2026, the MNRE approved a pilot CfD scheme for 500 MW of renewable energy capacity, making India one of the first developing economies to formally adopt a CfD instrument for clean power. The Solar Energy Corporation of India (SECI), the nodal implementation agency, has since issued a tender that gives concrete shape to the framework.

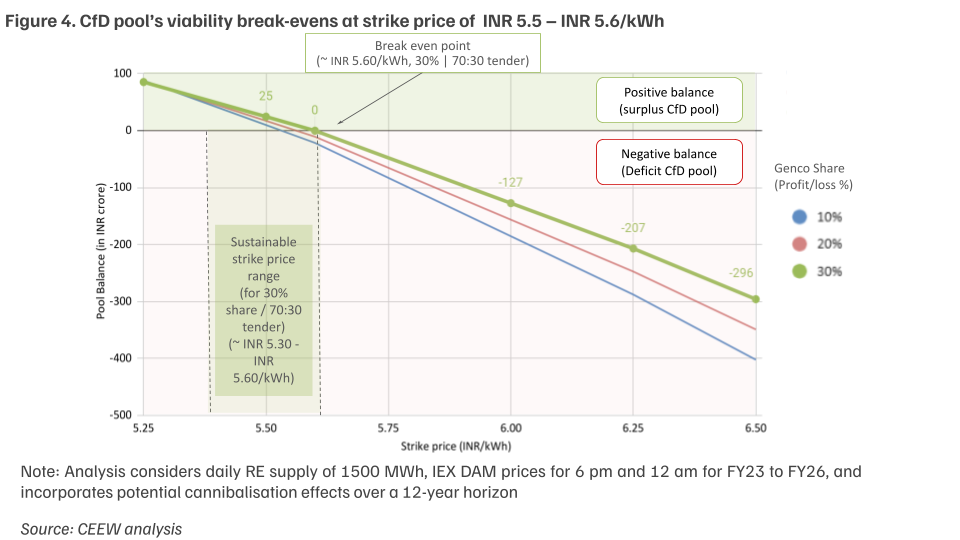

The pilot is built around a two-way, financially settled CfD contract model. SECI, as a counterparty, manages a dedicated stabilisation fund, seeded at INR 76 crore to pay developers when market prices fall below the strike price and receiving returns when prices exceed it (Figure 3). The design serves three broad objectives: (i) speeding up the deployment and offtake of renewable energy and battery storage; (ii) facilitating clean energy availability during critical evening peak-demand (non-solar) hours; and (iii) stabilising market prices to attract a wider set of buyers and sellers.

Note: GDAM is the Green Day-Ahead Market, where renewable power is traded a day in advance; DAM is the Day-Ahead Market, where electricity is bought and sold for delivery the next day on Power exchanges; RTM is the Real-Time Market, which enables trading close to the time of delivery to manage last-minute imbalances; REC stands for Renewable Energy Certificates, tradable instruments representing units of clean power; and REIA refers to Renewable Energy Implementing Agency, such as SECI, that anchor procurement on behalf of buyers/discoms.

The Government of India has already signalled the need for such market-linked instruments. The Ministry of Power's Report of the Group on Development of Electricity Market in India (2023) and the Draft National Electricity Policy 2026 both call for instruments that increase efficiency in power procurement.

The pilot establishes a strong foundation for catalysing innovation. Four design challenges will determine whether CfDs can fulfil their potential to deepen wholesale markets, de-risk market-linked clean energy investment, and support cost-effective peak power procurement.

The SECI tender marks a decisive move from viewing CfDs as a policy idea to deploying them as a market instrument. It reflects a careful balancing act: de-risking investments to attract capital while preserving enough market signals to drive competitive behaviour and build exchange liquidity. The value of the pilot lies in the market intelligence it generates: on investor appetite, on price formation dynamics, and on the structural reforms needed to design further such sophisticated market instruments.

For policymakers, the next steps are as important as the pilot itself. The Central Electricity Regulatory Commission’s support for pricing benchmark development, the Government of India’s effort to design subsequent CfD rounds informed by pilot learnings, and the broader pace of electricity market reform will determine whether such instruments can build a vibrant and efficient power market.

Rashi Singh is a Programme Associate, Disha Agarwal is a Senior Programme Lead, and Vishal Tripathi is a Consultant at the Council on Energy, Environment and Water (CEEW).

Add new comment